Things are looking bright for Boeing and Co (BA) the U.S.-based jetliner manufacturer. Orders for passenger planes, as well as military helicopters, have been steadily building.

At the same time, the company is making good headway in increasing its capacity to meet that rising demand. But this brightening outlook carries with it both good news and bad news for Boeing stock.

At the same time, the company is making good headway in increasing its capacity to meet that rising demand. But this brightening outlook carries with it both good news and bad news for Boeing stock.

Let’s start with the good news: The brightening outlook for Boeing is not fully priced in Boeing stock. That means there is more near-term upside for BA stock as we come into the year’s end.

The bad news: In order to keep up with demand and grow the business Boeing accumulated a high debt burden. Once growth in the aviation sector slows Boeing’s balance sheet could come under pressure.

Boeing Stock Has an Upside

Every time the aviation industry enters a growth cycle investors flashback to the ‘90s. That was when rapid expansion among air carriers ignited a price war. For those that couldn’t keep up, that meant Chapter 11 bankruptcy.

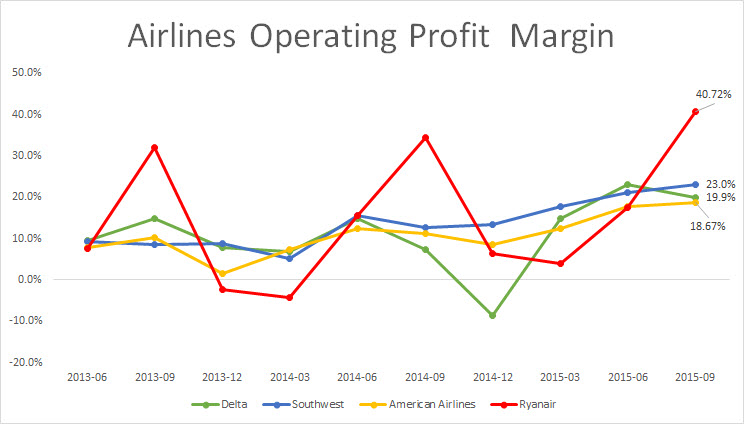

So it comes as no surprise that the current industry expansion is raising some concerns among Boeing stock holders. They fear that another aviation crunch could ignite a cancelation of orders.

Yet this time around things seem to look a bit different. When analyzing the operating profit margins of four of Boeing’s largest customers in civil aviation we learned something. The data suggests that, at the moment at least, there is no pricing war. As can be seen in the chart, all of the four major air carriers have experienced expanding operating profit margins. If there was a price war, operating margins would have been shrinking not expanding.

Click to Enlarge

Projections from the International Air Transport Association suggest that air travel is likely to continue and expand. Thus we have a bright outlook for airlines which are experiencing both a rise in volumes and in margins.

It’s no surprise, then, given that outlook that Boeing’s order book swelled to a massive $485 billion. More profitable airlines means that demand for passenger jets will also rise. And that means that Boeing’s pricing power could be getting stronger.

This has already had a tangible effect on Boeing’s bottom line. The company raised its 2015 revenue target to $95 to 97 billion and GAAP EPS to $7.60 to $7.80. Yet, for Boeing stock, this improved outlook hasn’t been fully priced in.

Boeing’s historical price-to-earnings ratio averages 20, but Boeing stock is trading at an 18 times earnings. Boeing’s bottom line is on a rising trajectory and set to become more profitable.

Thus a solid case can be made for BA stock to trade at its long-term average of 20 times earnings. Especially when you consider that the aviation business is set to continue and expand.

The Long-Term Risk for Boeing Stock

But with that rapid expansion there is also risk. In order to keep up with demand Boeing had to invest a lot in raising its capacity. And that capacity is likely to increase to more than 65 planes a month by 2017.

The problem however is that Boeing had to take it upon itself plenty of debt to keep up with growth of the business. Currently, Boeing’s debt-to-equity ratio is 125%. Compare that to, say, General Dynamics Corporation (GD), a Boeing peer, which has a debt-to-equity ratio of a mere 40%.

In the event of a sudden crisis, Boeing’s balance sheet could come under pressure, making its debt difficult to manage. Though there doesn’t appear to be any significant crisis looming, bear in mind this is an era of uncertainty. One such potential risk could be if terror threats force the airlines to invest in additional security. That would certainly weigh on their bottom line and curb airlines’ purchasing power.

Bottom Line on BA Stock

Though the risks to long-term debt are real, they won’t necessarily materialize. At the moment, possible hurdles for the aviation industry have not yet been felt. Therefore, there’s no immediate need or reason for concern on Boeing stock.

However as long as Boeing’s long-term risks don’t turn into an imminent threat the growth outlook still in place.

Given that , on the short-term Boeing stock is set to trade back at its historical multiple of 20 times earnings. Which pins down $164 as the short-term target for Boeing stock.

As of this writing, Lior Alkalay did not hold a position in any of the aforementioned securities.