Another dramatic day must end. Keep an eye on the website, Twitter, or your nearest Reuters/Bloomberg terminal in case Moody's does downgrade some Spanish banks, as we had expected. In the meantime, here's a closing summary:

Fears that Greece might leave the eurozone, sparking global turmoil, intensified tonight as Fitch downgraded its credit rating. The ratings agency said that there was a heightened risk that next month's election will lead to a government that does not support the current austerity plan, leading to a break-up of the single currency and a Greek default. Fitch would also put all eurozone countries on negative watch, which could lead to further downgrades.

Rumours of a bank run at Spain's fourth-largest bank rocked the markets. Spanish media reported that over €1bn had been withdrawn from Bankia since it was nationalised. The report was denied, after shares in the bank fell by almost 30%.

It was another day of losses on many world stock markets.

The FTSE 100 closed 66 points lower at 5338, meaning it is now officially in correction territory. On Wall Street, the Dow closed 156 points lower.

In Greece, the temporary government was swown in as the election campaign got underway. Polling data painted a mixed picture, with one showing New Democracy in the lead, and another placing Syriza in front. The party's two leaders both hit the headlines, with ND's Antonis Samaras warning that Greece faced a 'nightmare' if it left the euro, and Syriza's Alexis Tsipras predicting 'hell' if it didn't renegotiate its financial programme.

UK politicians weighed in on the crisis again. David Cameron urged other leaders on a conference call to take decisive steps to save the eurozone, Alistair Darling warned that the crisis could blow up in a few hours, and Vince Cable argued that Germany would act to protect the euro.

Thanks, and goodnight! We'll be back in the morning. Hope you can be too.

Wall Street just closed after another day of losses, with the Dow Jones unofficially finishing 157 points lower at 12,441, a drop of 1.25%. That's its 11th fall out of the last 12 day's trading.

The S&P 500 ended almost 1.5% lower, while the Nasdaq lost over 2%.Europe got a lot of the blame.

Downing Street officials have been telling journalists tonight that David Cameron warned fellow European leaders that they need to take "decisive action" to ensure eurozone stability.

This afternoon's high-level conference call involving Cameron, German chancellor Angela Merkel, French president François Hollande and Italian prime minister Mario Monti lasted for 45 minutes.

'This is a debt crisis. And the deficits that caused those debts have to be dealt with.' David Cameron delivers his speech on the eurozone crisis at the Institute of Directors in Manchester today. Photograph: Nigel Roddis/REUTERS

'This is a debt crisis. And the deficits that caused those debts have to be dealt with.' David Cameron delivers his speech on the eurozone crisis at the Institute of Directors in Manchester today. Photograph: Nigel Roddis/REUTERS

A Downing Street spokeswoman said it was a "constructive discussion", ahead of this weekend's G8 meeting at Camp David.

He discussed with the others their priorities for G8: the eurozone - including Greece, growth and the importance of expanding trade relations between the US and the EU.

It's been a tough day for Spain* -- with those rumours (officially denied) of a run at Bankia, the higher borrowing costs seen at this morning's auction of sovereign debt, the IBEX closing at a new nine-year low, the regional downgrades from Moody's, and confirmation that it's in recession.

And in a few minutes, we fear Moody's will also announce that it has downgraded some Spanish banks.....

* - not Greece as briefly mistyped. Perhaps a sign to close things up

Fitch's downgrade of Greece came as I was digesting two opinion polls from Athens.

The latest MARC/Alpha survey, which was conducted between Tuesday and today, put New Democracy (which broadly supports the terms of Greece's financial programme) back in the lead, closely followed by Syriza (which has vowed to reshape it).

New Democracy: 26.1% of the vote

Syriza: 23.7%

Pasok: 13.2%

That, according to Bloomberg, would give New Democracy 123 seats (including the 50-seat bonus for coming first), followed by 66 for Syriza and 41 for Pasok. So the two "mainstream" parties could then form a majority in the 300-seat parliament.

