Andrea Riquier is a New York-based writer covering mortgages and the housing market for Forbes Advisor. She was previously at Dow Jones MarketWatch, on the housing market and financial markets beats. Before that, she covered macro and central banks for Investor's Business Daily, and municipal bonds for Debtwire.

Kiah Treece is a small business owner and personal finance expert with experience in loans, business and personal finance, insurance and real estate. Her focus is on demystifying debt to help individuals and business owners take control of their finances. She has also been featured by Investopedia, Los Angeles Times, Money.com and other financial publications.

Andrea Riquier,

Andrea Riquier is a New York-based writer covering mortgages and the housing market for Forbes Advisor. She was previously at Dow Jones MarketWatch, on the housing market and financial markets beats. Before that, she covered macro and central banks for Investor's Business Daily, and municipal bonds for Debtwire.

Kiah Treece

Kiah Treece is a small business owner and personal finance expert with experience in loans, business and personal finance, insurance and real estate. Her focus is on demystifying debt to help individuals and business owners take control of their finances. She has also been featured by Investopedia, Los Angeles Times, Money.com and other financial publications.

Chris Jennings is a writer and editor with more than seven years of experience in the personal finance and mortgage space. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. His work has been featured in a number of outlets, including Yahoo Finance, MSN, Fox Business, and GOBankingRates.

Reviewed

Chris Jennings

Chris Jennings is a writer and editor with more than seven years of experience in the personal finance and mortgage space. He enjoys simplifying complex mortgage topics for first-time homebuyers and homeowners alike. His work has been featured in a number of outlets, including Yahoo Finance, MSN, Fox Business, and GOBankingRates.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

If you’re looking for a lump sum of money to help renovate your home, consolidate debt or cover another major expense, then a home equity loan might be a good option. Forbes Advisor compiled a list of the best home equity loan lenders based on their starting interest rate, average closing time and other factors pertinent to a satisfying borrower experience.

Read more

Show Summary

- Featured Partner

- Best Home Equity Loan Rates April 2024

- TD Bank

- Navy Federal Credit Union

- BMO Harris

- Connexus

- Discover

- Fifth Third Bank

- US Bank

- Summary: Best Home Equity Loan Rates

- Current Home Equity Loan Rates

- How Does a Home Equity Loan Work?

- What Can I Use a Home Equity Loan For?

- How To Apply for a Home Equity Loan

- Alternatives to a Home Equity Loan

- Methodology

- Frequently Asked Questions (FAQs)

Best Home Equity Loan Rates April 2024

- TD Bank: Best for Home Equity Loan Rate Overall

- Navy Federal Credit Union: Best for Highest Home Equity Borrowing Limit

- BMO Harris: Best for Loan Amounts

- Connexus Credit Union: Best for Fastest Closing Time

- Discover: Best for Borrowers With Low Credit Scores

- Fifth Third Bank: Best for Customer Friendly Home Equity Loan Products

- U.S. Bank: Best for Real-Time Rate Estimates

Summary: Best Home Equity Loan Rates

| Company | Forbes Advisor Rating | APRs starting at | CLTV | Min. credit score | Learn More | ||||

|---|---|---|---|---|---|---|---|---|---|

| TD Bank |  |

5.0 |  |

7.99% | 89.99% | 740 | Compare Rates | Compare rates from participating lenders in your area via Bankrate.com | |

| Navy Federal Credit Union |  |

4.0 |  |

7.34% | 100% | Did not disclose | Compare Rates | Compare rates from participating lenders in your area via Bankrate.com | |

| BMO Harris |  |

3.5 |  |

8.19% | 89.99% | 700 | Compare Rates | Compare rates from participating lenders in your area via Bankrate.com | |

| Connexus |  |

3.5 | |

7.20% | 90% | 640 | Compare Rates | Compare rates from participating lenders in your area via Bankrate.com | |

| Discover | 3.0 |  |

8.49% | 90% | 620 | Compare Rates | Compare rates from participating lenders in your area via Bankrate.com | ||

| Fifth Third Bank |  |

3.0 |  |

8.50% | 90% | 660 | Compare Rates | Compare rates from participating lenders in your area via Bankrate.com | |

| US Bank |  |

3.0 | |

8.40% | 80% | Did not disclose | Compare Rates | Compare rates from participating lenders in your area via Bankrate.com |

