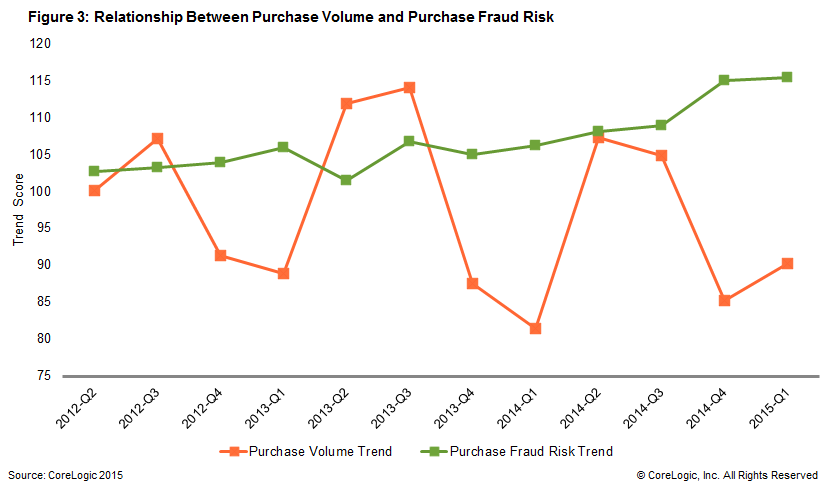

A new analysis by CoreLogic shows an increased risk of mortgage application fraud associated with purchase loans while loans made for refinancing are showing decreased risk. Thus, as rates rise and refinancing diminishes, fraud can be expected to rise as well.

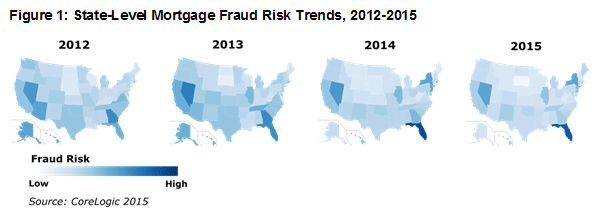

The company, which has tracked fraud since 2010, said that application fraud has increased in Florida, New Jersey and New York by more than 20 percent since 2012 and to a lesser extent in Nevada, Illinois and California. According to its Mortgage Application Fraud Index, Fraud has decreased in most of the rest of the country, notably in Arizona and Georgia (down 36 percent and 26 percent respectively. Nationwide, however, fraud is increasing and is becoming more prevalent in larger metropolitan areas, especially in the Northeast and Southeast.

CoreLogic says that Orlando and Miami have always been hot spots for mortgage fraud but it was nearly non-existent in New York and New Jersey in 2012. Since then fraud has begun to concentrate around NYC and Atlantic City and they as well as the two Florida cities have seen increased risk.

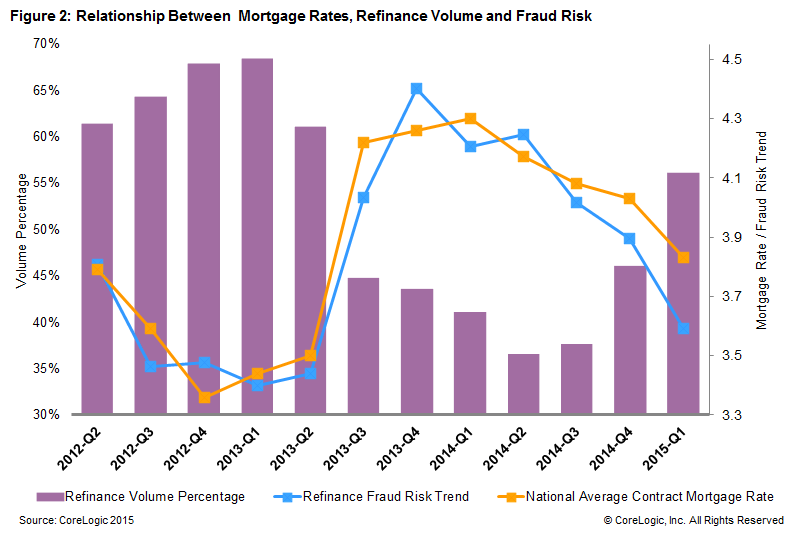

The company said its analysis has found that application fraud risk increases with purchase loans and decreases with refinance loans. This is directly linked to the quality of borrowers most likely to be found with each. When the share of purchase loans rise so does the risk of fraud. The risk thus also correlates to interest rates; as rates drop the number of refinance loans and their associated higher quality of borrowers increases as well and the risk of fraud drops.

CoreLogic says its data shows that mortgage application fraud risk is a consistent problem facing the industry and risk trends will continue to be tied to mortgage rates. "As mortgage rates rise above 4 percent from all-time historic lows, more borrowers will likely pursue purchase loans, which, in turn, will increase fraud risk at the national, state and local levels."