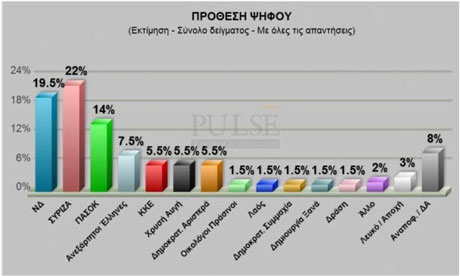

However, a different poll carried out by the Pulse polling group (see bar chart) found that Syriza was the most popular:

Photograph: Pulse

Photograph: Pulse

Syriza: 22%

New Democracy: 19.5%,

PASOK: 14%,

KKE Communist Party: 5.5%

Democratic Left: 5.5%

Golden Dawn: 5.5%

Fitch has also warned that it would put all eurozone sovereign ratings on rating watch negative following the Greek elections if it believes a Greek exit from the eurozone has become "probable".

That would be the first step towards credit rating downgrades. As things stand, only four eurozone countries still hold AAA ratings with all three major rating agencies, while others have already suffered several rating cuts since the crisis began.

Tonight's statement also shows that Fitch have cut Greece's "country ceiling to just B-" That, I think, means that no bond issuer based in Greece can have a higher rating....

Business Insider have now helpfully uploaded the whole statement.

Big breaking news tonight -- Fitch has just downgraded Greece, warning that it could soon crash out of the single currency.

The rating agency cut Greece's long-term rating to CCC, from B-, just two months after upgrading its rating following its debt swap deal.

Fitch said it had taken the move because of the chance that the next Greek government will be led by parties who oppose the current austerity plan.

In a statement, Fitch said

The downgrade of Greece's sovereign ratings reflects the heightened risk that Greece may not be able to sustain its membership of Economic and Monetary Union (EMU).The strong showing of 'anti-austerity' parties in the 6 May parliamentary elections and subsequent failure to form a government underscores the lack of public and political support for the EU-IMF EUR €173bn programme.

In the event that the new general elections scheduled for 17 June fail to produce a government with a mandate to continue with the EU-IMF programme of fiscal austerity and structural reform, an exit of Greece from EMU would be probable.

Fitch went on to warn that a Greek exit would likely result in widespread default on bonds issued by Greek companies, as well as its own sovereigh debt.

Not too bullish today. Photograph: Charles Rex Arbogast/AP

Not too bullish today. Photograph: Charles Rex Arbogast/AP

On Wall Street, the main stock indices have fallen again today. That's partly due to fears over the eurocrisis, and partly the weak economic data released today (see 3.06pm). The Dow Jones is currently down 46 points at 12551, a fall of 0.4%, with the S&P 500 down 0.6%.

That puts the S&P on track for its fifth daily loss in a row.

Brad Sorensen, director of market and sector analysis at Charles Schwab in Denver, told Reuters tonight:

Europe continues to drive sentiment, and it continues to be negative, while in addition today's data was mediocre overall. That's causing people to take risk off the table.

Some breaking news on Spain -- Moody's has just announced that it has downgraded four Spanish regions: Catalunya, Murcia, Andaluca, and Extremadura.

It confirmed its ratings on two other regions - Valencia, and Castilla-la Mancha.

Moody's said it had taken the decision because it believes there is little chance that authorities in these areas will hit their deficit goals. That's worrying – Spain missed its overall deficit target in 2011 because its regions borrowed too much.

The move comes as speculation grows that Moody's will downgrade as many as 21 Spanish banks tonight. According to the FT's fine Alphaville blog, the downgrade is definitely coming, and it's going to be big....

Nearly £190bn has been wiped off the value of shares on the London Stock Exchange since markets began to take fright over a potential Greek exit from the euro, two months ago.

