Compare today’s personal loan rates for March 25, 2024: Rates trend in different directions

“Verified by an expert” means that this article has been thoroughly reviewed and evaluated for accuracy.

BLUEPRINT

Published 3:01 p.m. UTC March 25, 2024

Editorial Note: Blueprint may earn a commission from affiliate partner links featured here on our site. This commission does not influence our editors' opinions or evaluations. Please view our full advertiser disclosure policy.

Ivan Nadaski, Getty Images

Personal loan interest rates are set by individual lenders based on market conditions. However, the actual rate you’re offered will also depend on a variety of factors, such as your credit score and repayment term.

Here are today’s personal loan rates as well as average rates by credit score.

Today, the average rate for a three-year personal loan is 14.64% while the average rate for a five-year personal loan is 21.26%. This is an increase from last month’s 13.97% and 21.15% for three- and five-year loans, respectively.

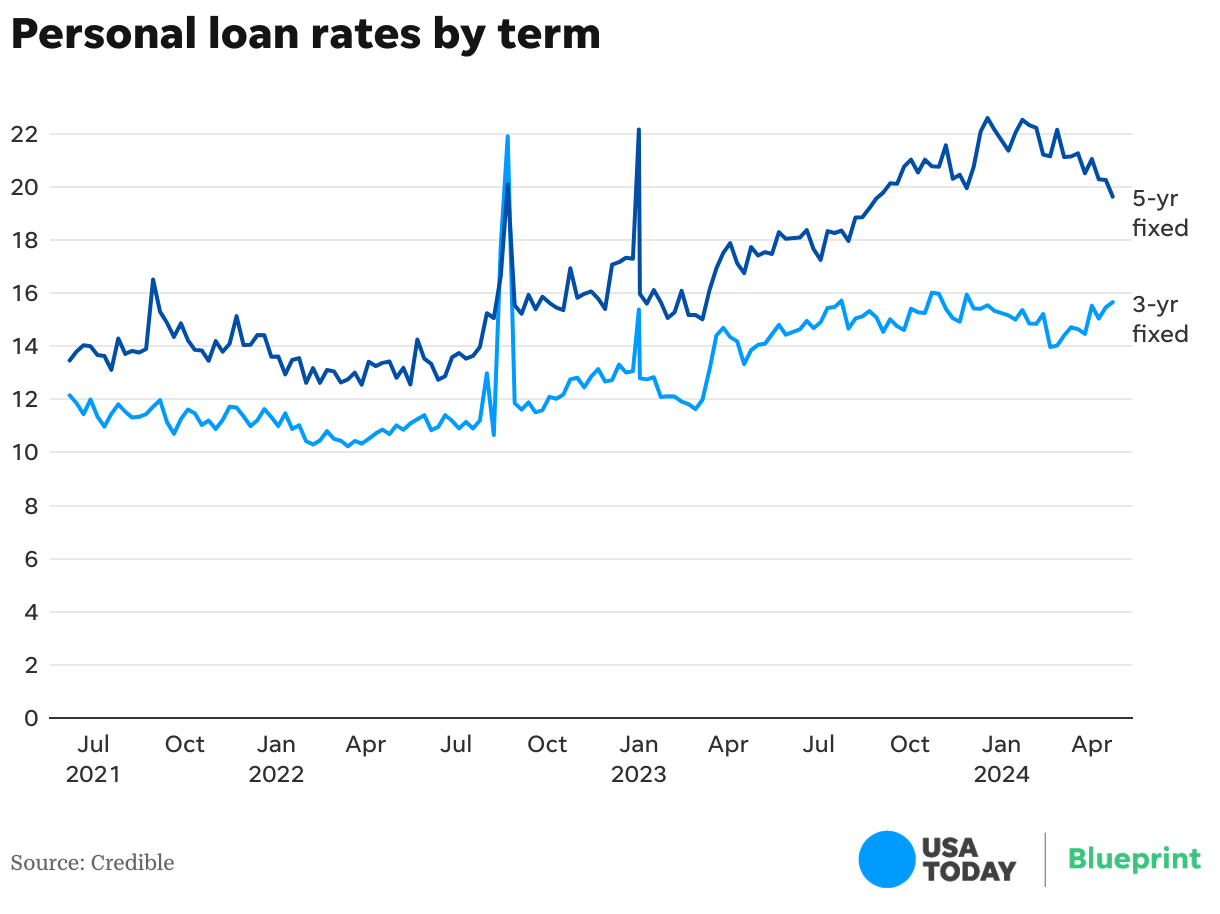

3-year personal loan rates

Today’s rate for a three-year personal loan is 14.64% — lower than last week’s 14.71%, according to data from Credible. This is an increase from last month’s 13.97% and is also higher than last year’s 13.10%.

If you take out a loan at today’s rate, you can expect to pay $344.89 per month for every $10,000 you borrow. This is lower than last week’s $345.23.

5-year personal loan rates

Today, the rate for a five-year personal loan sits at 21.26% — a rise from last week’s 21.14%, according to data from Credible. This is also up from last month’s 21.15% as well as an increase from last year’s 16.10%.

A loan with today’s rate will result in a monthly cost of $272.00 for every $10,000 you borrow. This is an increase from last week’s $271.32.

