By Alpha Beta Strategy and Economics, republished with permission

Resource exports still tanking

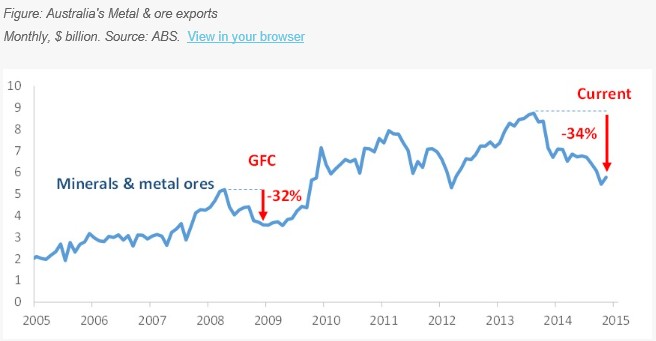

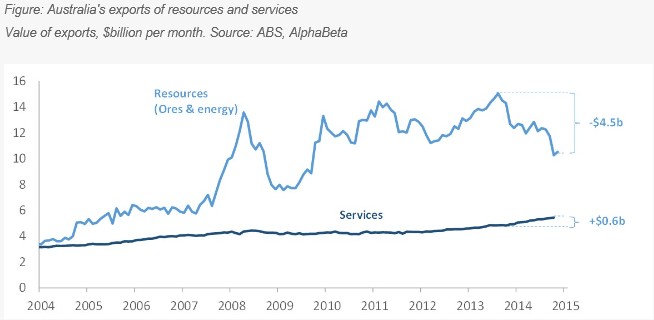

Australia’s trade data released yesterday shows that our resources exports are in serious trouble. The news coverage has positively reported that our ‘trade deficit shrank in May’. But the lift in our exports this month was less than 1% and a blip compared to the shellacking our exports have received over the last 15 months. Our key minerals exports have plummeted 34 per cent since their peak – that’s a bigger fall than the GFC slump in 2008.

What will fill the gap?

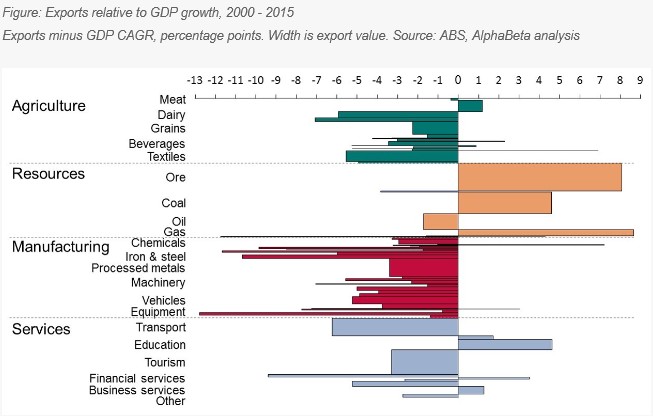

As the resources tide goes out, the big question for Australia is: What will we fall back on? Unfortunately, during the mining boom, we allowed most of the rest of our export base to wither. As the chart below shows, our exports have gone backwards as a proportion of our economy over the last 15 years in almost every non-resources industry.*

The narrowest export base in 50 years

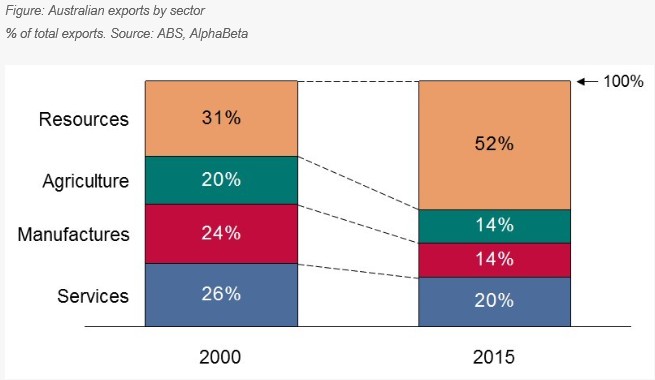

In 2000 less than one third of Australia’s exports came from resources, but today more than half is made up of just three commodities. IMF data shows that Australia’s exports are now more concentrated than they have been for more than 50 years.* We have the narrowest export base since the Korean War wool boom in the 1950s.