My colleague Patrick Collinson has crunched the numbers, and reports:

In the eight weeks since the FTSE peaked on March 16, the market has fallen by 10.4%, including today's 1.24% drop. The FTSE100 has plummeted from 5965 to 5338, while the All Share index has slumped from 3098 to 2776, according to FTSE Group.

The scale of the fall means it is now an official 'market correction', which is defined as a fall of 10% or more in a relatively short space of time.

Alistair Darling, the former UK chancellor of the exchequer, has blasted Europe's leaders for wasting the last two years, and warned that the crisis could blow up in just a few hours.

Speaking on Sky News, Darling said EU politicians must realise that:

If you don't get growth, you don't get deficits down. It's common sense. We had this debate seventy five years ago.

Darling, who was UK finance minister between June 2007 and May 2010, warned that the world economy simply couldn't cope with another banking crisis, saying that confidence was "desperately needed"

From my own experience these things can blow up in a matter of hours. The slow bleeding of Greek banks should worry everyone.Europe for the last two years has been running round like headless chickens. It's no wonder people now think things will go wrong.

European stock markets have closed in the red again, after another day dominated by fears over the eurozone.

FTSE 100: down 66 points at 5338, - 1.24%

DAX: down 67 points at 6316, -1.06%

CAC: down 32 points at 3016, -1.07%

IBEX: down 73 points at 6537, -1.11%

FTSE MIB: down 194 points at 12089, -1.46%

Fears over Bankia's future saw its shares close 13% lower, despite the official denials that it was suffering a bank run.

The Stoxx 600 Euro Zone banking index, which includes financial stocks from across the single currency, fell by 2.6% to its lowest ever closing level. That reflects speculation that Moody's will downgrade a swathe of Spanish banks at 8pm BST tonight...

With stock markets heading into the close after another day of losses, it has been calculated that the collective pension deficits of Britain's biggest listed companies has swelled by £30bn in the past fortnight.

Actuaries at Towers Watson have, according to the Daily Telegraph, worked out that total deficits in FTSE350 companies' pension funds have increased from £62bn at the end of April to £92bn yesterday.

Most of the damage was caused by falling yields on government bonds such as UK gilts and German bunds, rather than the drop in share prices. Lower bond yields mean that pension funds must calculate that they will earn less from holding sovereign debt, which is why pensions groups really dislike quantitative easing.

Following today's denials from Bankia, City analysts are warning this afternoon that Europe could see bank runs in earnest unless progress is made to resolve the crisis.

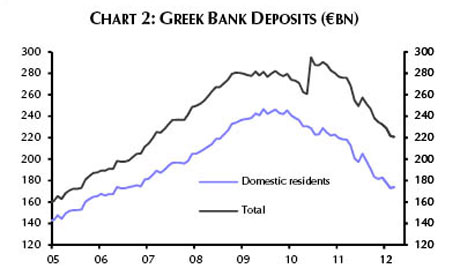

Capital Economics pointed to reports of deposit outflows in Greece, saying:

Concerns are growing that bank runs could soon become a regular feature in other troubled countries in the region deemed at risk of following Greece's lead.

The recent rapid decline in Greek bank deposits underlines our warnings that it could be market pressures exerted through the banking system which prompt some form of euro-zone break-up.

This graph shows how Greek bank deposits have been falling for months.

With the euro bobbing around the $1.27 mark, and shares down in Europe, CMC Markets' Michael Hewson compared the markets to the Vortex rollercoaster at the Thorpe Park theme park:

Talk of bank runs in Europe clobbered banking shares across Europe with Bankia in Spain gyrating wildly lower. Reports that ratings agency Moody's is considering downgrading 21 Spanish banks has also weighed on sentiment as the Spanish IBEX hit fresh nine year lows, as economic data confirmed that the country was back in recession.UK banks also got caught up in the backdraft with Royal Bank of Scotland and Barclays the biggest losers in UK markets.