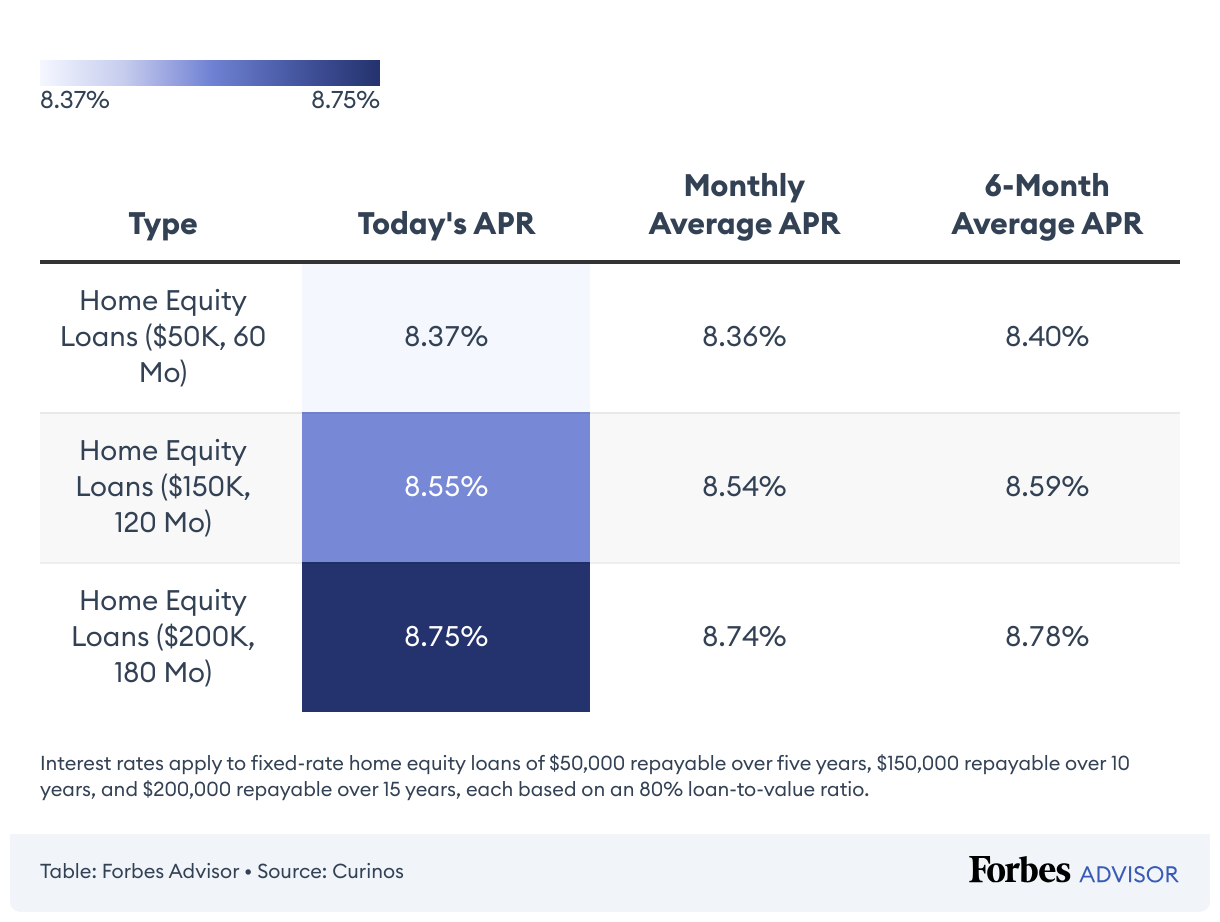

Current Home Equity Loan Rates

How Does a Home Equity Loan Work?

You can generally borrow up to 80%—sometimes 85%—of your home’s value, depending on the lender and your financial profile.

Home equity loan rates are fixed, meaning your interest rate won’t change over the course of your loan; you’re expected to repay both principal and interest in monthly installments. Repayment terms typically range from five to 30 years, but lenders tend to offer better rates to borrowers who choose shorter terms and have higher credit scores.

You’ll have to pay fees and closing costs between 2% and 5% of the total loan amount. Some lenders might waive these additional costs.

Discover Home Equity

Interest Rate:

Above national average

Minimum Credit Score:

620

Compare Rates

Compare rates from participating lenders in your area via Bankrate.com

Above national average

620

Pros & Cons

- No application fees, loan origination fees, appraisal fees or closing costs

- Offers cash-out refinancing up to $300,000

- Allows you to borrow against almost 90% of your equity

- Can complete all or nearly all of the application process online

- Only offers refinancing and home equity loans

- Doesn’t offer home equity products in certain states or in any U.S. territories

- Might charge prepayment penalties up to $500 if you repay your loan early

- Takes an average of 6 to 8 weeks to close on a loan

What Can I Use a Home Equity Loan For?

If you’re approved, you’ll receive a lump sum to use how you wish. Many people use home equity loans to fund:

- Home improvements

- Debt consolidation

- College tuition

- Medical bills

- Emergency expenses

- Major purchases (such as a new car or wedding)

- Vacations

How To Apply for a Home Equity Loan

- Understand your current financial situation. Like with most loans, you’ll need good to excellent credit (a credit score of at least 680) as well as a stable income and a low debt-to-income (DTI) ratio to qualify.

- Determine how much home equity you have. You must have enough equity in your home—typically at least 20%—to be eligible for a home equity loan. Take your remaining mortgage balance and subtract it from your home’s estimated market value to get a rough idea of how much equity you have.

