Joe Biden's Top Economic Advisor Has a Harsh but Realistic Solution to Social Security's Growing Cash Shortfall

For most retired Americans, Social Security income is something they couldn't live without. Over two decades of annual surveys from national pollster Gallup have shown that 80% to 90% of then-current retirees rely on their monthly benefit, in some capacity, to cover their expenses. Furthermore, 76% to 88% of non-retirees expect to lean on their payout to offset at least some portion of their retirement costs.

Ensuring the health of America's top retirement program should be at or near the top of the list for lawmakers on Capitol Hill. Yet reports show that Social Security's financial health is worsening.

Current and future retired-worker beneficiaries are looking to elected officials to address Social Security's shortcomings -- and that begins in the White House with President Joe Biden and his top economic advisor, former Federal Reserve Chairperson Janet Yellen.

Social Security's long-term funding shortfall has surpassed $22 trillion

Before digging into the details of Yellen's proposal to strengthen Social Security, let's first address the elephant in the room: Social Security's crumbling financial foundation.

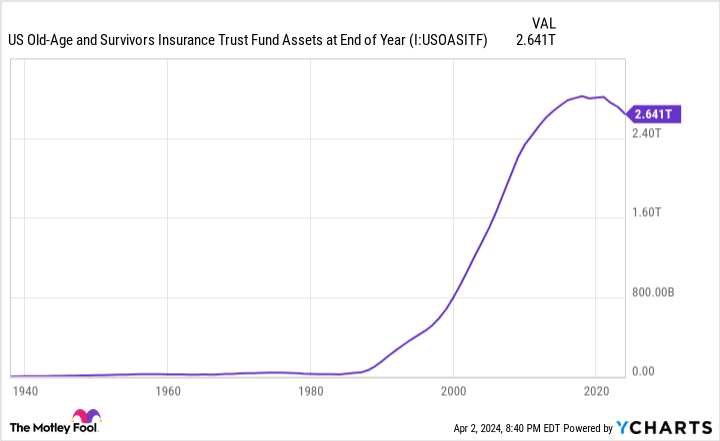

Every year since the first retired-worker benefit was mailed out in 1940, the Social Security Board of Trustees has released a report that examines the financial health of this top retirement program. In addition to detailing how revenue is collected and where each Social Security dollar ends up, this annual report factors in changes to fiscal and monetary policy, along with demographics shifts, to estimate the financial outlook for Social Security 10 years (the short term) and 75 years (the long term) following the release of a report.

Every Trustees Report since 1985 has cautioned that Social Security is facing a long-term funding shortfall. To be clear, this doesn't mean the program is facing bankruptcy or insolvency. Rather, it means the existing payout schedule, including annual cost-of-living adjustments (COLAs), can't be sustained if things continue on their current trajectory.

As of the 2023 Trustees Report, Social Security was facing an estimated $22.4 trillion long-term funding deficiency. Worse yet, the Old-Age and Survivors Insurance Trust Fund (OASI), which is responsible for doling out monthly benefits to over 50 million retired workers and approximately 5.8 million survivor beneficiaries, is on track to exhaust its asset reserves by 2033. If the OASI's asset reserves are depleted, sweeping benefit cuts of up to 23% may be necessary to avoid any further need for reductions through 2097.

What didn't get Social Security into this mess is "Congress stealing funds" or "undocumented workers receiving benefits." These are some of the biggest myths and lies told on social media message boards.

The bulk of Social Security's shortcomings can be traced to sustained demographic shifts. Some of these you know, such as the ongoing retirement of baby boomers and increased longevity since retired-worker payouts began in 1940. However, some of the demographic changes that are adversely impacting Social Security may not be as visible, such as:

A historically low U.S. birth rate.

A more-than-halving in net-legal migration into the U.S. since 1998.

Rising income inequality.