Greece can look forward to a visit from the International Monetary Fund after next month's election.

David Hawley, the IMF's deputy director of external affairs, told reporters in Washington that officials were very keen to meet Greece's next government, and review progress made against the targets set by the Troika as part of its €130bn bailout.

EC president José Manual Barroso has told the United Nations that Europe will do whatever it takes to help keep Greece within the eurozone.

In prepared remarks running on Reuters, Barroso told the UN General Assembly that the EU will meet its obligations, and that Greece must do the same. Here's a flavour:

As far as Greece is concerned, I would like to reaffirm very clearly that we want Greece to stay in the euro area. And the European Union will do all it takes to ensure it.

Barroso also sent a signal to Greece's leaders, as the new general election campaign gets underway.

We will honour our commitments toward Greece and we expect the Greek government - current and future - to fulfill jointly agreed conditions for financial assistance.

Some disappointing data from America has just knocked market confidence, and suggested that the US economic recovery is faltering.

The Philadelphia Fed business conditions survey was weaker than expected, coming in at -5.8 for May. That suggests US business leaders in the Philadelphia region are seeing tougher conditions.

Seperately, the Confidence Board's Leading Economic Index (a measure of future economic activity), fell in April for the first time in seven months.

Stuart Gulliver, chief executive of banking giant HSBC, has told the Guardian that the crisis has intensified over the last week, and that a firewall would need to be put around Spain if Greece leaves the euro.

Jill Treanor, our banking expert, reports:

A week ago, when Stuart Gulliver was asked about whether Greece would stay in the eurozone he said it was "impossible" to tell. Asked again today, he said "We're in a worse place than we were a week ago".

"It remains a very difficult thing to call. I think the second election in June will be be a referendum on whether to stay in the euro. A month is a very long way away," he said.

"We are now seeing price action that is consistent with capitulation," said Gulliver. And if Greece decides to exit the eurozone, he believes an firewall will need to put around Spain. "We need to take Spain out of the market," he said.

HSBC has a bank in Greece with 16 branches and he said there were no particular signs of inflows or outflows. Asked it if was logical for Greeks to keep their money in banks if the county was going to leave the euro, he said it was: "if you believe the polls that show 75% of the electorate want to stay in the eurozone but don't support the austerity".

But, he added, that if there was a run on Greece banks it might not be possible to wait for the elections on June 17.

Our Madrid correspondent Giles Tremlett has full details on Bankia's denial of a bank run:

In the note, published by the Comisión Nacional del Mercado de Valores as "price sensitive information", Bankia said that operations in its branches "have been within the normal parameters", adding:

The evolution of deposits in the first fortnight of May has a highly seasonal nature

However, there is no mention of the €1bn euros that El Mundo newspaper said had been pulled out of the bank over the past week.

Bankia also expected that "the level of deposits will not suffer any major changes over the coming days."

The bank went on to remind clients that the governmnent had said they would not suffer because of the nationalisation and that the Bank of Spain said last week that Bankia was solvent and functioning normally.

Shares are now "only" 11% down on the start of day price.

Look, no queue. A man uses a Bankia ATM machine on May 17, 2012 in Madrid. Photograph: Pedro Armestre/AFP/Getty Images

Look, no queue. A man uses a Bankia ATM machine on May 17, 2012 in Madrid. Photograph: Pedro Armestre/AFP/Getty Images

Breaking news: Spain's Bankia has called on savers to remain calm. The bank has responded to today's reports that more than €1bn of funds had flowed out of the company in recent days.

Bankia issued a statement to the Madrid stock market in the last few minutes. In it, new chairman Jose Ignacio Goirigolzarri said:

Bankia's clients can be absolutely calm about the security of the the savings they have deposited

So, a clear signal that a bank run is not taking place.

It appears that Spain's economy minister Fernando Jimenez Latorre has calmed the worst of the crisis by insisting that Bankia was not suffering from an outflow of deposits (see 12.54pm)

Shares in Bankia have struggled back a bit, now down 13.6% at €1.43. Still a hefty fall.