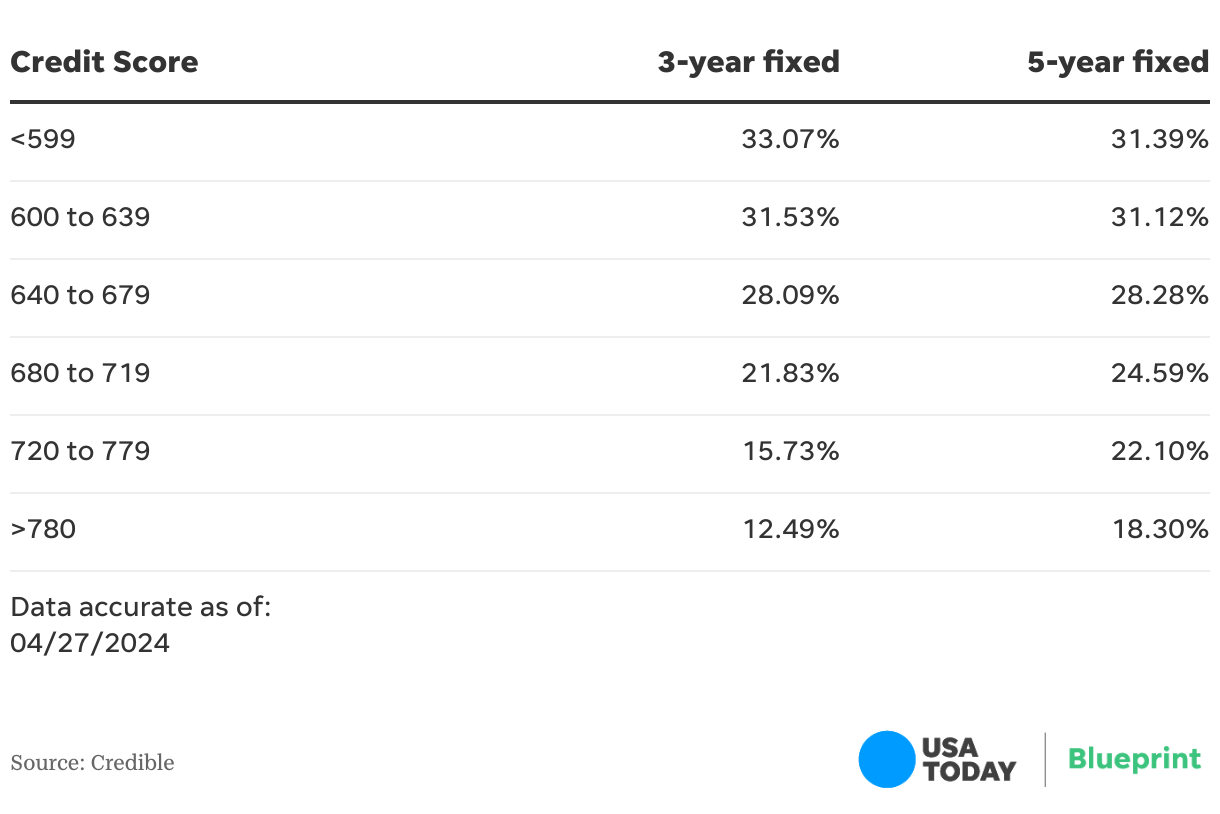

Today’s personal loan rates by credit score

Your credit score is one of the biggest factors that lenders use to determine your interest rate. In general, the higher your credit score, the better your rate will be.

Frequently asked questions (FAQs)

While the exact credit you’ll need for a personal loan will depend on the individual lender, you’ll generally need good to excellent credit to get approved. A good credit score is usually considered to be 670 or higher.

There are also several lenders that accept poor or fair credit scores. Just keep in mind that bad credit loans usually come with higher interest rates compared to good credit loans.

Whether it’ll be better for you to borrow from a bank or credit union will depend on your circumstances. Because credit unions are nonprofit organizations, they tend to offer lower rates on personal loans compared to banks and are also sometimes more lenient with credit score requirements. However, you’ll have to join the credit union to proceed with a loan. Every credit union has its own eligibility requirement for membership.

Banks, on the other hand, are for-profit institutions, and they generally charge higher rates and fees on personal loans compared to credit unions. But if you already have an account with a bank, you might be able to take advantage of loyalty rate discounts that could help you save money on interest charges. Additionally, almost anyone can open a bank account by providing identification and an initial deposit.

When you apply for a personal loan, the lender will perform a hard credit check while determining if you qualify. This can cause a slight drop in your credit score — usually by five points or less. While a hard credit inquiry can remain on your credit report for up to two years, it will only affect your credit score for a year at most.

Additionally, taking out a personal loan could help your credit score in the long run. For example, you could see an improvement in your score if you make on-time payments or are able to diversify your credit mix. Ultimately, a personal loan might have a greater positive impact on your credit compared to any initial negative effects.

Blueprint is an independent publisher and comparison service, not an investment advisor. The information provided is for educational purposes only and we encourage you to seek personalized advice from qualified professionals regarding specific financial decisions. Past performance is not indicative of future results.

Blueprint has an advertiser disclosure policy. The opinions, analyses, reviews or recommendations expressed in this article are those of the Blueprint editorial staff alone. Blueprint adheres to strict editorial integrity standards. The information is accurate as of the publish date, but always check the provider’s website for the most current information.