Is Australia still a developed country?

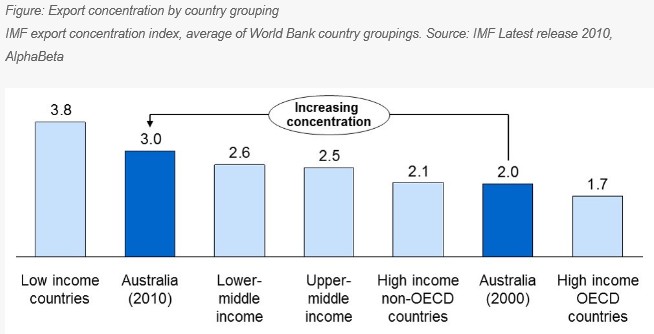

Our extreme dependence on bulk commodities is almost unique among advanced economies. Before the boom, Australia’s export concentration was broadly in line with other similar high income countries. But by 2010 our export concentration had soared. Today our exports are more concentrated than the average of even the middle income countries. And even some low income countries like Nepal, Kenya, and Tanzania have greater export diversity than Australia.

Is Australia still a developed country? Of course we are. We have one of the highest per-capita income levels in the world. But it should be very concerning that, measured by our export base, we have more in common with the banana republics than the high income countries.

What’s wrong with export concentration?

Is it healthy to have such a concentrated export base? David Ricardo showed a century and a half ago that countries should specialize, not diversify. And while the prices of iron ore and coal were skyrocketing, most Australians took the view that if we can make more money selling iron ore than manufactured goods, then so be it. Farewell Ford! Bye bye Alcoa! Sayonara Toyota!

In this spirit, Australia watched idly as the rust-belt manufacturing suburbs around Sydney and Melbourne were transformed from red-brick factories into red-hot real estate. As our share portfolios grew in value, we didn’t worry that the index came to be dominated by a handful of bulging finance and mining giants.

But now that commodity prices are coming down, the real costs of Australia’s export concentration are becoming clear.

For one thing, our economy is now heavily exposed to the volatility of commodity prices. Our nominal GDP has become a roller-coaster, rising dramatically in the decade to 2012 but now stuck in a sustained slowdown. And our federal budget is now hostage to global iron ore markets, with a $10 price change able to rip up to $10 billion from forecast revenues.*

Second, as the growth in mining exports fades, we don’t seem to have much to fill the gap. It’s hard to revive manufacturing exports once plants have closed down, skilled workers have left and customer relationships are lost.* And after a decade of stagnation, services are now too small to offset falling resources exports.

What is to be done?

Australia needs stronger economic policy. Over the last decade our economy was underpinned by a temporary boom in commodity prices and an unsustainable rise in public and private leverage. We have allowed ourselves to become seriously indebted, dangerously exposed to commodity prices and stuck in a rut of low domestic growth and falling export prices.

For a decade, Australian governments have been operating on the assumption that, once the mining boom passed, low interest rates and a falling dollar would be enough to bring the non-resource sectors dancing out of their graves. Unfortunately, no such resurrection is occurring.

As the report we release today explains, many countries are using industry policy to re-balance and re-energise their economies. But in Australia industry policy, as the Productivity Commission reminded us last week, is regarded by many as economic heresy.*

Our report argues that industry policy can be effective, but it must be guided by practical experience of what works to help business flourish, not the result of a messy compromise between rent-seekers and purist bureaucrats.

Click here to read the AlphaBeta report: Rethinking Industry Policy: Seven rules for pro-competitive, pro-globalisation industry policy