Janet Yellen's Social Security solution offers a harsh reality to future beneficiaries

Lawmakers on Capitol Hill, which include President Biden and his cabinet, aren't oblivious to the fact that Social Security's foundation has weakened. The challenge is deciding how best to "fix" it.

While on the campaign trail in 2020, Joe Biden proposed a four-point plan that primarily relies on taxing the rich to raise additional revenue.

In 2024, all earned income (wages and salary, but not investment income) between $0.01 and $168,600 is subject to Social Security's 12.4% payroll tax. Meanwhile, earned income above this figure is exempt. Biden's plan would reinstate the payroll tax on earned income over $400,000, which would help raise immediate revenue for the program.

During the president's State of the Union address to Congress last month, he had this to say: "Many of my Republican friends want to put Social Security on the chopping block. If anyone here tries to cut Social Security or Medicare, or raise the retirement age, I will stop them!"

But mindful cost-cutting, along with revenue increases, may be exactly what the economist ordered.

In 2018, Janet Yellen and four other authors published an op-ed piece in The Washington Post ("A debt crisis is coming. But don't blame entitlements.") that offered a harsh but realistic way to tackle Social Security's widening cash shortfall. According to the authors:

There is room for additional spending reduction in these [entitlement] programs, but not to an extent large enough to solve the long-run debt problem. The Social Security program needs only modest reforms to restore its 75-year solvency, and these should include adjustments in both spending and revenue.

In contradiction to what President Biden stated during his State of the Union address, former Fed Chair Janet Yellen has gone on record as suggesting that cuts should be part of the solution to strengthen Social Security.

A bipartisan approach to resolve Social Security's cash shortfall makes the most sense

Keep in mind that "cutting Social Security" doesn't mean taking the proverbial scissors to retiree benefits. Reducing outlays would primarily be accomplished by gradually raising the full retirement age to as high as age 70 for future generations of retired workers. The "full retirement age" represents the point where you become eligible to receive 100% of your retirement benefit.

If the full retirement age is gradually increased, future retirees will either have to wait longer to receive 100% of their benefit or accept a steeper reduction for claiming their payout earlier. Either way, the goal would be to reduce the amount of lifetime benefits paid by the program to workers.

The prospect of reducing lifetime benefits is an absolute kick in the pants considering how many people are supported by Social Security each year. But with the full retirement age increasing by two years since the program's inception, compared to an increase in life expectancy of roughly 13 years over the same span, there'd be logic behind the proposal.

Ultimately, Social Security would be its strongest if the approach were bipartisan.

While gradually raising the full retirement age would successfully reduce long-term outlays, it would take decades for the program to realize these cost savings. This means the Republican's approach to lower spending does nothing to address the expected depletion of the OASI's asset reserves by 2033.

On the other hand, President Biden and the Democrat's calls to increase payroll taxation on high earners would immediately lift revenue and push the OASI's asset reserve-exhaustion date further down the road. What taxing the rich doesn't do is come anywhere close to eliminating Social Security's long-term funding shortfall. In fact, Biden's four-point plan reappropriates much of the revenue raised from taxing the rich and pushes the OASI's asset reserve-exhaustion date out by only five years.

The point is that Social Security's best chance of success is if core components from Republicans and Democrats are incorporated into one bill. This is what happened with the Social Security Amendments of 1983, and it's likely what's needed to ensure the financial health of this program for generations to come.

The $22,924 Social Security bonus most retirees completely overlook

If you're like most Americans, you're a few years (or more) behind on your retirement savings. But a handful of little-known "Social Security secrets" could help ensure a boost in your retirement income. For example: one easy trick could pay you as much as $22,924 more... each year! Once you learn how to maximize your Social Security benefits, we think you could retire confidently with the peace of mind we're all after. Simply click here to discover how to learn more about these strategies.

View the "Social Security secrets"

The Motley Fool has a disclosure policy.

Joe Biden's Top Economic Advisor Has a Harsh but Realistic Solution to Social Security's Growing Cash Shortfall was originally published by The Motley Fool