An information panel displays trading information for Spain's Bankia and Spain's benchmark IBEX 35 at the Madrid stock exchange today. Photograph: Paul Hanna/Reuters

An information panel displays trading information for Spain's Bankia and Spain's benchmark IBEX 35 at the Madrid stock exchange today. Photograph: Paul Hanna/Reuters

Today's plunge in Bankia shares comes just a week after Spain's government stepped in to partially nationalise the bank. Under that deal, €4.5bn of state loans are being converted into shares, giving the Madrid government 45% of the company.

Like the rest of the Spanish banking sector, Bankia has suffered massive losses because of the country's property crash. This has left it sitting on around €30bn worth of bad debts to developers, or losses on land and buildings which have been repossessed.

Spain's economy secretary has just denied that Bankia is suffering a bank run, Reuters reports from Madrid.

Asked about today's reports that Bankia customers had withdrawn more than €1bn since it was nationalised last week, Fernando Jimenez Latorre told a press conference that:

It's not true that there is an exit of deposits at this moment from Bankia.

According to news flashes from Madrid, Jimenez Latorre also said that Bankia has everything it needs for succes, and should be given time....

The euro has just slipped to a new four-month low against the US dollar, as fears over the eurozone crisis swept through the foreign exchange markets again.

The euro hit a low of $1.2668, its lowest level since 17 January this year. The dollar was also rallying against other currencies, hitting a four-month high against the Swiss franc.

As well as the sitation in Bankia, traders were reacting to a report that Moody's would announce updated ratings for 21 Spanish banks tonight. City analysts fear that many of the banks could be downgraded, with the news now expected at 8pm BST.

European stock markets have fallen sharply following the news that Bankia's shares had tumbled.

In London the FTSE 100 is down 57 points, or 1.05%, at 5348, with Barclays shares falling 3.7%, and IAG (British Airway's parent company which also owns Spain's Iberia) down 3.8%.

Spain's IBEX is down 1.5% at 6510, a new low since 2003.

Italy's FTSE MIB has dropped almost 2%, with its own financial stocks falling.

The French CAC is down 0.8%, losing 24 points to 3023, while the German DAX is down 0.6%, or 40 points, at 6343.

Shares in Spain's Bankia have now fallen by as much as 26% on the Madrid stock market, following those reports of customers withdrawing funds (see 11.17am for more).

Bankia was previously classed as 'under auction' (Reuters reports) -- which indicates that a large buy or sell order was passing through the market, or that the Madrid exchange was struggling to match buy and sell orders due to a mismatch.

UPDATE: Looks like I was wrong to state that Bankia shares had actually been officially suspended, as some City traders also thought. It appears that market volatility was causing trading to be interrupted (with thanks to Pablo Rodriguez of El Mundo, which was the first to report that some Bankia customers have been withdrawing funds.

Vince Cable, the business secretary, said this morning that Germany can save the eurozone from disaster, pointing out that Europe's largest economy has done very well out of the single currency.

Cable told my colleague Dan Milmo that he was not "Apocalypse Now" about the crisis. Speaking from Ellesmere Port, where more than 2,000 Vauxhall car manufacturing jobs have been saved this morning, Cable said he confident of a positive outcome to the Greek crisis.

I am not Apocalypse Now about the European Union and the Eurozone. There are risks around Greece but Greece is a very small country. The significance of Greece is if you get contagion but I think that it is possible to be reasonably optimistic that Germany understands those risks and will put mechanisms in place. There are risks and worries and I am not minimising that. But there is every reason to believe that the EU will pull out of this crisis as Britain will.

