It has been anything but a cakewalk for the retail industry over the last few years. Heck, make it the last decade. By now, most industries and sectors have recovered from the Great Recession. Homebuilders, heavy equipment companies, the rails, automakers, etc. But many prominent retail stocks haven’t.

The recession destroyed consumer confidence and pinched spending. Retail had a brief rebound, sure. But now the economy is finally gaining some real momentum and confidence is more than week-to-week or month-to-month. Businesses are hiring and paying (at least slightly) more. Consumers are taking risk. They’ll get that extra latte from Starbucks Corporation (NASDAQ:SBUX). Order an extra pizza from Domino’s Pizza, Inc. (NYSE:DPZ) or go out to celebrate at Fogo de Chao Inc (NASDAQ:FOGO).

But the emergence of e-commerce and Amazon.com, Inc. (NASDAQ:AMZN) have been lethal for most. In a time where Macy’s Inc. (NYSE:M), Nordstrom, Inc. (NYSE:JWN) and other mall-based retailers should be crushing it, they are dwindling away, fighting tooth and nail just to stay relevant.

Does anyone see the disconnect with this? The economy is arguably doing the best it has done in a decade. At least on a sustained basis. We’ve almost forgotten what it’s like to have a solid-growing economy for more than one to two quarters. And yet, that’s not enough to help these stocks. Nor is the fact that we’re a week into November, with Black Friday about two weeks away. It used to be that investors could buy retail stocks in the weeks or even months ahead of Black Friday.

The holidays — and fourth quarter in general — is the biggest season for retailers. It makes sense for them to rally into the event. You know, “buy the rumor, sell the news.”

But what happens when investors aren’t buying ahead of the results?

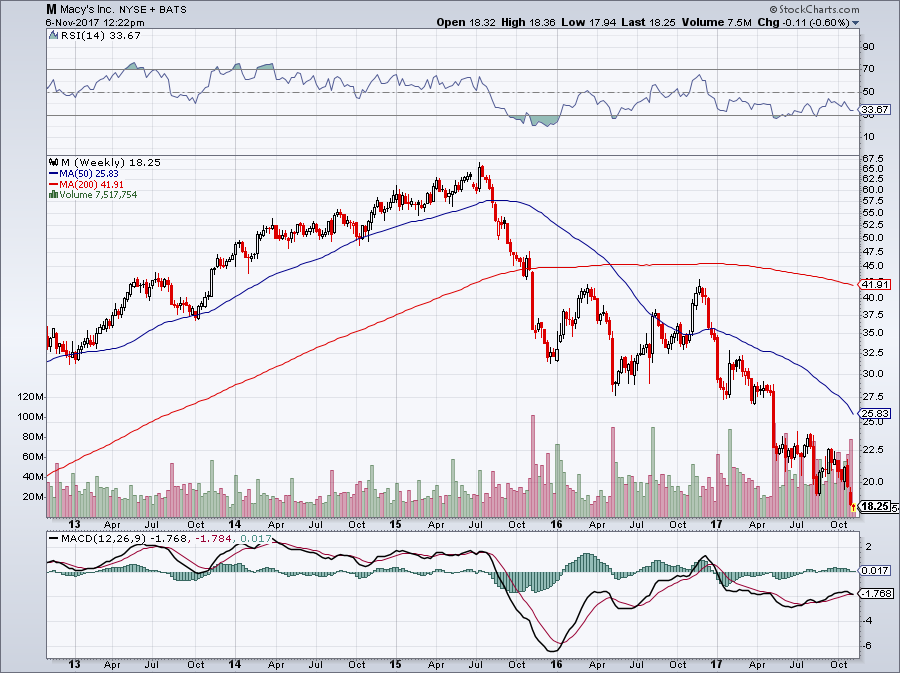

Retail Stocks to Watch: Macy’s (M)

Roulette Spin: Miss … for now.

Roulette Spin: Miss … for now.

Macy’s hit fresh 52-week lows in Monday’s session as the situation seemingly gets uglier by the minute. But does M stock stand a chance? First and foremost, Macy’s still turns a profit. Last year, the company earned $619 million. It also generates about $1 billion in free-cash flow.

On a valuation basis, M stock looks like Ford Motor Company (NYSE:F) and General Motors Company (NYSE:GM) before their 2017 rallies. With high dividend yields and investors calling for peak auto, F and GM stock had single-digit price-to-earnings (P/E) ratios. M stock currently trades with a P/E ratio of 8.3 and a forward P/E ratio of 6.9.

