Plenty of people would stop worrying about money if they had a net worth of $2.3 million. That number dwarfs the median household net worth of $166,900, according to Census Bureau data, and it lands the earners comfortably in the 90th percentile of U.S. households.

Nevertheless, a couple of very-well-off 37-year-olds recently wrote to money expert and self-made millionaire, Ramit Sethi, to express their financial angst. Both partners work in tech and together earn about $850,000 a year, Sethi told his readers in a recent newsletter. They have a combined net worth of $2.3 million with over $1.5 million in retirement and regular investment accounts.

They still fear they're not saving enough.

Based on that and other information they provided, Sethi is "a bit troubled" by their situation. Here's why.

Get South Florida local news, weather forecasts and entertainment stories to your inbox. Sign up for NBC South Florida newsletters.

Their money concerns are misplaced

"This couple is going to be extraordinarily wealthy over the course of their life," Sethi said in the newsletter. "If they simply left that money in the market and did nothing else, it would turn into many, many, many millions of dollars at a conservative 7% return rate."

This couple is far from being in a precarious financial situation. So why the fear?

Money Report

Their attitudes about money aren't aligned with the reality of their objectively secure position. Anything can happen, and the couple mentioned fears like artificial intelligence making their jobs obsolete. Still, "they are playing life on defense," Sethi wrote.

"They are so far ahead of almost anyone else and yet they still feel worried."

DON'T MISS: The ultimate guide to earning passive income online

'They have already won the game'

Sethi routinely hosts guests on his "I Will Teach You to be Rich" podcast who need a reality check when it comes to their spending. But it's usually because they're spending more than they can afford, either on fixed costs, such as mortgages and car payments, or on discretionary expenses like dining out and travel.