Asked what 'mechanisms' he was referring to, Cable added:

We are talking about the firewall, the willingness of the European Central Bank to intervene, the understanding of the Italian and Spanish governments that if they play their part they will get back-up from, particularly, Germany. The Eurozone has advanced quite a long way from the peak of the crisis

It ultimately comes back to Germany thinking they have done extremely well out of the Eurozone, the competitive exchange rate. They have everything to gain from making sure this succeeds. And they are not just going to let it go down the pan.

Shares in Bankia, Spain's fourth-largest bank, have tumbled by as much as 26% this morning. This follows a report that worried customers have withdrawn more than €1bn from their accounts since it was partially nationalised last week.

The El Mundo newspaper reported this morning that Jose Ignacio Goirigolzarri, the bank's new chairman, gave Bankia's board the information at a meeting this week.

Bankia, which was created from seven 'cajas' (savings banks) last year, was only floated on the stock market last July.

Photograph: Reuters

Photograph: Reuters

This graph shows how its share price tumbled in recent weeks, and is down 70% since flotation. That means huge losses for the many retail investors who took part.

David Cameron has begun giving his speech in Manchester, warning about the dangers of the eurocrisis. He began by saying:

We are living in perilous economic times. Turn on the TV news and you see the return of a crisis that never really went away. Greece on the brink; the survival of the Euro in question. Faced with this, I have a clear task: to keep Britain safe. Not to take the easy course - but the right course. Not to dodge responsibility for dealing with a debt crisis - but to lead our country through this to better times.

Andrew Sparrow is covering the whole event here, in his Politics Live blog.

A striking poster urging a No vote in Ireland's referendum on the EU fiscal treaty was erected overnight in Central Dublin:

Photograph: Henry McDonald

Photograph: Henry McDonald

It shows a European fist squeezing Ireland until it bleeds, and was put up by the Mandate union over its headquarters in Dublin's Parnell Square.

It appeared as the latest opinion polls send a warning sign to the Republic's governing parties. Just over a third of the Irish electorate remain undecided about what way to vote in a fortnight's time, according to respected polling firm Milward Brown.

From Dublin, Henry McDonald reports:

Around 35% of voters are in the "Don't Know" category with 37% saying they will vote Yes and 24% indicating they will vote No. This latest snapshot of Irish public opinion was taken amongst 1,000 voters on Monday and Tuesday for today's Irish Independent newspaper.

Of the two ruling parties Labour has the toughest task in securing a Yes vote on 31 May with 50% of their supporters saying they oppose the EU fiscal treaty, the poll found.

However a substantial majority of voters want the Republic to remain inside the euro currency zone with three out of every four polled stating they do not want Ireland to exit the euro.

The increase in the "Dont Knows" indicates that the Taoiseach Enda Kenny and his team still have a fight on their hands to persaude the Irish people to ratify a treaty that ties his government and all other states in the EU into tight budgetary controls.

The opposition to the treaty ranges from Sinn Fein and the United Left Alliance over to pro free market multi millionaire businessman Declan Ganley and his Libertas organisation. Even the British eurosceptic UKIP have entered the fray distributing tens of thousands of leaflets across Ireland urging voters to reject the latest EU treaty.

The word from Westminster is that Downing Street officials are confirming that prime minister David Cameron will hold a conference call with François Hollande, Angela Merkel and Mario Monti this afternoon.

This will give the leaders of the UK, France, Germany and Italy a chance to talk ahead of this weekend G8 meeting, where Barack Obama is expected to urge Merkel to back a new eurozone growth package.

Spain has seen its borrowing costs jump sharply at an auction of government bonds. That's worrying, but the good news is that it raised the funding it needed.

The interest rate, or yield, on €1.09bn Spanish bonds maturing in 2016 jumped to 5.106%, compared with 3.374% at a similar auction in March. That underlines the fears swirling through the eurozone.

Spain also sold €1.02bn of 2015 bonds at an average yield of 4.375%, up from 2.89% in April (a much calmer month).

In total, Spain managed to raise €2.5bn, which means it has met 55.8% of its gross funding programme for 2012.

