Water damage insurance claims statistics

Water damage is among the most common and potentially destructive forces facing homeowners. Just one leak or burst pipe can wreak costly havoc — resulting in thousands of dollars in damages — and even cause larger problems like mold infestations or severe structural issues.

With so much at stake, homeowners would be wise to ensure their insurance covers a wide array of water damage. Not every policy covers each specific type of water damage, however. Read on for a deep dive into water damage insurance claims, including statistics and guidance on protecting your home and possessions.

According to recent data, the average U.S. household claim for water damage and freezing exceeds $12,500.

Jump to insightDespite the risks, fewer than 20% of homeowners say they take precautionary steps to protect their home against water damage.

Jump to insightFor the most recent year full data is available, water damage comprised almost 24% of all U.S. homeowner insurance claims.

Jump to insightThirty-two percent of U.S. homeowners say their home has been affected by a weather event in the past five years.

Jump to insightWater damage claims cost insurers approximately $13 billion per year.

Jump to insightGeneral water damage insurance statistics

While wind, hail, fire, and lightning tend to cause the most severe damage to U.S. homes, water damage is not far behind in terms of frequency and severity.

- Analyzing data from 2017 through 2021, the average household claim stemming from water damage or freezing was approximately $12,514.

- During that time, the Insurance Information Institute (Triple-I) found that water damage claims (including damage incurred from freezing temperatures or burst pipes) were the third-most frequently filed insurance claim for property damage, making up nearly 24% of all homeowners insurance claims in 2021.

- Every year, approximately 1 in 60 insured homes seeks a property damage claim caused by water damage or freezing.

Keep in mind that homeowners insurance typically does not cover damage originating from outside flooding. If you live in an area prone to floods, it may be best to purchase flood insurance separately. Another note: Claims may also be denied if water damage is deemed to be caused by homeowner negligence due to lack of upkeep or reasonable maintenance. For instance, gradual water damage from leaky pipes or a roof leak that gets worse over time may not be covered.

Despite all this, recent findings found that less than 20% of homeowners take precautionary steps to protect their homes against water damage (like checking appliance hoses or performing water heater maintenance).

Types of water damage

According to the Institute of Inspection Cleaning and Restoration Certification, there are three general categories of water damage: clean water, gray water and black water.

While clean water does not pose a substantial risk if exposed, gray water can contain unsafe levels of bacteria, mold and viruses. Black water can contain harmful toxins that cause significant adverse reactions if exposed. It’s also the most expensive to treat and repair.

