Is the stock market in a bubble?

This bull market has been a strange one. It's been accompanied by one of the weakest economic recoveries on record. But thanks to the Federal Reserve's cheap-money policies, stock prices have enjoyed a rip-roaring rebound, rising more than 180 percent over the last five years.

But recent volatility in financial markets, along with a nagging sense that investors have grown complacent during the upturn, is now causing many to ask if stocks are in a bubble.

Driving the talk are the dramatic plunges in big technology and biotech stocks since early March. Although such shares have rebounded this month as investors cover their positions, doubts remain about how much farther the bull can run. Could the selloff that hit stocks like Twitter (TWTR) and Google (GOOG) spread to the rest of the market?

Investors were certainly feeling confident heading into the recent decline. In late February, bearishness from newsletter writers and individual investors had fallen to among the lowest levels in 25 years. Moreover, the bullishness of money managers as measured by the National Association of Active Investment Managers had reached its second-highest level ever.

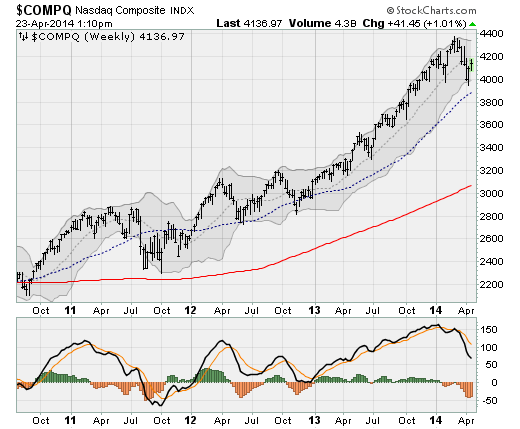

Much of that optimism owes to the consistency we've seen in stocks since the fiscal cliff selloff in late 2012, which was the last time the market suffered any really significant bout of panic selling. That was the last time the Dow Jones industrial average closed below its 20-week moving average.

As a result of the tech and biotech selloff, the tech-heavy Nasdaq composite wasn't so lucky. It suffered the indignity of closing below its 20-week moving average for the first time since late 2012. The Nasdaq remains below this level even as large-cap indices like the Dow and the S&P 500 flirt with new record highs.

Part of the problem has been that investors, jolted from their stupor, are starting to realize that perhaps some of the economic fundamentals didn't justify the excitement. Consider that when it peaked back in January, Amazon (AMZN) was trading at a trailing 12 month price-to-earnings ratio of 691. Now, it's fallen to 551. The same valuation metric on Facebook (FB) has fallen from 88 to 70.

Or consider that the percentage of money-losing IPOs brought to market, nearly 75 percent, has only been eclipsed by the very peak of dot-com fever in early 2000.

Moreover, the overall market's forward price-to-earnings multiple, as measured on the S&P 500, has now exceeded the peak reached at the 2007 market peak. At just over 16, that multiple also exceeds the 35-year average of 12.9. Although valuations reached nearly 25 during the dot-com peak, stocks are fully valued.

In order to justify higher stock prices from here, we'd need to see either acceleration in corporate profits and/or an expansion in the earnings multiples investors are willing to pay for. And so far, first-quarter corporate earnings aren't providing much hope. The blended S&P 500 earnings growth rate stands at around -1.1 percent. While that's up slightly from last week, it's a far cry from the 4 percent plus growth rate expected at the beginning of the year.

The problem is that bank stocks, a huge contributor to S&P 500 earnings, are suffering a dramatic drop in earnings from a decline in mortgage activity, a drop in bond trading profits and an inability to pad results with releases of loan-loss reserves. Moreover, companies in every sector are now dealing with higher input prices and higher labor costs as the job market tightens. By all indications, profits will remain under pressure.

If the market's upside progress is likely to be limited throughout the rest of 2014, what are the chances of a dramatic, bubble-popping selloff? While the fundamentals don't justify another 2013-style melt-up, they similarly don't yet support at 2008-style meltdown either.

The recovery, while no barnburner by any means, is one of the most consistent on record. After a harsh winter constrained economic growth, analysts are looking for a rebound. Research firm Macroeconomic Advisors forecasts GDP growth of just 0.9 percent for the first three months of the year, but expects it to jump to 3.6 percent in the second quarter.

The Fed also remains in full-tilt stimulus mode and is unlikely to raise short-term interest rates until the middle of 2015.

The takeaway is that while areas of the market have certainly become overheated and gains going forward are likely to be much less impressive, a catastrophic wipeout seems unlikely. The best advice is to trim high-risk positions, dial down your overall exposure to equities, and recalibrate your expectations after 2013's smooth and powerful rise.

That isn't to say there aren't opportunities for skeptics out there. Money is flowing into safe havens such as U.S. Treasury bonds, lifting the leveraged Direxion 3x Treasury Bond Bull (TMF) 8.1 percent since I added it to my Edge Letter Sample Portfolio in late February. Or consider short-side plays in stocks like Microsoft (MSFT), due to report earnings this week, that appear vulnerable to a breakdown as lofty expectations are disappointed. I've recommended the May $41 MSFT puts to clients, which are already up 20% so far.

Disclosure: Anthony has recommended TMF and MSFT Puts to his clients.

Anthony Mirhaydari is founder of the Edge and Edge Pro investment advisory newsletters, as well as Mirhaydari Capital Management, a registered investment advisory firm.