Nicholas Spiro of Spiro Sovereign Strategy said it would be "painful" for the Spanish Treasury to be selling debt at such prices.

Spain is selling its debt at punitive rates against a rapidly deteriorating domestic and external backdrop. Eurozone "break-up contagion" is seeping into Spanish yields.The Greek crisis is placing huge strain on peripheral eurozone bonds and European bank shares. Spain is on the sharp end of these fears. The Spanish government itself can do very little to shore up confidence in the near term.

Unless there is a bold and decisive response on the part of the eurozone, sentiment towards Spain will deteriorate further. This is a very slippery slope right now.

More developments in Greece - Antonis Samaras, the conservative New Democracy party leader, has addressed his parliamentary group this morning saying "we are the front of resistance against catastrophe."

From Helena Smith in Athens:

The unilateral withdrawal from the EU-IMF sponsored loan deal keeping the Greek economy afloat would be tountamount to the destruction of the country, he said, attacking Syriza for its "lack of preparedness and inability" to govern.

Samaras spelt out "the nightmare" that would ensue if Greece gave up the euro.

Reverting to the drachma would mean wages being "cut in half, deposits being cut in half" and property prices being devalued. The price of imports would skyrocket particularly for food and gas.

"This is the nightmare that those who speak of a unilateral condemnation [of the loan accord] will bring us."

Looking visibly shaken, the ashen-faced Samaras who had been a vociferous supporter of Greeks going to the polls "as early as possible" after the emergency interim government of Lucas Papademos took over last November, said Greece's national interests would also be threatened.

"Greece in Europe is protected nationally and geopolitically," he said. "If we become isolated we will find ourselves totally vulnerable with many around us being tempted to exploit our weakness," he said.

With the new caretaker government in power the speech in effect kicked off the electoral campaign. Alexis Tsipras' will also address his parliamentary group at 1:30 PM (11.30am BS) (as I type, his speechwriters are sharpening their pens).

We're hearing that Alexis Tsipras, the head of the Syriza party whose popularity has surged recently, will travel to France and Germany next week to discuss the crisis.

More from Helena.

Senior cadres in Syriza, the radical left group which looks poised to emerged as the biggest party in next month's elections, have just confirmed that Alexis Tsipras, its leader, will be visiting Berlin and Paris for talks next week.

The 38-year-old, who has sent shockwaves through EU capitals saying that Greece can no no longer commit to the onerous terms of €130bn loan agreement it has signed up to with the EU and IMF, will be departing from Athens for Berlin on Monday.

It's not clear yet who Tsipras will be meeting.

News in from Greece, where our correspondent Helena Smith says the country's interim caretaker government has just been sworn in.

Helena writes:

In what will go down in modern Greek history as one of the smallest cabinets ever, it is comprised of 16 ministers, mostly university professors and diplomats.

The swearing in of the new cabinet followed a similar ceremony for new prime minister Panagiotis Pikramenos. In another first the make-up of the new government was announced at dawn. A high court judge, Pikramenos takes over from former vice president of the European Central Bank Lucas Papademos who left the post warning that Greeks hadn't made sacrifices for "an empty shirt" but to put the debt-stricken Greek economy back on track. "There are those who are waiting to benefit from the chaos that will follow the humbling exit of the country from the common currency," he said.

Benedict Brogan of the Daily Telegraph has a good take on David Cameron's upcoming address in Manchester:

'The Prime Minister's speech is the verbal equivalent of grabbing the Germans by the lapels and shouting 'do something'.

Shares have fallen in major European stock markets today, but we're not seeing a repeat of Wednesday's selloff.

FTSE 100: down 19 points at 5384, - 0.36%

CAC: down 10 points at 3038, - 0.34%

DAX: down 3 points at 6380, - 0.06%

Mike McCudden of Interactive Investor said markets remain on a "negative trajectory", despite some traders reckoning that the crisis might prompt yet more quantitative easing from the world's central banks.

