The ongoing problems at Twitter (TWTR) are fairly easy to identify and really illustrate why TWTR has gone from Wall Street favorite to half the valuation of LinkedIn (LNKD) stock.

While LNKD is largely considered a niche company, operating in the jobs industry, it has clearly been the superior company, with LinkedIn stock sure to remain superior to TWTR for a long time to come.

While LNKD is largely considered a niche company, operating in the jobs industry, it has clearly been the superior company, with LinkedIn stock sure to remain superior to TWTR for a long time to come.

The Difference Between TWTR and LNKD

Twitter has constant turnover with management, and its current CEO is also the chief at another company, Square, that is reportedly prepping for an IPO.

Thus, there are serious concerns that Jack Dorsey is not as dedicated to TWTR as he should be, thereby causing doubt that he will actually get the company back on track.

And lastly, TWTR can’t seem to grow its user base at an acceptable pace, causing concerns over longevity.

Meanwhile, LNKD’s user base continues to surge, which remains the best metric of future success for a social media company. During Twitter’s third quarter, it finished with 307 million monthly active users excluding SMS fast followers, a gain of 10 million MAUs since the end of last year, and growth of just 1% sequentially.

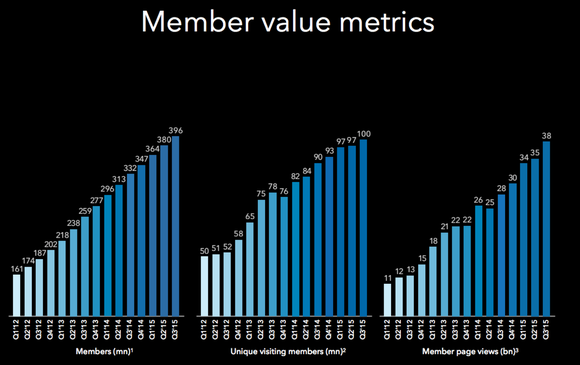

LNKD had 396 million MAUs to end Q3, and has since topped 400 million. That’s an increase of 53 million MAUs since the end of last year, and 5.2% growth sequentially.

LNKD Has a Superior Business Model

Theoretically, a social media’s sequential and annual MAU growth should slow as it grows larger, yet LNKD’s MAU growth is far faster than the smaller TWTR. And while Twitter’s revenue growth has surged following an overload of advertising products to monetize its business — thus pushing ads on users — LNKD is growing in a far more valuable area for the future of its business: engagement.

During the third quarter, LinkedIn had 38 billion member page views. This is up 35.7% from the 28 billion in Q3 of 2014. With member page views growing faster than MAUs, it suggests that engagement is improving. This fact likely played a large role in why LinkedIn’s revenue grew 37.3% year-over-year.

With that said, some investors will correctly point to the fact that TWTR is growing revenue faster than LNKD.

While true, TWTR’s revenue is 100% advertising, a very congested market where just about every dotcom social media platform creates revenue. Therefore, advertisers have many choices, and monitor what platforms are growing the fastest, have the highest engagement, and the best delivery of ads to users. Therefore, TWTR’s lack of diversity in how it creates revenue is a natural risk.

Meanwhile, LNKD is very diversified in how it creates revenue, adding yet another reason why LinkenIn stock is superior to TWTR. LNKD’s ad revenue accounted for only 18% of the total during its third quarter, meaning it is not as dependent on ads to drive business growth. LinkedIn creates another 18% of its revenue from subscriptions, premium memberships where users are willing to pay extra for increased access to employers and connections.

The rest of LNKD’s revenue comes from Talent Solutions, money paid by corporations who rely on LinkedIn’s human resource services to find talent, post jobs and separate talent. This business saw 46% revenue growth, faster than overall growth, and with 40,000 hiring accounts to end Q3, it certainly seems that Talent Solutions will continue to grow for LNKD.

LinkedIn Stock Is the Way to Go

With that said, LinkedIn is only able to create so much revenue outside of advertising, and grow so quickly, because it has an identity. LNKD is the quintessential face of human resources and job seekers, where just about everyone goes to hire, seek employment and network professionally. LinkedIn has embraced this identity, whereas TWTR is known for being complicated to use.

Collectively, LNKD is growing MAUs faster than TWTR, it has stable leadership, a business identity, and does not compete with advertising juggernauts Google (GOOG, GOOGL) and Facebook (FB) for its core business.

Last but not least, LinkedIn is also profitable, having $190 million in free cash flow over the last year versus a loss of $8.5 million for TWTR.

So for investors who want to own a social media stock outside of Facebook, LinkedIn stock certainly looks like the way to go.

As of this writing, Brian Nichols did not hold a position in any of the aforementioned securities.