Various Student Education Loan Options Continue to Expand

Income-based student education loans could be a suitable scheme to be implemented in Indonesia.

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

The atmosphere of learning English in the education program "Kejar Paket C" at the JICT Learning Center in Koja, North Jakarta, on Monday (6/3/2023). Some students drop out of school due to various factors such as costs, being a victim of bullying, and being expelled from school due to a mistake or conflict with the law.

The issue of student loans (student loans) intended for college students continues to arise. At least, there are two main points of discussion surrounding this polemic, namely the loan scheme which includes tenor, interest rate and funding source, as well as the risk of default as experienced by several countries, including when the Indonesian Student Credit (KMI) program was implemented.

Discussions about student loans emerged after the polemic about paying single tuition fees (UKT) at the Bandung Institute of Technology (ITB) through the online loan scheme was widely discussed in cyberspace in early 2024. Students who feel burdened by the payment scheme, suspecting there is a conspiracy between the campus and the lender. On the other hand, the campus and lenders who have signed the cooperation claim that this is in accordance with applicable regulations.

Also read: KMI Education Loan Ended Due to Traffic Jam?

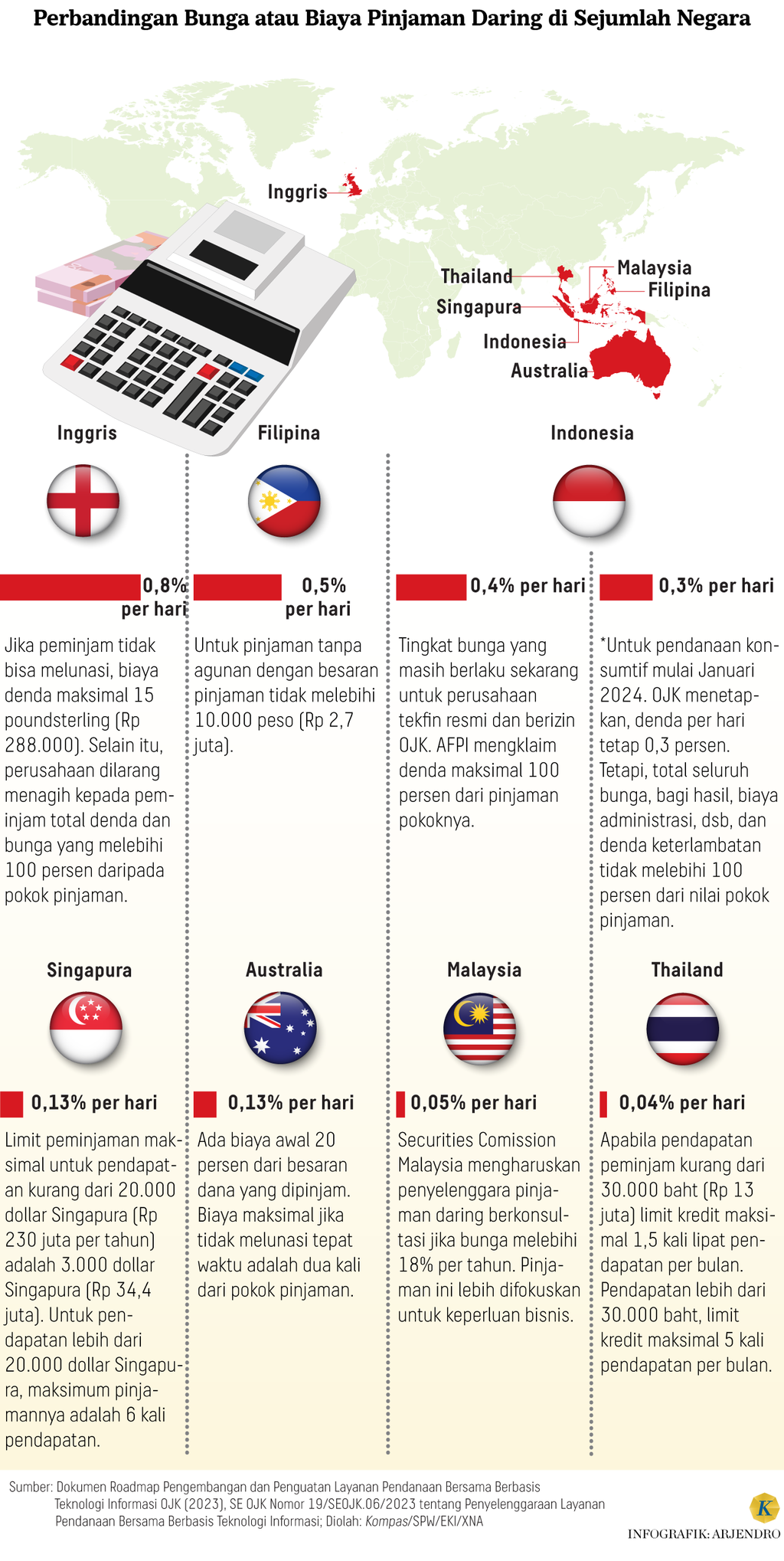

Last week, the Business Competition Supervisory Commission (KPPU) stated that it had discovered alleged violations of Law Number 5 of 1999 concerning Prohibition of Monopoly Practices and Unfair Business Competition in the education loan polemic through loans online. The results of the KPPU's study and in-depth study since February 2024 show that business actors have set interest rates that are too high, both compared to banks and education loans abroad.

"The KPPU suspects that online lending business actors have engaged in monopolistic practices and unhealthy business competition in the market. Therefore, on March 20, 2024, the KPPU decided to continue the study or research by conducting preliminary investigations to find evidence of violations and clarity on allegations of violations of Law No. 5 of 1999," said the Chairman of KPPU, M Fanshurullah Asa, in his official statement on Friday (22/3/2024).

