Starbucks (SBUX 0.29%), the largest coffee chain in the world, doesn't have many direct competitors. The only rival that comes close to matching its reach is Dunkin' Brands (DNKN), the parent company of Dunkin' Donuts and Baskin-Robbins.

Source: Pixabay.

Starbucks operates 22,088 stores worldwide, compared to Dunkin' Brands' 11,300 Dunkin' Donuts locations and 7,500 Baskin-Robbins stores. Both chains are already massive, but which business has the potential to grow faster in the long term? To determine the answer, let's compare the two businesses' top lines, bottom lines, dividends, valuations, and growth plans.

Top-line growth

Dunkin' Brands went public in 2011, but its top-line growth doesn't come anywhere close to matching that of Starbucks.

Source: YCharts.

Dunkin' Brands' comparable-store sales growth also lags behind Starbucks'. Last quarter, Dunkin' reported systemwide annual comps growth of 6.2%. Dunkin' Donuts reported 2.7% growth in the U.S. and 1.7% growth abroad, while Baskin-Robbins posted 8% U.S. growth and 0.3% international growth.

Starbucks reported 7% annual comps growth last quarter, with a 7% jump in the Americas, a 12% gain in the CAP (China Asia-Pacific) region, and 2% growth in the EMEA (Europe, Middle East, Africa) region. In terms of pure sales growth, Starbucks comes out on top.

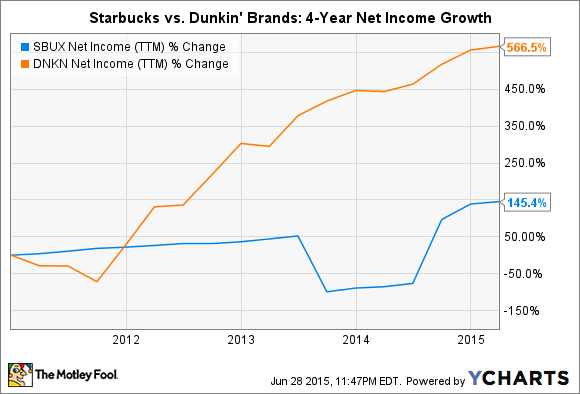

Bottom-line growth

However, Dunkin' has grown its earnings at a faster rate than Starbucks.

Source: YCharts.

This is because all of Dunkin's stores are franchised, while only 46% of Starbucks stores are franchised. Franchising stores shields the parent company from overhead risks, but these locations only generate franchise fees and royalties for the parent. Company-owned stores shoulder overhead risks but also book full sales and profits.

Dunkin' boasts beefier margins than Starbucks. Last quarter, Dunkin's adjusted operating margin came in at 47%, compared to 17% for Starbucks.

Starbucks sometimes converts licensed stores to company-owned locations by buying them once they achieve a certain level of profitability. In Japan, for example, Starbucks recently bought out over 1,000 licensed locations and turned them into company-owned shops.

Dividend growth

Starbucks currently has a forward annual dividend yield of 1.2%, while Dunkin's sits at 2%. Over the past 12 months, Dunkin' Brands paid out 60% of its free cash flow as dividends, compared to 37% for Starbucks. Some investors might assume that means Dunkin' is more "generous," but it also indicates Starbucks has more room to increase its dividend in the future.

Both companies have consistently raised their payouts each year. Since going public, Dunkin' has raised its dividend an average of 22% annually, which is comparable with Starbucks, which has boosted its dividend an average of 23% per year since 2011.

Valuations

Starbucks and Dunkin' Brands stocks have respectively rallied 34% and 28% since the beginning of the year, easily outperforming the S&P 500's 1% gain. But as a result, their multiples have become a bit overheated in comparison to that index.

|

Trailing P/E |

Forward P/E |

Trailing P/S |

|

|

Starbucks |

32.2 |

29.4 |

4.6 |

|

Dunkin' Brands |

32.6 |

24.8 |

6.9 |

|

S&P 500 |

21.5 |

16.7 |

1.8 |

Source: Yahoo! Finance and Thomson Reuters, June 29.

While neither Starbucks nor Dunkin' look cheap, investors should note both their P/E ratios are still lower than the industry average of 40 for the "specialty eateries" sector.

Plans for growth

Both Starbucks and Dunkin' Brands are expanding into China to generate fresh sales from the nation's growing middle class. Starbucks recently opened its 1,600th store there, and plans to boost that number to over 10,000 within five years. Dunkin' plans to open 1,400 stores in China via a joint venture over the next two decades

Back at home, Starbucks has a stronger presence in the western and central U.S., but Dunkin' Donuts dominates the eastern seaboard. Dunkin' intends to move westward and open 200 stores in California over the next five years, which might adversely impact Starbucks' U.S. sales.

Both companies are also piggybacking off the success of Keurig Green Mountain's home coffee brewers. Starbucks had shipped 2.5 million K-Cup packs as of last quarter, and Dunkin' Brands is expanding its K-Cups from its restaurants to over 60,000 retail locations in the U.S., as well as to online channels. While neither company has disclosed exactly how much revenue those K-Cups generate, they should enhance their consumer packaged goods businesses.

Source: Starbucks.

The verdict

Dunkin' Brands is a solid company with a lower-risk business model, robust bottom-line growth, and decent dividends. But if I could only buy one, I'd pick Starbucks for two reasons.

First, Starbucks has better sales growth, particularly in critical foreign markets. That sales growth offsets its lower earnings growth, and gives Starbucks the ability to shift strategies much faster than Dunkin' Brands. Second, it has a premium appeal that Dunkin' Donuts arguably can't match in brand conscious markets such as China.