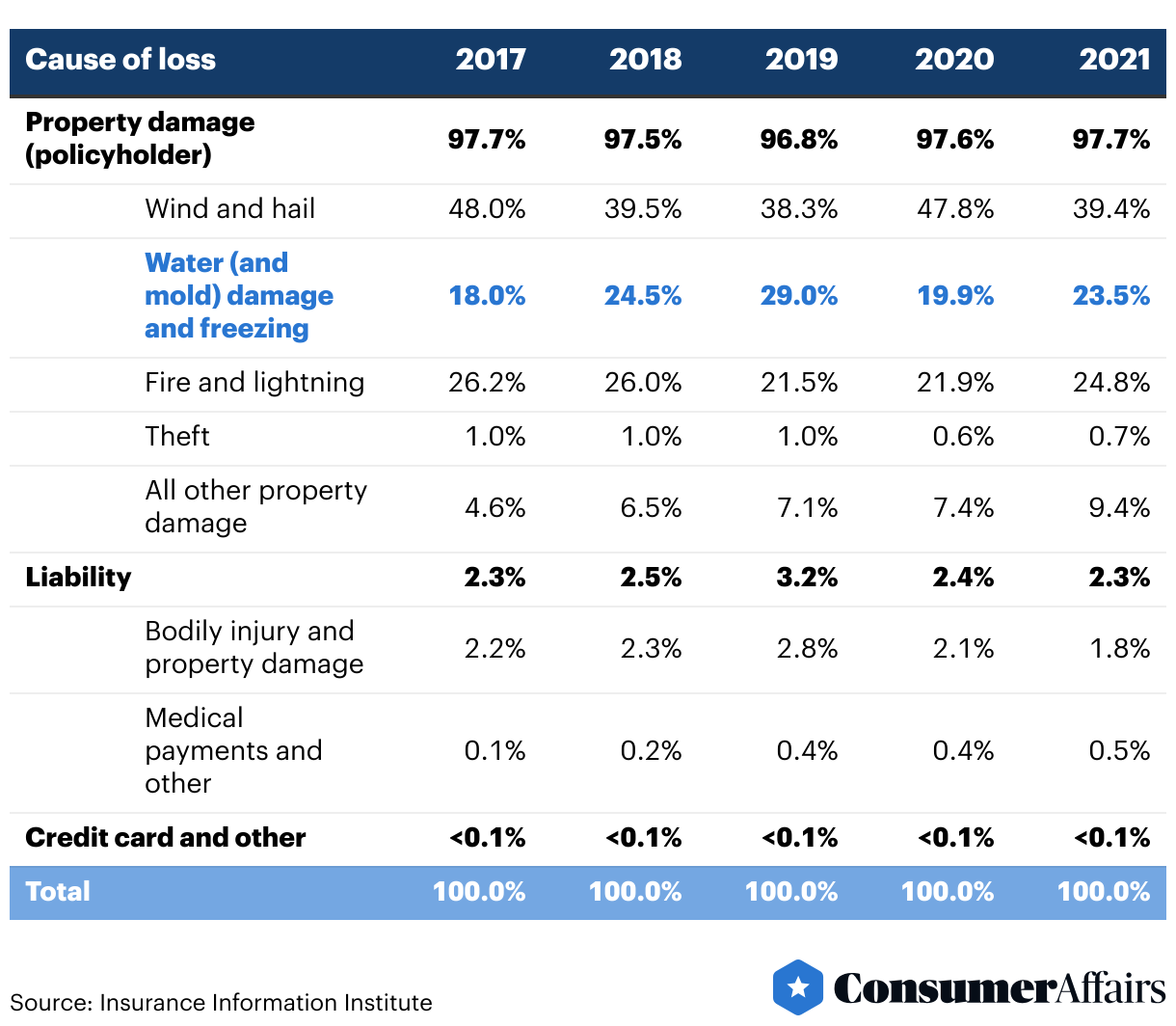

Annual insurance losses for water damage

A 2023 consumer survey by Triple-I/Munich Reinsurance America found that 47% of homeowners have an inventory of their property to provide to insurers in case of losses. Taking stock of belongings may be prudent, as each year, 1 in 20 insured homes ends up having to file a claim. In addition, 32% of homeowners say their home has been affected by a weather event in the past five years.

The percentage for each type of property damage loss varies from year to year, depending largely upon the number and severity of weather-related events. However, water damage is typically near the top of homeowners’ concerns. In fact, the National Association of Insurance Commissioners estimates water damage claims cost insurers approximately $13 billion per year.

Between 2017 and 2021, 5.9% of insured homes submitted a claim. Of those, losses stemmed from the following categories more so than others:

- Wind and hail damage: 2.97%

- Water (and/or freezing) damage: 1.61%

- Other property damage, including vandalism and malicious mischief: 0.83%

Annual homeowner losses from water damage

According to Triple-I, homeowner losses and claims from 2017-2021 break down as follows:

Most common causes of water damage

Water damage can occur multiple ways and by a multitude of means. Household leaks, which can waste nearly 10,000 gallons of water per year, are a common culprit.

Other common causes of water damage include the following:

- Burst pipes caused by pressure changes, sudden temperature drops or wear and tear

- Severe weather and natural disasters

- Damaged appliances, whether due to rusty pipes or worn-out hoses on refrigerators, dishwashers, washing machines or water heaters

- Clogged drains, which can cause overflows that seep into floors, cabinets or walls — all of which can facilitate mold growth (Clogged gutters can also cause significant damage if water is not sufficiently diverted away from the home.)