- Compare lenders and interest rates. Once you have an idea of how much you want to borrow and the amount of equity you have in your home, start looking at several different lenders. Compare at least three to five lenders before settling on a single loan to get the best deal.

- Submit your application. When applying for a home equity loan, you’ll need to supply your lender with several key documents and pieces of information. This includes your Social Security number, current mortgage statement, two years’ worth of W-2s, bank statements and tax returns.

- Get your home appraised. Your lender will likely order an appraisal to confirm your home’s value. This helps them determine how much you can borrow.

- Sign your closing documents. Once you’ve had your home appraised and your loan approved, you’ll review and sign all the closing documents with your lender. You’ll also pay any closing costs—although some lenders waive closing fees on home equity loans. The lender will then finalize your loan, and you’ll receive your funds once the three-day right of rescission period ends.

Alternatives to a Home Equity Loan

Home equity can be a powerful tool for homeowners needing to finance significant expenses. However, a traditional home equity loan might not always be the best or available option. These are some popular alternatives to home equity loans.

- Cash-out refinancing. Cash-out refinancing involves refinancing a mortgage for more than the outstanding balance and taking the difference in cash. This is best for borrowers who can secure a lower interest rate than their current mortgage and want to consolidate debt.

- Personal loans. Personal loans are unsecured loans that don’t require home equity and are based on creditworthiness. This option is typically best for borrowers with strong credit who need funds quickly and don’t want to use their home as collateral.

- Credit cards. Credit cards offer revolving credit that borrowers can use for various purchases, with some providing 0% introductory annual percentage rate (APR) offers. These are ideal for those who prefer short-term borrowing and can take advantage of promotional interest rates.

- Retirement account loans. Certain retirement accounts allow individuals to take loans against their saved retirement funds. A 401(k) loan is one popular example. These are suitable for borrowers with substantial retirement savings and who are confident in their ability to replenish the funds.

- Life insurance loans. A life insurance loan is a type of financing taken out against the cash value of a life insurance policy. This form of financing is suitable for policyholders with a whole-life policy that has built up cash value, offering a low-interest option without a credit check.

- Peer-to-peer lending. Unlike traditional financial institutions, peer-to-peer (P2P) lending connects borrowers directly with investors through online platforms. P2P lending is a good option for borrowers with good credit who want a more personal borrowing experience and competitive interest rates.

Methodology

We reviewed a dozen home equity loan lenders for customers across the nation. Lenders that do not display their interest rates online or decline to respond to emails or calls from reporters are not eligible for the list.

We scored lenders primarily on the basis of their interest rates but also included additional information that’s important to borrowers, such as time to close and amount you can borrow as well as offered discounts or promotional rates.

The score is weighted among the following loan and lender features:

- Interest Rate: 50%

- Maximum Combined Loan-to-value Ratio: 20%

- Closing timelines: 20%

- Credit Score: 10%

Bonus points: Lenders who offer some kind of discount (usually for a banking relationship) are eligible for five bonus points.

To learn more about our rating and review methodology and editorial process, check out our guide on How Forbes Advisor Reviews Mortgage Lenders.

Frequently Asked Questions (FAQs)

What is a home equity loan?

Home equity loans allow homeowners to borrow against the equity in their homes. Equity is the difference between your home’s value minus what you owe on your mortgage. Tapping your equity through a home equity loan is just one way to access it, and unlike some types of loans, it will allow you to get the full amount upfront. But to make sure it’s worth the cost to finance, it’s important to first calculate how much you will pay in interest.

Home equity loans are popular among borrowers who want to use the funds to cover large expenses, such as home improvement projects or high-interest debt consolidation.

How do I calculate how much equity is in my home?

A rough rule of thumb is that the amount of equity you have in your home is the home’s value minus any outstanding loans on the property, like your mortgage. You can use our home equity loan calculator for a more precise calculation.

How does a home equity loan differ from a home equity line of credit (HELOC)?

Home equity loans and HELOCs are both technically second mortgages on your home. A home equity loan allows you to get a lump sum of money all at once and then repay it over time, while a line of credit gives you access to a revolving credit line that you can tap into, repay and tap again over a period of years.

Home equity loans are often a better option if you know the amount you need already—say for a child’s education or a home construction project. That’s because when you get the money all at once, you repay it according to a fixed interest rate. In contrast, a home equity line of credit offers a lot more flexibility and the ability to take some or all of the money over time—but you pay for that flexibility by agreeing to a variable interest rate that could rise, in some cases substantially, over the life of the credit line.

How do I calculate my combined loan-to-value ratio?

Your CLTV ratio is the sum of anything you owe on the house—say a mortgage and a home equity loan—divided by the value of the property. Most lenders prefer you to borrow no more than 80% of your CLTV, but some will go up to 90%.

How long does it take to get a home equity loan?

The more organized you are, the faster you will be able to get a home equity loan. So make sure you have all the required documents before applying. There will be factors, such as the timing of the home appraisal and underwriting process, that might not be under your control.

In a best case scenario, you could close on your home equity loan in a couple of weeks. However, it’s not uncommon for this process to take up to two months.