The launch of New Zealand's Depositor Compensation Scheme (DCS) has been pushed back again, this time by about nine months to the middle of next year.

Launching the latest consultation paper in the ongoing process of establishing the DCS on Monday, the Reserve Bank said; "Once operational in mid-2025, eligible deposits will be protected up to $100,000 per customer, per deposit taker."

Last year the Reserve Bank said the DCS was expected to come into force in October 2024. And prior to that its launch had been targeted for early 2024.

"The DCS was scheduled to be operational by late 2024. Following the passage of the Deposit Takers Act near the end of the previous Parliament, the time needed to consult on important policy details and implement secondary legislation, as well as feedback received from industry on the timeframes needed to operationalise a robust customer-facing DCS, the Minister of Finance [Nicola Willis] now intends to commence the DCS by mid-2025," a Reserve Bank spokeswoman told interest.co.nz.

"We have continued to build the operationality capability to implement the DCS, and this is on track to be ready by the end of 2024. The additional six months will allow time to successfully launch the DCS to the public."

The DCS will provide protection of up to $100,000 per eligible depositor, per deposit taker in the event of deposit taker failure. It will be funded through the DCS fund, which will be raised by levies charged to deposit takers. (See all our previous stories on the DCS here, and an episode of the Of Interest Podcast on it here).

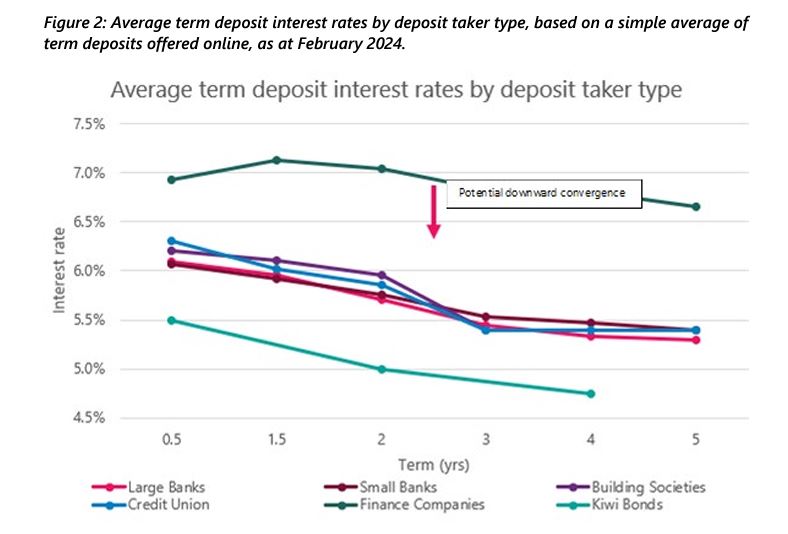

Deposit rate convergence

Meanwhile, in the DCS regulations consultation paper issued on Monday, the Reserve Bank says it expects "some level" of deposit rate convergence across different types of deposit takers, as the perceived risk of deposit takers who previously offered higher deposit rates falls into line with other deposit takers due to the protection available to depositors under the DCS.

"For example, interest rates offered by credit unions and building societies for term deposits are generally around 15 basis points higher than comparable rates offered by the major banks. Finance companies, by comparison, offer a much higher premium, often around 120 basis points higher than those offered by major banks. The DCS levy is expected to narrow, but not fully close, those gaps for deposit takers covered by the scheme," the Reserve Bank says.

Credit card & revolving loan funds may be included

The consultation paper also looks at the proposed scope of protected deposits and entitlement conditions. Protected deposits, as defined by the Deposit Takers Act, are NZ dollar denominated “debt securities,” and include current accounts, savings accounts and term deposits. The Act also allows other products offered by deposit takers to be included or excluded as protected deposits through regulations.

"We propose that the definition of protected deposits include credit balances [money owned by customers to be repaid by deposit takers] of specific lending products [such as] credit cards, revolving credit facilities, revolving home loans, as these can be equivalent to current accounts in substance," the Reserve Bank says.