Volatility will remain until the markets have some comfort over Greece and the elections on the 17th June are looking more like a vote on whether they stay in the Euro despite local public opinion.

There are reports from Italy this morning that Mario Monti, Francois Hollande, Angela Merkel, David Cameron and Herman Van Rompuy will hold a videoconference this afternoon, ahead of a meeting of G8 leaders this weekend. Nothing official yet...

New economic data from Spain has confirmed that its economy shrank by 0.3% in the first three months of 2012, which put it officially back into recession.

No relief for the Madrid government, as it battles record unemployment and the crisis in its banking sector.

Spain will be in the spotlight this morning, as it holds an auction of government debt.

Today's front page (with a nice picture of the Erechtheum in Athens, not alas the Parthenon)

Today's front page (with a nice picture of the Erechtheum in Athens, not alas the Parthenon)

$1,000,000,000,000. That's the cost of a disorderly, badly managed Greek exit from the eurozone, according to the Centre for Economics and Business Research.

The CEBR warned this morning that the end of the euro in its current form is certain. But while a well-managed Greek exit might only knock 2% off global GDP, the worst-case would see a 5% drop in global output (or $1 trillion).

CEBR's Douglas McWilliams said: "The economic consequences depend on the timing and the way in which the euro splits. There is no doubt that when the euro breaks up it will be costly.

Some countries will lose around 10% of annual GDP. But this will happen anyway – the choice is between a period of austerity followed by the impact of the end of the euro and then some eventual recovery OR facing the trauma of the end of the euro early and then starting to get the recovery underway."

More details in our front-page story here.

The fact that David Cameron will make such a blunt intervention on the eurozone later today underlines the desperately serious nature of the crisis.

The prime minister's message to Europe will be delivered in the city of Manchester. It appears to be partly a message to his European counterparts, and partly a signal to domestic voters that he will do everything possible to keep Britain safe.

Here's what we expect the prime minister to say:

Either Europe has a committed, stable, successful eurozone with an effective firewall, well capitalised and regulated banks, a system of fiscal burden sharing, and supportive monetary policy across the eurozone, or we are in uncharted territory which carries huge risks for everybody.

"But be in no doubt: whichever path is chosen, I am prepared to do whatever is necessary to protect this country and secure our economy and financial system.

Cameron may also repeat his line from Prime Minister's Questions yesterday that the eurozone "either has to make up, or it is looking at a potential break-up".

Our politics editor, Patrick Wintour, also reports this morning that Treasury insiders has been criticising Germany for demanding too much from peripheral countries. UK sources claim the Westminster government has long been pushing for eurobonds (collective borrowing) and a looser monetary policy.

But while Britain is badly exposed to the eurocrisis, Cameron's ability to influence events is limited. As political commentator Gaby Hinsliff points out this morning, it's not ideal for governments to be warning of problems they can't solve.

..& that's a dangerous position for govt to be in. warning of perils ahead, sounding rather powerless to stop it.

— Gaby Hinsliff (@gabyhinsliff) May 17, 2012

Good morning, and welcome to our rolling coverage of the eurozone financial crisis.

Coming up ... David Cameron is due to warn of the desperate consequences of a eurozone break-up. In a sign that the crisis is dominating the political world, the UK prime minister will argue that eurozone leaders must urgently create closer fiscal ties and an effective firewall to prevent their currency union imploding.

More on that shortly.

In Greece, the new caretaker government will be sworn in this morning. Outgoing prime minister Lucas Papademos has warned that the country stands at a "critical crossroads", but insisted that it can return to "stability, sustainable development and social prosperity".

In the financial markets, yesterday morning's mood of panic has been replaced by a sense of weary unease. Asian markets have clawed back some losses overnight, as traders hunker down for weeks of uncertainty until the Greek elections of 17 June.