Michelle is a lead editor at Forbes Advisor. She has been a journalist for over 35 years, writing about insurance for consumers for the last decade. Prior to covering insurance, Michelle was a lifestyle reporter at the New York Daily News, a magazine editor covering consumer technology, a foreign correspondent for Time and various newswires and local newspaper reporter.

Michelle Megna

Michelle is a lead editor at Forbes Advisor. She has been a journalist for over 35 years, writing about insurance for consumers for the last decade. Prior to covering insurance, Michelle was a lifestyle reporter at the New York Daily News, a magazine editor covering consumer technology, a foreign correspondent for Time and various newswires and local newspaper reporter.

As a former claims handler and fraud investigator, Jason Metz has worked on a multitude of complex and multifaceted claims. The insurance industry can be seemingly opaque, and Jason enjoys breaking down confusing terms and products to help others make well-informed decisions.

Fact Checked

Jason Metz

As a former claims handler and fraud investigator, Jason Metz has worked on a multitude of complex and multifaceted claims. The insurance industry can be seemingly opaque, and Jason enjoys breaking down confusing terms and products to help others make well-informed decisions.

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

Finding affordable health insurance on the Affordable Care Act (ACA) marketplace requires comparing the cheapest health insurance plans in your area.

The ACA marketplace at Healthcare.gov lets you weigh health plan options side by side, including information about costs, deductibles and coinsurance. The marketplace is a great way to find health insurance if you can’t get coverage through work.

We compared health plans that offer ACA coverage to find the best and most affordable health insurance plan.

Read more

Show Summary

- Best Affordable Health Insurance Companies

- Summary: The Best Affordable Health Insurance Companies

- How Much Does Health Insurance Cost?

- How Can I Get Affordable Health Insurance?

- What to Consider When Searching for Affordable Health Insurance

- How Do I Choose the Best Affordable Health Insurance Company?

- Need Help Getting Health Insurance?

- Methodology

- Affordable Health Insurance Frequently Asked Questions (FAQs)

Best Affordable Health Insurance Companies

- Kaiser Permanente – Cheapest Health Insurance Company

- Blue Cross Blue Shield – Best Provider Network

- UnitedHealthcare – Best for Customer Satisfaction

Summary: The Best Affordable Health Insurance Companies

Kaiser Permanente and Blue Cross Blue Shield top our list with UnitedHealthcare also receiving high marks.

| Company | Forbes Advisor Rating | Average monthly bronze plan cost for a 40-year-old | Average bronze plan deductible | LEARN MORE | ||||

|---|---|---|---|---|---|---|---|---|

| Kaiser Permanente | 5.0 | $351 | $6,700 | Learn More | On Healthcare Marketplace's Website | |||

| Blue Cross Blue Shield | 5.0 | $458 | $7,173 | Learn More | On Healthcare Marketplace's Website | |||

| UnitedHealthcare | 4.5 | $427 | $8,177 | Learn More | On Healthcare Marketplace's Website |

Source: Healthcare.gov. Based on unsubsidized ACA plans. Average costs can vary significantly depending on your state and age.

How Much Does Health Insurance Cost?

A bronze health insurance plan costs an average of $373 monthly for a 30-year-old. A 40-year-old pays $420 monthly on average for the same coverage, a 50-year-old pays $587 monthly and a 60-year-old pays $890 monthly for bronze coverage.

A bronze plan has the lowest health insurance premiums on the ACA marketplace. Silver plans have the next lowest premiums. A silver health insurance plan costs an average of $488 monthly for a 30-year-old, $549 for a 40-year-old, $767 for a 50-year-old and $1,164 for a 60-year-old.

All of those averages don’t include subsidies or tax credits. ACA plans are the only types that qualify for subsidies based on your household income. People with household incomes below 400% of the federal poverty level qualify for the subsidies that can receive your health insurance costs.

Average Cost of Health Insurance by Age

Age plays an important role in how much you pay for ACA marketplace coverage.

| Age of member | Average monthly overall cost | Blue Cross Blue Shield monthly cost | Kaiser Permanente monthly cost | UnitedHealthcare monthly cost |

|---|---|---|---|---|

|

Age 21

|

$397

|

$444

|

$348

|

$396

|

|

Age 27

|

$419

|

$468

|

$365

|

$415

|

|

Age 30

|

$453

|

$506

|

$396

|

$450

|

|

Age 40

|

$509

|

$569

|

$445

|

$506

|

|

Age 50

|

$712

|

$795

|

$622

|

$708

|

|

Age 60

|

$1,079

|

$1,206

|

$946

|

$1,076

|

Source: Healthcare.gov. Based on unsubsidized ACA plans.