"We also propose an entitlement condition that ensures depositors cannot be paid twice for the same deposit where funds are recovered by a liquidator."

"We propose that trusts are required to provide prescribed documents. This should support the Reserve Bank to act with certainty when making a payout."

The Reserve Bank notes almost all NZ banks provide revolving loan products including both home loans and credit facilities.

"The available funds are always on call, so they do not have to reapply when they need extra funds. From discussions with industry, we understand that a substantial proportion of revolving loan products are generally in positive balance," the Reserve Bank says.

The consultation paper cites the following example: "After 10 years a customer pays off the amount owing on their revolving home loan, then continues to use the product in credit balance. The product otherwise has the features and capabilities of a current account."

Credit cards are mainly used as a form of borrowing, the Reserve Bank acknowledges, however, credit cards can be in credit balance for various reasons, including topping up before international travel, getting a refund from a merchant, or receiving payments from others.

"Reserve Bank credit card survey data as at 30 November 2023 showed $153 million of credit balances on credit cards."

"Only credit balances on these specific borrowing products are proposed to be included in the protected deposit regulations. We do not recommend covering all borrowing products, where a credit balance may occasionally arise due to an error or an inadvertent extra payment (such as on a personal loan), as these products are unlikely to be equivalent to deposits and would be more complex to include. Note that the Deposit Takers Act specifies that debit balances (negative balances such as accounts in overdraft) are disregarded when calculating DCS entitlement," says the Reserve Bank.

Will debentures be protected deposits?

Meanwhile, the Reserve Bank says whether debentures are protected deposits is likely to be determined by whether they are readily tradeable.

"A debenture is a type of debt security between a borrower and a lender, that commonly provides the lender security over the borrower’s assets. A small group of deposit takers, primarily finance companies, commonly issue debentures to depositors. In general, depositors may treat these debentures as ordinary deposits (or be otherwise unaware of their different legal status). Whether debentures are protected deposits is therefore important to clarify."

"Whether debentures are protected deposits is likely to be determined by whether they are ‘readily tradeable’. Tradability can create uncertainty about the appropriate protected balances. For example, if half of a $200,000 balance was in the process of being transferred at the point of failure, it may not be clear if it has become a separately eligible $100,000 deposit in the hands of the new owner," the Reserve Bank says.

Section 457 of the Deposit Takers Act has more detail on what "readily tradable" means.

The Reserve Bank's seeking submissions by May 10.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

35 Comments

Let's rather work on a scheme to protect folk who lose their money through being stupid:

It's very important to protect wealthy NACT-voters from scammers (not to mention themselves), you know. /sarcasm

Exactly.

Also: "He said I was the most beautiful woman he'd ever seen (online), and that he'd love me forever and a day. I was devastated when he told me how his 4 kids (from a previous marriage) all died in a freak rickshaw accident in Laos. How could I say no when he asked to borrow money for the funeral.."

Please don't force us all to assist scammers like these by providing insurance for their victims.

$100,000 seems low. Given that deposits will remain the same overall, all it does is to share the deposits more widely around the various banks. Some will lose some deposits others gain some. Which makes no difference to overall stability.

Unless of course a higher sum recieves a higher interest rate to account for it only being covered up to $100,000. Pigs on standby for takeoff.......

Kiwibank used to be explicitly covered by NZ Post. No more.... Now, implicitly covered by the govt. Hence I have favoured it.

I have also favoured Kiwi Bonds which are explicitly covered by the govt. These might come into their own when banks are released from any liability for getting into trouble.

eg Their covered bonds which the general public have no idea about....

Is your statement correct ? It’s not how I read it, in the disclosure statement below.

https://debtmanagement.treasury.govt.nz/sites/default/files/nz-govt-kiw…

"However, section 55 of the Public Finance Act 1989 provides that all money payable in relation to money borrowed by the Crown, including all money payable to Bondholders is secured by a charge upon and payable out of the revenues of the Crown".

