How federal stimulus accidentally bottlenecked affordable housing in DC

The Westerly in Southwest DC. Image by Hoffman & Associates. Used with permission

This is the third in a series of posts about how affordable housing works, by an affordable housing developer. Read all the previous posts here: Affordable Howsing.

In the first two columns of this series, I explained the general financing sources needed to build income-restricted homes for low-income households and the District of Columbia’s primary specific financing tool, the Housing Production Trust Fund.

This column focuses on a major new challenge facing local affordable housing development projects: the District’s recent crash into the federal limit on private-activity bond issuance, known as the “volume cap” or “bond cap.” This issue has sent shockwaves through the District’s affordable housing industry and abruptly brought many projects to a halt.

Pairing private-activity bonds and Low-Income Housing Tax Credits

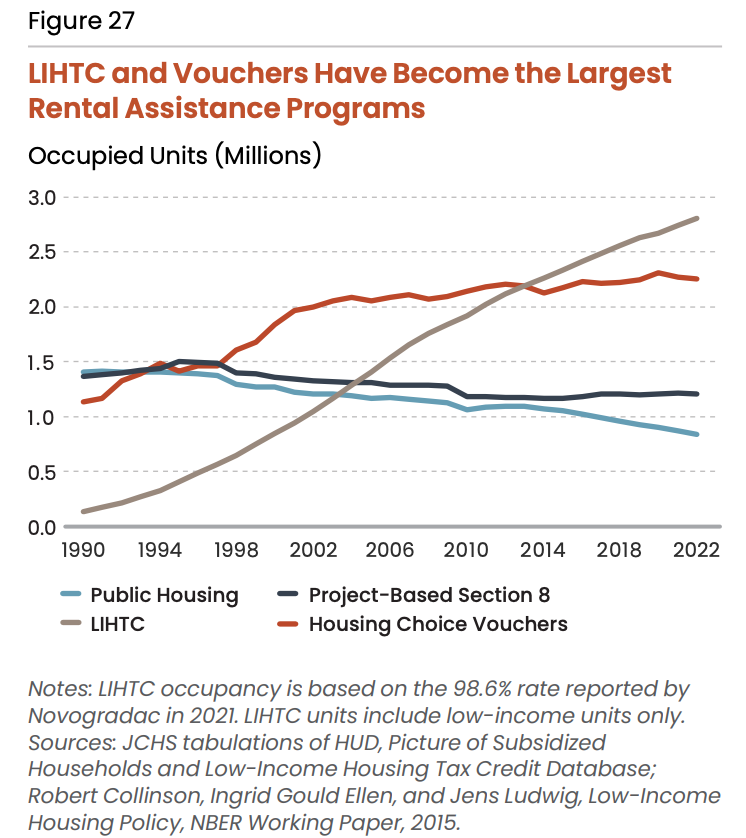

As I explained in my first column, the federal 4% Low-Income Housing Tax Credit (LIHTC) program, which was created in 1986 and allows investors to fund affordable housing developments in exchange for a deduction in their corporate tax liability, has become the predominant federal funding program for affordable housing. A recent report from the Harvard Joint Center for Housing Studies illustrates how the program has steadily increased since its inception, surpassing public housing, project-based Section 8 (rental assistance payments tied to privately owned buildings), and Housing Choice Vouchers (rental assistance payments tied to tenants for use in the private market) to become the largest affordable housing program in the country by total unit count.

Source: Harvard Joint Center for Housing Studies, “The State of the Nation’s Housing 2023”

Low-Income Housing Tax Credits are divided into two categories: 9% LIHTC and 4% LIHTC. 9% LIHTC provide an annual tax credit worth 9% of eligible costs for 10 years (so a total tax credit worth 90% of eligible costs). 4% LIHTC provide an annual tax credit worth 4% of eligible costs for 10 years (so a total tax credit worth 40% of eligible costs). Because not all project costs are tax credit-eligible costs, most notably the cost to purchase the land, in practice 9% LIHTC cover less than 90% of total project costs (closer to 70%) and 4% LIHTC cover less than 40% of total project costs (closer to 30%).