How Can I Get Affordable Health Insurance?

The most affordable health insurance is generally through a plan that you buy at work. Most pre-retirement Americans who have health insurance get group health insurance through an employer.

If a workplace health plan isn’t an option, you may find affordable health insurance costs through the Affordable Care Act (ACA) marketplace, especially if you qualify for subsidies.

Another option for cheaper health insurance is catastrophic health insurance. You can purchase catastrophic coverage through the ACA marketplace, but they’re only available to people under 30 or those going through severe financial hardship, such as homelessness.

Catastrophic health plans offer the same comprehensive coverage found in standard ACA plans. Two major differences between catastrophic plans and standard plans are eligibility and catastrophic health insurance doesn’t have coinsurance. Coinsurance is the percentage you pay for healthcare services after reaching your annual deductible and before meeting your out-of-pocket maximum.

Catastrophic plans only have a deductible and out-of-pocket maximum, which is the same amount. That means you pay up to your deductible and then the health insurance company picks up the rest of the out-of-pocket costs for the year if you have catastrophic health insurance.

Average Monthly Health Insurance Costs by Tier

| Tier | Average monthly cost |

|---|---|

|

Catastrophic

|

$260

|

|

Bronze

|

$345

|

|

Silver

|

$452

|

|

Gold

|

$585

|

Average costs for a 27-year-old. Source: Healthcare.gov. Based on unsubsidized ACA plans.

What to Consider When Searching for Affordable Health Insurance

Consider your family’s current and near future healthcare needs when looking for an affordable health insurance plan. Are you planning to start a new family? Are you on many prescription medications? Do you expect you’ll need to get that trick knee fixed in the coming year?

All of those factors should be taken into account so you can decide whether or not you can choose a plan with a high deductible. A high-deductible health plan (HDHP) typically has lower premiums, but you pay more out-of-pocket when you need healthcare.

Annual Costs, Premiums and Deductibles

The first thing you’ll likely notice when looking for affordable health insurance on the ACA marketplace is the monthly health insurance premium. What you pay varies by the insurance company, deductible, where you live, type of plan, how many people are covered, your age, whether you smoke and your household size and income. Review all costs—premiums, deductibles and coinsurance—of plans you’re considering.

You’ll also want to pay attention to how your health insurance deductible stacks up against your premium. A plan with lower premiums and a high deductible might be a good fit if you don’t expect to need much healthcare. But if you regularly see a doctor, a plan with higher premiums and lower out-of-pocket costs like deductibles may be the most affordable health insurance over the course of the year.

Understand Metal Tiers

In the health insurance marketplace, ACA plans are grouped into four “metal” categories: bronze, silver, gold or platinum health insurance. The metal tiers which indicate how costs are split between you and the health insurance company.

- Bronze plans: You pay the lowest premium every month, but you also have a high deductible, so when you seek care, you have higher costs because it’ll take more to reach your deductible. This metal plan is ideal if you just want coverage for worst-case scenarios. Your health insurance pays 60% of your healthcare costs and you pay the remaining 40%.

- Silver plans: This monthly premium is slightly higher than bronze plans, but your costs are lower when you seek care. Your health insurance pays 70% of your healthcare costs while you contribute 30%.

- Gold plans: If you routinely visit your physician or need care, consider a gold plan, which has a higher monthly premium but lower point-of-care costs. Your health insurance pays 80% and you pay 20%.

- Platinum plans: This plan features the highest monthly premium, so if you’re frequently in need of care, you can rest assured that most of your care will be covered with minimal point-of-care costs when you use any services.

Premium Tax Credits

You’ll want to take advantage of premium tax credits if you’re eligible. Premium tax credits can be used to make health insurance more affordable. The tax credits lower your monthly health insurance payments when you enroll in an ACA plan on the health insurance marketplace.

People with household incomes at 400% of the federal poverty level or below are eligible for premium tax credits. Silver plans may also get cost-sharing subsidies that reduce out-of-pocket costs, depending on household income.

These are two ways to get more affordable health insurance through the ACA marketplace. You’ll find out if you’re eligible after you enter your household information into the marketplace website. The marketplace will tell you whether you’re eligible for those discounts and how much you may save.

HSA vs. FSA

When looking for the most affordable health insurance plan for you, it’s important to know the difference between an FSA and an HSA. Health savings accounts (HSAs) are available only if you have a high-deductible health plan. These are health plans with an annual deductible of at least $1,600 for an individual or $3,200 for family coverage.

