BHP and RIO have both stated a wish to maintain a solid A rated balance sheet. A detailed analysis of the credit rating methodologies suggest that the solid A credit ratings for both companies are at risk, with BHP’s A+ rating almost certain to suffer from a downgrade in the next 12 months. The size of the respective progressive dividends, and more importantly the resulting impact on leverage and cash flow coverage metrics, is the key pressure point on credit ratings. We note that at spot prices neither company is likely to sustain an A rating under S&P’s methodology for more than 18 months, suggesting a change to the progressive dividend policies of both BHP and RIO is possible next year if spot prices persist.

Current ratings look more secure under Moody’s

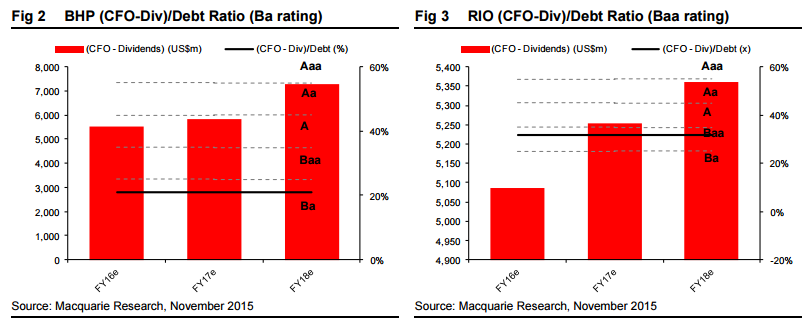

A detailed analysis of Moody’s methodology suggests the credit ratings for BHP and RIO are secure, and are unlikely to see a downgrade on our base case commodity price forecasts. In fact both companies score very highly on most measurements and RIO could actually see an upgrade in its rating should our forecasts become Moody’s base case. For both BHP and RIO the lack of free cash flow coverage on dividends is the key negative when assessing the future credit rating. However BHP and RIO could add at least US$4-5bn of debt without impacting the key credit rating metrics.

A downgrade for both looks likely under S&P

Standard and Poor’s (S&P) methodology paints a much harsher picture for BHP and RIO, as indicated by its negative credit watch rating on both companies. S&P have recently reaffirmed BHP’s A+ (negative long-term outlook) rating and currently assess RIO as A- (negative long-term outlook). On our base case forecasts we expect that BHP could suffer consecutive downgrades to A- over the span of 12-24months, whilst RIO could be downgraded to BBB+. We estimate that with a copper price of US$3.00/lb (real), the oil price would need to average >US$100/bbl and iron-ore >US$60/t for BHP to meet the 50% FFO/Debt ratio between FY16-FY17 required to avoid a credit rating downgrade from A+. Likewise we expect that RIO would require >US$60/t iron-ore at a copper price of US$3.00/lb to avoid a downgrade under S&P’s methodology.

At spot prices progressive dividends are not sustainable

Unsurprisingly, assessing the credit ratings of BHP and RIO using spot prices is likely to trigger downgrades. Assuming spot prices, BHP’s rating would likely suffer consecutive downgrades to A-/A3 over the next 12-24 months, with RIO likely to be downgraded to BBB+ under S&P but retain its A3 rating under Moody’s. At spot prices cuts to BHP’s progressive dividend policy seem inevitable under both methodologies as BHP would be required to reduce net debt substantially to maintain its A credit rating. Likewise RIO would also be required to deleverage under S&P’s methodology, although its credit rating still appears secure under Moody’s.

And Macquarie’s forecast commodity prices are still far too high…

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.