The 9% LIHTC program is therefore designed to cover most of a project’s costs and is generally reserved for smaller projects that generate little revenue because they target very low-income households or other special-needs individuals. These credits offer a large amount of federal subsidy on a per-unit basis, which is necessary because the projects can support very little debt due to the lack of operating income. Each state receives a fixed allocation of credits from the federal government to award to projects on a competitive basis.

The 4% LIHTC program is designed to cover a smaller portion of a project’s total cost, with other funding sources needed to fill the gap. These projects generally have higher rents and therefore have more stable operating income, so they can take on more debt than 9% LIHTC projects. As a result, the federal government offers less subsidy on a per-unit basis for these projects, and state and local governments step in to fill the gap with local funding programs like the District’s Housing Production Trust Fund. It is common for 4% LIHTC affordable housing projects to have three main funding sources: 4% LIHTC equity, mortgage debt, and subordinate debt or grants from state and local government, like the District’s Housing Production Trust Fund.

While 9% LIHTC is funded by direct allocation from the federal government, there is no direct allocation for the 4% LIHTC program. This means that, in theory, 4% LIHTC is an unlimited tax credit that any qualifying project is allowed to claim (similar to the new tax credits for clean-energy projects in the Inflation Reduction Act). But this is not the case in practice. Real estate and construction make up an enormous portion of the U.S. economy, together accounting for $4.4 trillion in 2023, equivalent to 16% of Gross Domestic Product. To have an unconstrained tax credit available for such a large market runs the risk of creating an enormous cost for the federal government. To avoid this problem, Congress created an indirect mechanism for limiting the 4% LIHTC program, by requiring credits to be paired with private-activity bonds.

Private-activity bonds are a type of municipal bond where a state or local government issues bonds on behalf of a private-sector borrower. These bonds are generally revenue bonds, meaning that they are intended to be paid back from revenues generated specifically by the project. The bonds are used to pay for construction and then are paid back either upon construction completion, via refinancing, or long-term out of the project’s cash flows. For affordable housing projects in the District, the government entity that issues the bonds is the DC Housing Finance Agency (DCHFA), with affordable housing developers acting as the private sector borrowers.

For affordable housing projects to receive an allocation of 4% LIHTC, developers must use private-activity bonds to pay for at least 50% of total project costs, which include acquisition, construction, design costs, and other eligible expenses. If a project meets this threshold at the end of construction and lease-up, which is when units are occupied and tenants’ incomes have been verified, it is eligible to begin receiving the tax credits. If a project does not meet this threshold, it cannot receive any tax credits. Receiving a bond allocation prior to construction is thus a key requirement for a 4% LIHTC project to move forward.

Private-activity bonds are tax-exempt, which provides a significant incentive for investors to purchase the bonds but also an additional cost to the federal government. To limit this cost, Congress sets a ceiling, or “volume cap,” on the amount of private-activity bonds states can issue annually. This amount is set on a per-capita formula updated annually by the IRS, with a special “small-state minimum” level for jurisdictions with low populations such as Wyoming, Vermont, and the District of Columbia. This means that each state must keep its annual bond issuance at or below the volume cap, or risk jeopardizing the tax-exempt status of the bonds. Private-activity bonds can be issued for a variety of activities, such as water, sewer, and transportation infrastructure, but multifamily affordable housing programs tend to be a primary use.

Because affordable housing projects can only qualify for 4% LIHTC through the use of private-activity bonds, the volume cap thus acts as a de facto limit on the 4% LIHTC program. Without bonds, projects cannot use 4% LIHTC. Historically this was not a major issue for most states, but as the LIHTC program has grown over time, bond issuance for housing projects increased correspondingly.