Good enough for me.

The government can repay its bonds at any time that it chooses to and just as it did when it undertook QE and it doesn't require any revenues to do so and just as it doesn't need to issue any debt in the first place. https://www.levyinstitute.org/publications/can-taxes-and-bonds-finance-…

Yep, no surprises there... just keep pushing the date back until AFTER crashing the housing market.

Why stop at just wiping out those with hefty mortgages when you can also wipe out those other folks with savings. Then get the taxpayer to make up the rest so those precious banks can keep on scalping us all. Doesn't matter if everybody is left with nothing.

Cruel irony being many of those "folks" with savings probably realized them on the sale of a house or two, where the savings are derived from huge capital gains due to rampant expansion of mortgage lending, well in excess of what they put in + general inflation.

They're the other side of the ledger, i.e. you don't have to follow the money very far from its source. Sadly they'll have to take a share in the pain, but the system could never actually afford to give them what they received in the long run and it eventually catches up on you.

Thank you.

"However, OBR is technical, not well understood by the public generally, and was created specifically to serve a system that did not provide a Government deposit guarantee or insurance scheme to depositors. OBR is also entirely unique to New Zealand. This means there are no examples of OBR and a deposit guarantee or insurance scheme successfully co-existing," says NZBA.

Watch this space.

This is as I understand it. The retail and I emphasise retail will cover Joe Blogs in the street to the tune of $100k/account/bank. If you have 50k with say a unit trust cash fund eg Milfords Cash fund where they have a few million invested with one bank, ANZ I believe, you are not covered. You have the potential to loose some your funds with the institution if OBR is applied to the institution. Hopefully RBNZ cover institutions by OBR otherwise I can see RBNZ ensuring the institutions loose all their deposit that they have with a bank to payback retail investors.

Hopefully the pundits at RBNZ are looking carefully at all of this. My concern they let the public know as little as possible to ensure there is no "bank run" on institutions holding cash for their clients. In any event I think any unit trust fund has to hold a % in cash to re-imburse those who want to redeem their units and these will also be affected in event of a major bank collapse.

Thanks. It partially answers my concerns. With a bank deposit scheme we end up with a mixed setup. Those retail investors covered by the deposit scheme and the financial institutions who have bulk amounts with banks and down the line many retail depositors holding amounts with the institution. As far as I'm aware RBNZ has not indicated the institutions will be subject to OBR in a mixed setup. If that's the case, no OBR for financial institutions then they'll line up in the liquidation queue to get some funds back which is likely to take months if not years.

At my level of understanding OBR, as a stand alone system, gives everyone retail depositors (excluding de minimas) and financial institutions the same haircut to enable the bank to keep running within a week or so (forget the fanciful with 24h?). Liquidation is shut up shop for how ever long it takes liquidators to sort out the various parties.

When federal regulators stepped in to backstop all of Silicon Valley Bank’s deposits, they saved thousands of small tech startups and prevented what could have been a catastrophic blow to a sector that relied heavily on the lender.

But the decision to guarantee all accounts above the $250,000 federal deposit insurance limit also helped bigger companies that were in no real danger. Sequoia Capital, the world’s most prominent venture-capital firm, got covered the $1 billion it had with the lender. Kanzhun Ltd., a Beijing-based tech company that runs mobile recruiting app Boss Zhipin, received a backstop for more than $900 million.

Treasury Secretary Janet Yellen cast the government’s response — including backstopping all depositors — as necessary. “American households depend on banks to finance their homes, invest in an education, and otherwise improve their standards of living. Businesses borrow from these institutions to start new companies and expand existing ones,” she said at an industry conference the following week before discussing the intervention. Link

The debt wheel must keep turning or if everyone tries to pull their money it all goes down the drain. Confidence is now currency and with attention spans and intelligence on the decline, where anyone will believe anything without getting proper evidence, it’s easy to see how fragile the system, a.k.a human confidence is.

We welcome your comments below. If you are not already registered, please register to comment.

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.