An HSA lets you reduce overall healthcare costs by saving pre-tax money in a health-specific savings account. With an accompanying debit card, you can then use these funds to pay for deductibles, copays, coinsurance and qualified medical expenses. An HSA cannot be used to pay monthly premiums associated with your health insurance plan.

You can keep an HSA regardless of your employment status and, after you turn 65, you can treat it like a retirement account for health costs, using the funds however you want without penalty.

Meanwhile, a flexible spending account (FSA) is a similar benefit provided alongside health insurance plans offered through your employer. You fund your FSA with pre-tax dollars from your paycheck and use a paired debit card when you want to use the funds on qualified medical expenses. One drawback to FSAs is the amount you save is unlikely to roll over from one year to the next. In other words, if you don’t use it by a certain date, you lose it.

Out-of-Network Coverage

It’s generally more affordable to see in-network providers than out-of-network providers. If you’re going out of network to see a preferred provider or visit a preferred facility, know that they don’t have a contract with your health insurance plan company and will likely cost more—sometimes even full price.

To keep costs low, either pick a plan that includes your preferred care providers in its network or choose a more forgiving and flexible plan when it comes to out-of-network coverage.

Out-of-Pocket Maximum

This amount is the most you could possibly have to pay for healthcare services in a single year. Your deductible, copays and coinsurance for any in-network services all count toward this maximum. Monthly premiums, payments for services not covered and out-of-network visit costs don’t contribute to your out-of-pocket maximum.

Once you hit your maximum, your health insurance plan kicks in to cover 100% of your costs for the remainder of that year. So if you’re trying to find the most affordable healthcare plan, pay close attention to the out-of-pocket maximum and how much it could possibly support you.

How Do I Choose the Best Affordable Health Insurance Company?

As you prepare to compare health insurance quotes to identify the best, affordable health insurance, keep the following in mind issues beyond costs:

- The type of plan: If you want the most affordable health plan benefit design, you may want to go with a health maintenance organization (HMO) or exclusive provider organization (EPO) plan. Those plans require you to stay in the plan’s provider network, but they have lower premiums than a preferred provider organization (PPO) plan. A PPO gives you more flexibility, but that comes with a higher price tag.

- Your healthcare providers: Make sure that your providers accept a health insurance plan before you buy it. Check with your providers to confirm they take that specific insurance plan and don’t rely on the health insurance company’s online provider directory, which can be incorrect or out of date.

- Your health insurance options: Getting added to another person’s health plan may cost less than buying your own health insurance. Review all of your health insurance options, including a spouse’s or parent’s health plan, before choosing a plan.

Need Help Getting Health Insurance?

Finding an affordable health insurance plan can feel overwhelming, but there are a few ways to get expert help.

- Contact the Marketplace Call Center if you’re choosing your own individual or family plan for questions and assistance with enrollment.

- If you’re selecting a health plan through your employer, ask your human resources department if they can offer assistance.

- If HR can’t provide the help you need, ask them to direct you to an insurance agent or broker who can guide you through the process.

- You can also find a health insurance agent or broker yourself by doing an online search for your ZIP code or state.