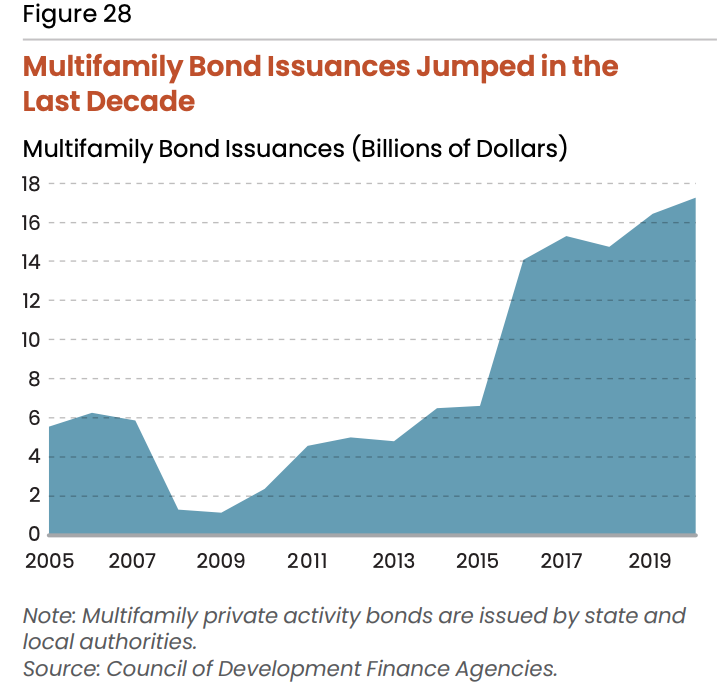

Source: Harvard Joint Center for Housing Studies, “The State of the Nation’s Housing 2023”

As the above graph shows, after a brief lull following the 2008 financial crisis, private-activity bond issuance for housing projects steadily rose during the 2010s as LIHTC was emerging as the largest federal affordable housing program in the country. By the end of the decade, an increasing number of states were hitting their volume cap, and concerns were growing about the eventual impact on the affordable housing development industry. These concerns quickly came to a head with the onset of the Covid-19 pandemic.

Pandemic-supercharged bond issuance

After a brief downturn in early 2020, the affordable housing development industry roared back to life as the economy bounced back. However, like many other sectors of the economy, the industry was then hit by profound economic shocks. The supply-chain crisis and soaring construction costs caused project expenses to skyrocket, leading to a major increase in the bonds needed per project to meet the 50% minimum threshold. Low-interest rates caused rents and land values to surge, further increasing the bonds needed per project. At the same time, Congress approved several stimulus measures directly aimed at supporting the affordable housing industry, which helped to juice demand for bonds. The December 2020 stimulus bill established a “minimum credit rate” for 4% LIHTC that increased the amount of tax credits available per project. The March 2021 stimulus bill included $350 billion in flexible funding for state and local governments, a large portion of which was invested in local affordable housing initiatives.

This combination of increasing costs and a surge in federal and local spending brought the volume cap issue from a simmer to a full-on boil. By late 2021, LIHTC experts were warning state governments and the affordable housing development industry that volume cap was becoming an increasing challenge nationally, throwing sand in the gears of efforts to build and preserve affordable housing across the country.

DC hits volume cap, projects grind to halt (or, Bitty Bitty Bond Bond)

The District of Columbia has not been immune to these national challenges. The volume cap issue was apparent even prior to the pandemic. In 2019 industry experts warned that the District’s 2018 multifamily private-activity bond issuance had exceeded its annual volume cap for the first time; it was only able to do so by “carrying over” unused bond capacity from prior years. But the major catalyst was the District’s unprecedented infusion of cash into the Housing Production Trust Fund during the pandemic. After years of steady annual allocations of $100 million into the Trust Fund from 2015 through 2020, DC allocated $400 million to the fund in 2021 and $444 million in 2022, thanks largely to federal stimulus funds.