Responding to this, AFPI General Chair Entjik S Djafar said, fintech lending or online loans can play a role in encouraging inclusion in the education sector through financing solutions (eduloan) and a number of AFPI members who licensed by the Financial Services Authority (OJK) to have implemented it. This collaboration is carried out with universities, course institutions and other competency development institutions.

Based on OJK data as of January 2024, funding from online loans to the education sector was recorded at IDR 2.47 trillion or 1.49 percent of the total loan distribution to the productive sector which amounted to IDR 165.82 trillion. Overall, the online lending industry has distributed funding of more than IDR 785 trillion targeting 123.45 million borrowers and originating from 1.4 million lenders. .

"The fintech lending industry has committed to implementing the best services in optimizing access to educational services through collaboration between universities and financial service institutions," he said at the LawTech Mini Roundtable event held online by AFPI, Wednesday (27/3 /2024).

Also read: Soft College Loans Prepared, Students Pay After Getting Work

Soft loans

On the other hand, the government is still discussing funding scenarios for students, including aspects of student protection, through regulations. One of the proposed schemes is soft loans or loans from the state or multilateral institutions.

The soft loan, as planned, will target students from the lower-middle class considering the financial obstacles and tuition fee arrears that they often face, but do not qualify for scholarships. It is possible that the interest rate of the soft loan will be similar to a microcredit of 3 percent per year or even without interest.

From the aspect of funding sources, the government is considering funding from non-governmental institutions such as philanthropy and corporate social responsibility (CSR) to support interest-free soft loans. To avoid default, the government is also considering the integration of identification number data (NIK) of loan recipients for tracking purposes.

"It is being discussed how the loan is a soft loan, repaid when the student graduates and works. "It's possible to return after graduating the second year," said Deputy for Coordination of Education Quality Improvement and Religious Moderation, Coordinating Ministry for Human Development and Culture, Warsito, (Kompas.id, 18/3/2024).

The "fintech lending" industry has committed to implementing the best services in optimizing access to education services through collaboration between higher education institutions and financial institutions.