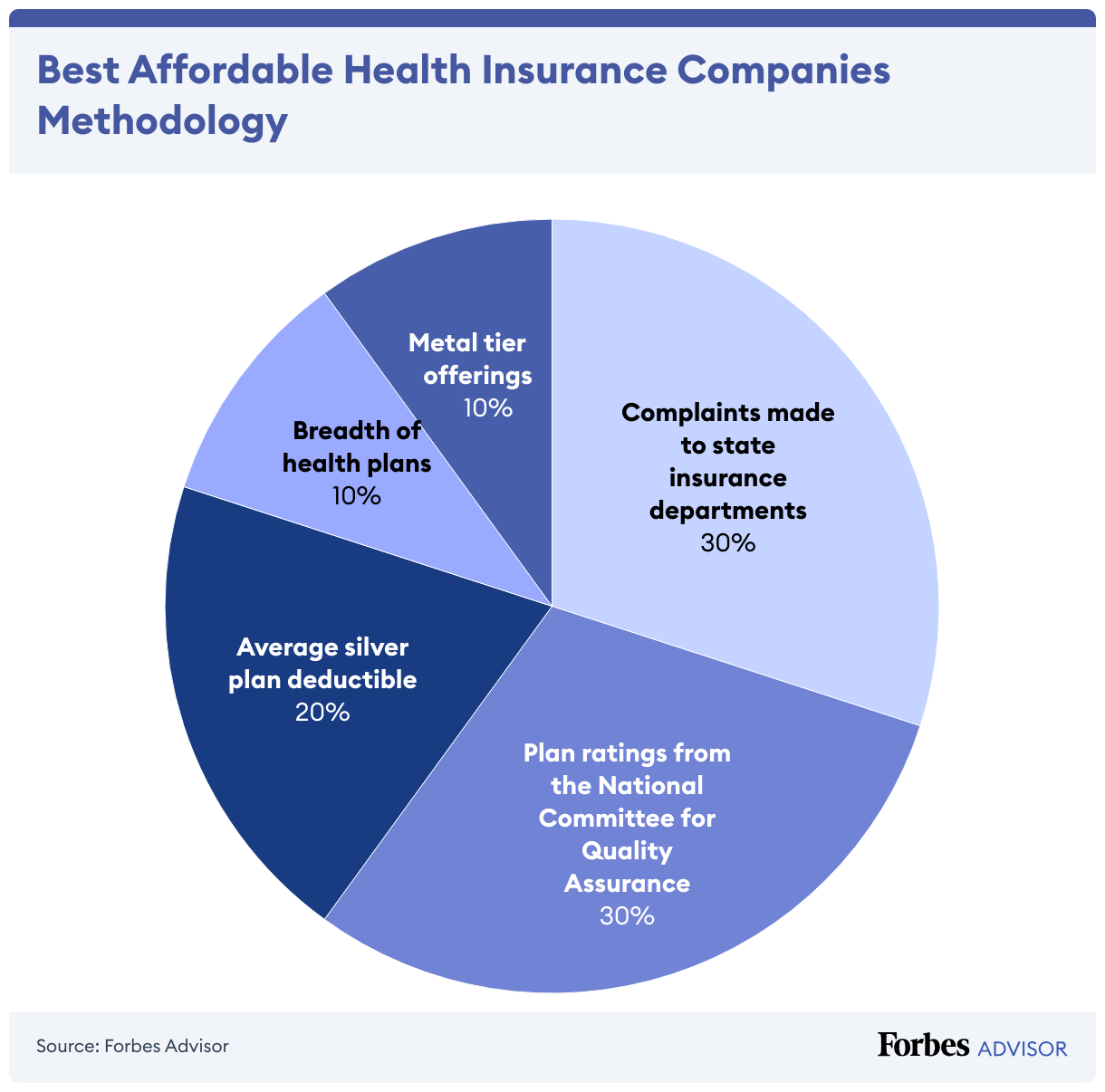

Methodology

We analyzed 84 data points about coverage and quality for seven large health insurance companies to determine the best and most affordable health insurance companies. Our ratings are based on:

- Complaints made to state insurance departments (30% of score): We used complaint data from the National Association of Insurance Commissioners.

- Plan ratings from the National Committee for Quality Assurance (30% of score): The National Committee for Quality Assurance (NCQA) is an independent, nonprofit organization that accredits health plans and produces ratings based on specific metrics, including patient experience, prevention, treatment, overall rating of the health plan and rating of care.

- Average silver plan deductible (20% of score): The deductible is how much you have to pay for healthcare in a year before the health plan begins picking up a portion of the costs. Companies with health plans that had low deductibles got more points.

- Breadth of health plans (10% of score): Health insurance companies may offer up to four types of plan benefit designs (PPO, HMO, EPO and POS). Companies that offered more types of plans got more points.

- Metal tier offerings (10% of score): The ACA marketplace has four metal tier levels. We gave points to companies that offered more tier plan options.

Read more: How Forbes Advisor rates health insurance companies

Affordable Health Insurance Frequently Asked Questions (FAQs)

Can I buy affordable health insurance any time?

You usually can only buy a new health insurance plan or change your coverage during the annual open enrollment period unless you have a qualifying life event. For instance, open enrollment for ACA marketplace plans runs from November 1 to January 15, though some states have longer open enrollment periods.

A qualifying life event, such as losing your health coverage, getting married or having a baby, typically kicks off a special enrollment period. During a special enrollment period, you can sign up for overage or change your existing health coverage.

Can I negotiate the cost of health insurance?

No, you can’t typically negotiate health insurance costs. The health insurance company may offer another plan that would be a better fit for you.

For instance, an insurer may suggest a lower-cost bronze plan, going with a higher deductible or choosing a more restrictive plan like a health maintenance organization (HMO) plan. Those options often have lower premiums than more expensive coverage options.

Should I get a health insurance broker?

A health insurance broker can be helpful if you’re self employed or don’t have health insurance through an employer. A broker can recommend personalized health insurance plans for you to consider.

Health insurance brokers are licensed by the state in which they work and are paid through commissions from health insurance companies, so using one can be a prudent way to find the best affordable health insurance plan.