This historic investment represented a major effort by the Bowser administration and the DC Council to solve the District’s housing affordability crisis through a massive infusion of capital to preserve and produce affordable housing across the city. Yet the effort almost immediately crashed into the reality of the volume cap. As I explained in my earlier columns, Housing Production Trust Fund financing is intended to be “gap” financing that supplements 4% LIHTC and other federal funding programs. The 4% LIHTC program on its own cannot fully fund a low-income housing project. Local gap financing programs are crucial to make affordable housing projects “pencil out” mathematically, particularly in high-cost jurisdictions. But because these local funding programs work in tandem with 4% LIHTC, an increase in local funding programs means more projects are able to move forward, which leads to an increase in demand for 4% LIHTC. As demand for 4% LIHTC increases, the jurisdiction moves closer to hitting its volume cap. Once the volume cap is reached, increasing funding for local gap financing achieves diminishing returns, as no more 4% LIHTC funds are available and the two programs are no longer able to work in combination. The volume cap on private-activity bonds thus creates a natural limit for the value of local gap financing programs like the Housing Production Trust Fund.

What makes the District unique is its exceptionally large volume cap. As I mentioned earlier, the District qualifies for the “small-state minimum” volume cap for private-activity bonds, rather than the standard per capita formula for most states, including Maryland and Virginia. In 2024, the small-state minimum bond volume cap is $378 million. Based on the standard per-capita formula ($125 per person), the District’s bond volume cap would be $85 million. Thus, due to its small population, the District actually has a per-capita volume cap 4.4 times larger than most states, meaning that it has access to 4.4 times more per-capita 4% LIHTC funds. This is an enormous and unique benefit of the program to DC. The fact that the District has reached even this uniquely high volume cap threshold is a testament to just how much the city has invested in affordable housing in recent years.

Unfortunately, the abrupt hitting of the volume cap has thrown numerous affordable housing projects in the city into turmoil. In January 2023, the DC Housing Finance Agency announced a new competitive selection process for projects planning to use 4% LIHTC and private-activity bonds, replacing the traditional rolling application process where most projects meeting threshold eligibility requirements could proceed on a flexible timeline. In August 2023, the DC Department of Housing and Community Development (DHCD) announced in its annual Consolidated Request for Proposals for Affordable Housing Projects (RFP) that projects planning to utilize 4% LIHTC could no longer apply for HPTF financing, with no estimate of when the freeze will be lifted. Together, these announcements represented a major paradigm shift for affordable housing projects in the District.

Based on the reality of limited federal funds, high demand for affordable housing projects, and the existing backlog of projects that received HPTF funding but are waiting to receive bonds, introducing a new competitive process to allocate bonds and instituting a temporary freeze are both no-brainers. Yet there are enormous uncertainties remaining about how this new process will work in practice, how large the existing backlog of projects is, how projections for future demand for bonds compare to projections for future volume cap, and when the freeze on pairing 4% LIHTC with HPTF funds might be lifted.

This current level of uncertainty has left affordable housing developers scrambling to salvage projects. As I previously explained, it can take several years to put together the financing sources to start construction on either a preservation or a new-construction affordable housing project. In that interim period, projects incur major costs. For preservation projects, developers often have to acquire properties on an interim basis, using short-term financing sources such as DC’s Affordable Housing Preservation Fund. For new construction projects, developers often have to pay non-refundable deposits to go under contract to acquire land, or even fully purchase the land on an interim basis with short-term, high-interest financing. For both types of projects, development teams must spend significant amounts of money to prepare financing applications, incurring architectural design costs, engineering studies, and other “predevelopment” costs, often using short-term loans.

Without any clarity on the timeline for recouping those costs or paying off these loans, properties are already being forced into foreclosure or forced sales, and businesses and nonprofits run the risk of bankruptcy. As these risks escalate over time, not only will current projects in the pipeline be lost, but new projects will stall out. The result is a precipitous drop in future affordable housing projects, as the current backlog of projects eventually gives way to an empty pipeline—a boom-and-bust dynamic rather than a slow-and-steady industry.