There are several things that need to be considered by the government when formulating a scheme for educational loans for students. This has been formulated in a study by the Institute for Economic and Social Research of the Faculty of Economics and Business, University of Indonesia (LPEM FEB UI) entitled "Reviewing Student Loans" as an Alternative Financing for Increasing Access to Higher Education.

Firstly, the government cannot enforce the same loan interest rates as conventional norms, or the higher the risk, the higher the interest rates. A scheme that the government could provide is interest rate subsidies, as applied in the people's business credit (KUR) program or even interest-free loans for students experiencing financial difficulties.

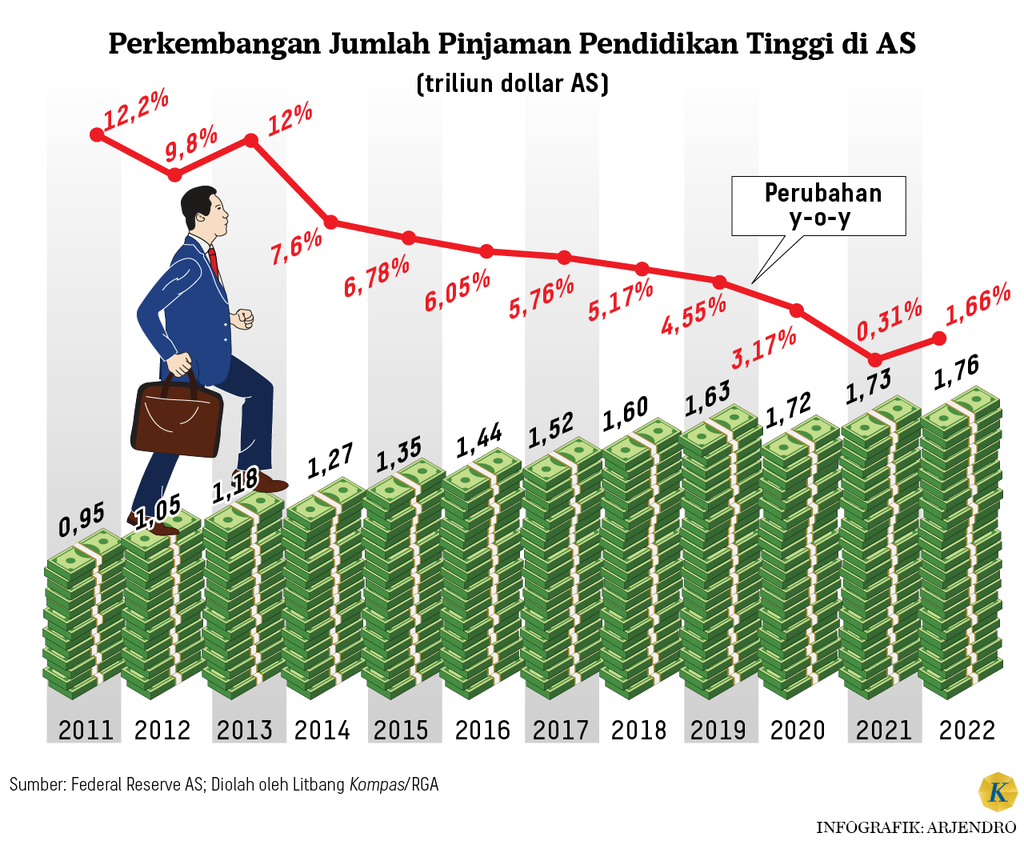

The policy of interest subsidies for student loans has been implemented in the United States (US), Canada, Australia, Germany, the United Kingdom, New Zealand, and India. A study by Dynarski (2021) discussing the concept of student loans in the US found that a lower interest rate can reduce the burden of monthly payments to cover the principal and interest installments, making loan payments easier for marginal borrowers while reducing the risk of default.

University students from Jenderal Soedirman University presented a low-sodium salt that can prevent high blood pressure in Purwokerto, Banyumas, Central Java, on Wednesday (21/2/2024).