However, with an 8.6% dividend yield and a payout ratio nearing 70%, there’s reason to doubt Macy’s ability to keep up with its quarterly obligation. The truth is, it will likely need to be cut. And remember that $619 million net income in 2016 we mentioned? That’s down more than 40% from 2015.

So while Macy’s is still profitable, is it only a matter of time before it’s operating in the red? Analysts expect earnings to fall about 21% next year to go along with a 3% sales decline.

Macy’s has the free-cash flow — particularly if it cuts its dividend — to stage a comeback. Overhauling its omni-channel operations and closing down underperforming stores will give it a chance. But I can see why no investor is willing to give this stock a premium whatsoever, holidays on tap or not.

The big concern is, what’s left after the holidays? As more shopping shifts to online, what is there to look forward to after December? For Macy’s, nothing. Along with the dividend concern, that’s why investors don’t want Macy’s.

Retail Stocks to Watch: JCPenney (JCP)

Roulette Spin: Chambered

Roulette Spin: Chambered

J C Penney Company Inc (NYSE:JCP) is in deep trouble. It makes Macy’s look like Apple Inc. (NASDAQ:AAPL). Like Macy’s though, the retailer hit new 52-week lows Monday and it’s unlikely to be the last. While Macy’s has a chance to turn the tables, it seems too late for JCPenney.

I remember a good investor friend of mine “pitching” JCP stock to me. He made the argument that it’s a turnaround story. A few improvements here and a few changes there could cause the stock to rally 50% to 75%. I don’t underestimate big moves in deep-value stocks. But even when there is perceived value “locked” in a stock, the problem comes down to trust — you need to trust that management will unlock it.

With the JCPenney team, I simply didn’t believe and I’m glad I didn’t.

The stock is down 71% so far in 2017 and 95% over the last decade. We’re 40 cents away from trading with a $1 handle. Could it rally 25% to $3? Sure. But I don’t want to buy stocks to see if I can capture its “last breath” before dying.

JCP has a market cap of just $736 million now, yet it has $4.3 billion in debt. Cash and short-term investments come in at just $314 million. The company has incurred steep losses over the years too, losing about $2.5 billion over the last four years. Free-cash flow is negative and JCP (rather obviously) pays no dividend.

This company reminds me more of Sears Holdings Corp (NASDAQ:SHLD) than anything else. It’s struggling just to survive. Retail is evolving rapidly and JCPenney is not. When my mother-in-law can coupon her way to paying 50 cents for a quality shirt, I know JCP is in trouble.

Retail Stocks to Watch: Kohl’s (KSS)

Roulette Spin: Miss

Roulette Spin: Miss

Kohl’s Corporation (NYSE:KSS) is an interesting play to me. Not that I’m a buyer in the department store space, but if I were, KSS would be on the radar.

Unlike Macy’s, analysts are forecasting about flat earnings growth for 2017 and 2018. While certainly not worth a premium valuation, that’s better than its average competitor. Throw in the fact that it trades with a forward P/E ratio of just 11 and KSS stock becomes more attractive.

While a dividend yield of 5% is lower than Macy’s 8% payout, it’s more sustainable at this level. It’s payout ratio of 54% also leaves Kohl’s in better shape. Kohl’s has superior operating and profit margins as well.

Finally, over the last 12 months, Kohl’s has generated revenue of “just” $18.7 billion compared to Macy’s $25.8 billion. However, its trailing free-cash flow of $851 million barely lags that of Macy’s $937 million.

Enough of the numbers blitz. In a nutshell, we have a dividend that can be reasonably maintained for the foreseeable future. The stock trades with a low multiple and has flat growth with decent retailing margins. But its business moves are interesting, too.

A lot of people were looking forward to Under Armour Inc (NYSE:UA, NYSE:UAA) getting its products in the store. Given UA stock’s tremendous fall, perhaps that excitement has waned a bit. But its partnership with Amazon is interesting. A number of locations in Chicago and Los Angeles will begin accepting returns for Amazon.

The deal expands Amazon’s physical footprint without opening its own locations. Kohl’s, to some extent, sees increased foot traffic at its locations. In my view, this is just a Band-Aid to the overall, secular issue. But it’s a patch that many retailers might wish they had.

Kohl’s isn’t a screaming buy, but a partial buy near $40 might makes sense. I would certainly consider KSS a buy at $35 for a low-risk entry. At least it’s not printing new low after new low. If retailers start to get any love for the holidays, look for KSS stock to run.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he held a long position in SBUX.