- HVAC systems that are unable to drain away condensation because of clogged or damaged drain lines and lead to overflow

- Damaged roofs, which can allow moisture to seep in and cause mold growth and significant structural damage

- Sewage backups, which can cause a multitude of costly problems, not to mention health risks

Water damage and weather risks

A 2023 consumer survey conducted by Triple-I/Munich Reinsurance America reveals insight into the weather risks U.S. homeowners face. The survey revealed the following:

- 88% of participants had purchased homeowners insurance.

- While 68% of homeowners reported not being adversely affected by weather in the past five years, 32% indicated impact by a weather event.

- Regarding ongoing weather risks, 54% reported their primary concern to be thunderstorms. When broken down, 11% cited flooding as a top concern, while 22% said lightning with rain and 21% said tornadoes.

The survey also offers insights into the risks and (perceptions of risks) posed by flooding, which is not typically covered by homeowners insurance. The survey revealed the following:

- Sixty-four percent of respondents believed they were not at risk of flooding.

- Fourteen percent were unsure about whether their home was at risk of damages due to flooding.

- Although 22% claimed to be at risk of floods, just 78% of these individuals had purchased flood insurance.

Geography plays a key role in terms of what sorts of water damage homeowners are most wary of. The 2023 report reveals what most concerns homeowners from different regions of the country. Findings include the following:

- Northeast: 17% thunderstorms, 16% flooding, 14% tornadoes

- Midwest: 42% tornadoes, 28% thunderstorms, 5% flooding

- South: 24% thunderstorms, 24% tornadoes, 7% flooding

- West: 16% flooding, 13% thunderstorms, 4% tornadoes

Water damage restoration costs and considerations

Water damage resulting from “sudden” acts of nature may be covered, at least in part, by homeowners insurance. However, cleanup and remediation costs can still be considerable. According to HomeAdvisor, water damage restoration can run anywhere from $1,342 to $6,044 — with significant damage possibly exceeding $15,000.

Average restoration service cost further varied according to the source of water damage (costs do not include related structural repairs or replacements):

- Clean water: $3 to $4 per square foot

- Gray water: $4 to $6.50 per square foot

- Black water: $7 to $7.50 per square foot

Water damage restoration pricing also hinges on how much property was affected. For instance, restoration for one section of a room may be as little as $150, while damage on structural materials throughout the home can run upward of $100,000.

FAQ

What’s the average cost of water damage?

According to data collected from 2017 to 2021, the average U.S. household claim for water damage and freezing was $12,514.

What are the most common types of water damage for homes?

Leaks (whether from toilets, showers, hot water heaters or elsewhere in the home), storms, clogged drains, damaged roofs and faulty appliances are among the leading causes of water damage.

Does homeowners insurance cover flooding damage?

Typically, no. Flood insurance is usually sold separately. Homeowners insurance often only covers water damage that’s “sudden” rather than “gradual,” such as damage resulting from a storm or a burst pipe compared to a slow leak that causes damage over time.

References

- “Facts + Statistics: Homeowners and renters insurance.” Insurance Information Institute. Evaluated March 15, 2024.Link Here

- “Chubb Homeowners’ Risk Survey.” Chubb Insurance. Evaluated March 15, 2024.Link Here

- “Homeowners Perception of Weather Risks.” Insurance Information Institute. Evaluated March 15, 2024.Link Here

- “Water damage is the most common insurance claim in the U.S.” EMC Security. Evaluated March 15, 2024.Link Here

- “Fix a Leak Week.” United States Environmental Protection Agency. Evaluated March 15, 2024.Link Here

- “How much does water damage restoration cost?” HomeAdvisor. Evaluated March 15, 2024.Link Here

Figures