Secondly, Indonesia should adopt a income-contingent student loan model as implemented in England, Australia, New Zealand, Chile, Thailand, and the United States. Under this mechanism, the repayment burden of the loan is adjusted based on the borrower's income.

On the other hand, there is a cross-subsidy between the winners or high-income groups who pay part of the tuition fees for the losers or low-income groups. In economic terms and theory, there will be adverse selection or a condition where borrowers who will be subsidized participate, while borrowers who will provide subsidies will not participate over time.

A mechanism like this would be more appropriate to apply in countries that have educational endowments because smart students are naturally less likely to want to take out loans. However, it is believed that this mechanism can work well in Indonesia because there is a special earmarking of 20 percent for education each year so that the education endowment fund in the State Revenue and Expenditure Budget (APBN) is still adequate.

A group of students from Bandung Institute of Technology displayed several writings with the hashtag #Institut Tapi Berpinjol during a protest in front of the institute's rectorate on Sulanjana Street, Bandung City, West Java, on Monday (29/1/2024).

Thirdly, the government can cooperate with public banks or the Association of State-Owned Banks (Himbara) to provide student loan facilities with lower interest rates and relatively long tenors, such as 20-25 years. This policy can also become part of the banks' corporate social responsibility (CSR).

To minimize the risk of default, banks can use diplomas as collateral, and the government must be the one to take responsibility in case of any defaults. For example, in India, the government provides a credit guarantee scheme for banks working together to provide educational loans.

Also read: Middle Class Bears Heavy Burden of Paying for Children's College Education

Income loan

There are two types of student loan models applied in the world, namely time-contingent loans (time-contingent loans) as implemented in the US and income-based loans (< i>income-contingent loan). This time-based loan model is like home ownership credit (KPR) and vehicles where the installment amount will follow a predetermined payment period or tenor.

However, such models tend to be risky in draining the allocation of daily needs for borrowers and have a high risk of delay in payment, as has happened in the US. With a loan of IDR 60 million with a tenure of 10 years and zero interest, for example, the borrower must allocate at least IDR 6 million per year or IDR 500,000 per month for installments. If their income ranges from IDR 2 million to IDR 3 million, their debt burden is around 16-25 percent each month.

Meanwhile, income-based loan models have been implemented in Australia, Sweden, and the UK. With this model, loan repayment burdens will be adjusted according to the borrower's income and will need to be equipped with an income tracking system. In addition, repayment of installments will begin after the borrower's income reaches a certain minimum amount and the payment tenure is not determined, but the debt repayment burden is established.

Based on the data from the 2023 National Labor Survey (Sakernas), the average income for college graduates reaches Rp 57.16 million per year. With an income-based loan scheme, the government can determine the amount of education loan installments, for example around 10 percent or Rp 5.71 million per year. Therefore, the higher one's income, the faster the loan repayment.

On the other hand, for borrowers who have difficulty in paying their installment payments, the government can provide relief in the form of payment deferment. The loan tenure can also be offered between 20 and 25 years, depending on the debt repayment scheme, so the government can calculate the allocation of subsidies to be given.

The findings of The SMERU Research Institute's study entitled "Income-Based Loans to Improve Access to Higher Education" in 2019 showed that the income-based loan model for students is possible to implement in Indonesia. This is because income-based loans will also ensure affordability, equal access, ease of payment, and reduce the risk of default.

In addition, the implicit subsidies that the government must provide in the student loan system only range from 3.1 to 48 percent. This subsidy level is much lower compared to scholarship or full subsidies policies.

However, there are several things that need to be considered in implementing such policies, including income inequality between men and women, job absorption, tracking systems for graduate income, as well as university accreditation to ensure quality. Furthermore, the loan scheme will work well if the country has an effective taxation system, where the majority of workers' income is reported and recorded in government data.

Whatever scheme is ultimately chosen, the government should ensure that the loan distribution is targeted and effective. Those who apply must truly be selected. Additionally, the availability of a database for loan recipients will also determine the success of this program.

Also read: Education Fee Loans, Is It Possible?