Planning for a new normal (or, the Bonds that Bind)

While the current oversubscription of bonds is not a permanent bottleneck, but rather the result of an unprecedented surge in affordable housing projects during the pandemic era, the likely reality is that the affordable housing development industry will never return to its pre-2020 normality. Even though Congress is currently considering reducing the 50% cost threshold for bonds to 30% on a temporary basis, requiring fewer bonds per project, this would only be a short-term fix to clear some of the immediate backlog. The expectation is that private-activity bond issuance in DC will remain limited and competitive on an indefinite basis.

District policymakers must therefore plan for a different future of affordable-housing financing. First, transparency about the scope of the problem is necessary. The District should publish data outlining its current obligations and projections for future bond issuance, as well as estimates for when the freeze on pairing 4% LIHTC with HPTF will be lifted, so developers, lenders, tenant organizers, and other groups with an interest in affordable-housing production can plan accordingly. This data will be pivotal in understanding the scope of the problem and helping developers to plan realistic timelines for their projects.

Second, DHCD and DCHFA should also commit to greater transparency regarding the competitive scoring process. As I explained in my last column regarding the Housing Production Trust Fund, projects are scored competitively, but those scores are not released publicly, making it difficult for project teams to know how well-positioned any given project is to receive funding in future rounds. Now that the same scoring system is being used for allocating scarce bonds, this issue has become even more paramount. DC should commit to an open and transparent scoring process for projects seeking its funds—something most jurisdictions, including Maryland and Virginia, already have.

Third, the DC Council should focus on a stable equilibrium for investments in the Housing Production Trust Fund, rather than occasional mega-investments that exacerbate boom-and-bust cycles. The Council returned to its $100 million annual baseline in the previous budget cycle, an amount sufficient enough to catalyze a major increase in the affordable housing stock over the long term, provided that the Trust Fund is monitored appropriately so a steady stream of cash from projects is recycled over time. While there should be room to slowly and carefully increase the Trust Fund budget allocation over time, doing so should match annual increases in the District’s private-activity bond volume cap in order to avoid creating future backlogs of bond allocations.

Fourth, the District should explore financing strategies for affordable housing projects that complement the use of 4% LIHTC. Public land dispositions are one such opportunity: surplusing land by selling at below-market rates provides a form of subsidy for affordable housing, and cross-subsidization from market-rate units in mixed-income projects can serve as an alternative to tax credits. However, the math behind such initiatives can be challenging and varies over time given macroeconomic conditions. It is usually impossible for public-land disposition projects to achieve affordability beyond the existing 30% requirement without requiring the use of 4% LIHTC. Property tax abatements are another common tool, but the District is legally required to account for the cost of such abatements in its budget. HPTF funds could be used for homeownership projects, which are not LIHTC-eligible, as well as non-LIHTC market-rate projects to replace equity financing in exchange for buying down rents to affordable levels. This latter approach has worked well in Montgomery County in recent years, albeit in conjunction with a generous tax abatement program. Finally, and perhaps most importantly, zoning reforms to increase the overall housing supply could create more opportunities for new non-LIHTC projects that include cross-subsidization between market rate and affordable units, expanding on the existing Inclusionary Zoning system.

For decades, the affordable housing development industry has operated in a fortunate environment of a steadily expanding LIHTC program unconstrained by the reality of limited federal funds. During this era, the limited supply of local gap financing was the primary concern, and producing and preserving more affordable housing was simply a matter of local jurisdictions finding more money to invest in projects.

Unfortunately, those days are now over. There will be a painful adjustment period ahead, both nationally and in the District, as we adapt to a world of scarcity and greater competition for resources in the post-pandemic era. But the affordable housing development pipeline will slowly right-size and new systems will emerge to prioritize and allocate bonds and tax credits. As we move forward, project quality will now matter more than quantity, creative financing approaches will be necessary, and zoning regulations will need to allow more density to facilitate the production of more affordable housing. Policymakers will need to foster an environment that is transparent, predictable, and easily navigable to those who produce income-restricted subsidized housing. The new era of affordable housing policy and development in the District is just beginning.