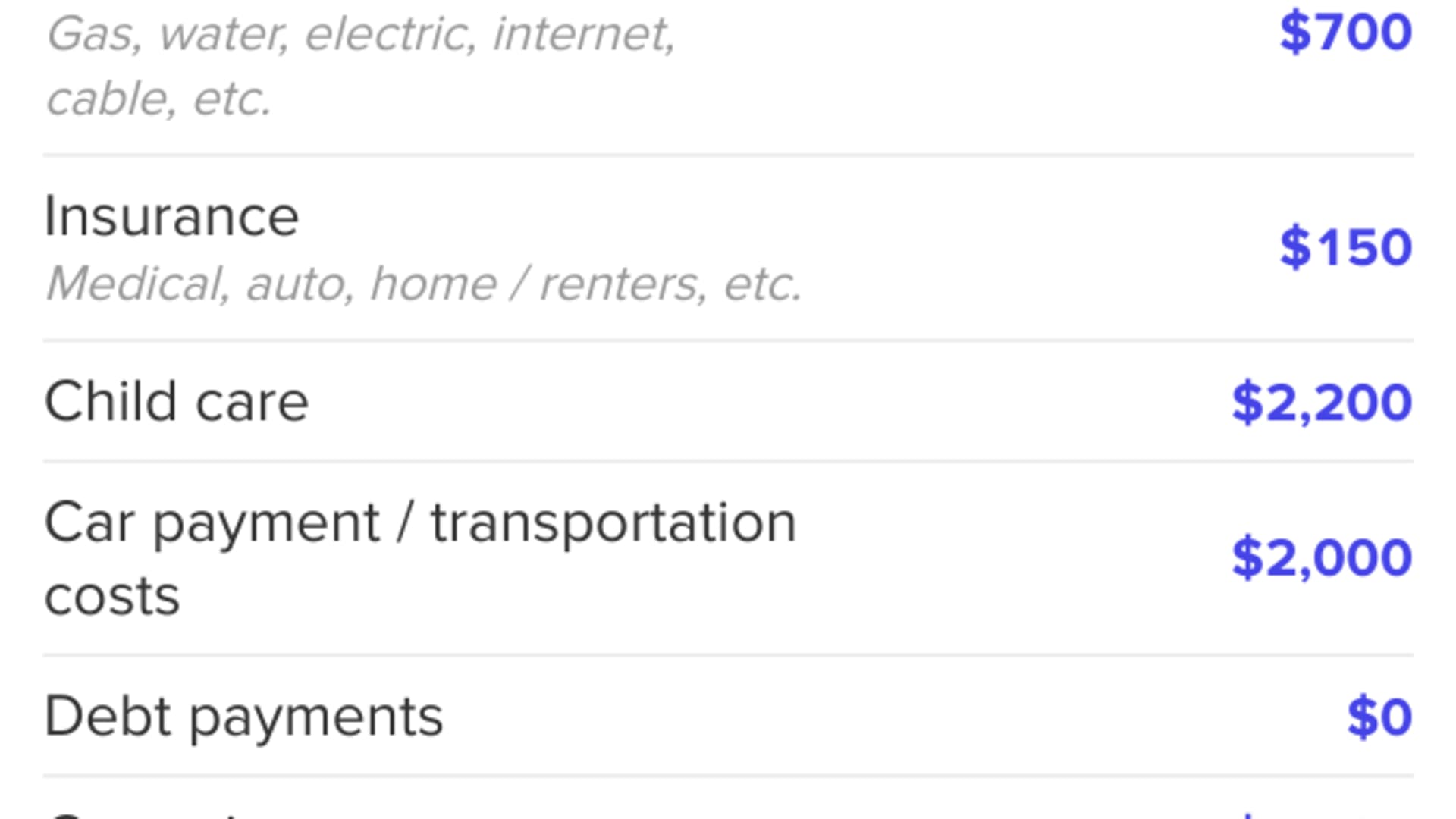

This $2 million couple's fixed costs, however, are well below Sethi's recommended 50% to 60% of income. Here's a glimpse at how they spend their money in a month:

Their living expenses including their mortgage payment, child care, food costs and more, totaling $18,305, come out to about 40% of the couple's net take-home pay. Since they have around $70,000 set aside, they're not regularly contributing more to their emergency savings. That, Sethi says, is fine.

The bulk of their income goes toward their investments — to the tune of about $25,000 a month, between retirement savings, taxable brokerage accounts and a 529 savings plan for their child.

At the time of the newsletter's writing, their investments were worth around $1.5 million. Since they still don't feel financially secure, Sethi believes that's coming from their cultural backgrounds. The partners are both immigrants from India, a culture Sethi says he understands well.

"They're probably going to go the rest of their life worrying about money, thinking they're behind, agonizing over tiny expenses and never actually zooming out and recognizing that they have already won the game," he wrote. "They could get laid off and they would be fine and that in and of itself is unlikely to happen."

They don't yet know 'how to spend money meaningfully'

The couple told Sethi they use about $1,862 a month for guilt-free spending, like going out to dinner or to the movies. That amounts to "an abysmal and pitiful 4%" of their monthly take-home pay, Sethi wrote. Hoarding as much money as possible is not what Sethi wants for his readers.

"This couple lacks the creativity on how to spend money meaningfully," he wrote. "Making $850,000 a year and only spending $1,800 a month or 4% is not something to be applauded. It's actually something that needs a lot of work."

Sethi's whole money philosophy revolves around the idea that money is a tool to provide you with the things you're most passionate and excited about in life. Regardless of your income, if you're not putting enough toward things that bring you joy, you'll probably never feel empowered by money or satisfied with the effort you've put in to build your wealth.

"I'm never going to tell you to stop feeling a certain way, but your feelings can lead you astray. With this couple, it has dramatically led them astray," Sethi wrote. He pointed out the fact that if the couple continues at the rate they're currently investing, they'd have around $35 million by the time they're 65 and wondered what they would possibly do with that money at that age.

"In my opinion, this is a pointless pursuit of wealth without building the skill of spending money meaningfully," he wrote.

'I want to see some improvement'

Sethi's podcast episodes rarely end with him telling a couple to go find ways to spend more money, but with this couple, that's more or less what his advice boiled down to.

"Rather than approaching their money out of fear and playing defense, go on offense," he wrote. He suggested the couple tell themselves, "'We've done great. We've accomplished more than we ever thought we would. We've set ourselves up for financial success for the rest of our life. We can easily take $5,000 a month and spend it on things that are way more meaningful to us.'"

He offered a variety of ways they could use their money to make their lives easier and more "magical." Is there a more convenient childcare option they can afford to splurge on? Perhaps they want to fly business class and bring their families on their next vacation. Maybe they could upgrade their groceries or hire someone else to do the shopping for them.

At their income level, the possibilities are nearly endless.

"By the way, you can afford a lot more than $5,000 a month, but I'm starting you off someplace achievable," Sethi wrote. "Nice job on the financial part of it. I really want to see some improvement on the spending psychology part of it."

Want to make extra money outside of your day job? Sign up for CNBC's new online course How to Earn Passive Income Online to learn about common passive income streams, tips to get started and real-life success stories. Register today and save 50% with discount code EARLYBIRD.

Plus, sign up for CNBC Make It's newsletter to get tips and tricks for success at work, with money and in life.