16 Sept 2013 ~ Good Morning Singapore!

Central Execution Team - The Excellence of Execution

This product is made available by your Central Execution Team, for you as TRs of OCBC Securities to help you with your business and therefore it is confidential and only for internal circulation. It is not intended for onward circulation to non-OSPL TRs, clients or any other third party in this or any other version. Neither is this intended to be relied upon as a sole basis for any recommendation. TRs must also consider their clients' investment objectives, financial position and needs when intending to make or making any recommendation. For the front desk, by the front desk. All feedback to make this a better product is welcome.

Global Flash: While You Were Sleeping

Source: Marketwatch

Quote for the day : Women are the largest untapped reservoir of talent in the world.

- HILLARY CLINTON

Singapore: The Day AheadSINGAPORE DAYBOOK :Emerging FX off bottom, but worries still linger. Yuan, Israeli shekel the only emerging market currencies that rose in past 12 months. EVEN though emerging market currencies have rallied from their lows last month, business people and economists continue to fret over the fallout.

Our table shows that even with the recent rally in highly volatile markets in India, Indonesia, Malaysia, Thailand and South Korea, these countries' currencies have weakened significantly against the US dollar. Moreover, since the euro, sterling, Swiss franc and other European currencies have appreciated against the greenback in the past few weeks, emerging market currencies have declined even more sharply against these European currencies.

Brazil, South Africa, Russia, Turkey, Mexico, Poland have also had their currencies hammered. In the Middle East, unsurprisingly, the Syrian and Iranian currencies are basket cases, indicating people of those nations are suffering extreme privations. The only emerging market currencies that have risen in the past 12 months are those of China and, remarkably, Israel.

Currency devaluation will help Asian and other emerging market exporters. In particular, raw materials producers Indonesia, Malaysia, Brazil, South Africa and Russia will benefit as their products are priced in US dollars.

Unfortunately, there are negative implications from devaluation for both the populace and local businesses. The table shows how far the US dollar has appreciated. The Indian rupee's devaluation from its top to bottom was 29 per cent. Other things being equal, exporters' products priced in international rupees fall to 71 from 100, making them extremely competitive. On the other hand, importers paying dollar prices would have to pay 40.8 per cent more.

Thus the price that they would have to pay, all things being equal, would be 141, compared with 100 previously. The inflationary implications of importing food are, therefore, awful, while there is also a severe squeeze on businesses which have to import raw materials, machinery, computers and other items. Higher oil prices because of Middle Eastern tensions add to the burden.

The other devaluation impact is on businesses which have loans denominated in dollars and other stronger foreign currencies. Businessmen, bankers and economists are finding anecdotal evidence that companies in Asia took advantage of much lower US interest rates and borrowed in US dollars. These companies and their bankers are thus exposed to a more expensive dollar.

In other words, repayments of the loans and interest will have to be made with a lot more rupees, rupiahs, ringgit and baht. (Due to interest rate differentials, forward US dollar exchange rates were at a discount when loans were negotiated, so it was difficult to hedge foreign exchange exposure.)

The sums are potentially large. As the Bank of International Settlements (BIS) shows, foreign exchange assets of banks based in Malaysia, for example, rose from US$33.1 billion (S$42 billion) in December 2010 to US$49.6 billion in March 2013 and liabilities from US$27.1 billion to US$45.6 billion. Increases in Asian bank exposure to foreign currencies are also evident in other Asian countries.

Banking sources say local and foreign banks in Asia and other emerging markets are closely examining the risk exposure of borrowers. They believe that banks will be cautious about further local and especially foreign loans and that loan provisions are likely to increase because of problematic clients.

Brendan Brown, London-based head of economic research at Mitsubishi UFJ Securities International, fears there could be large corporate failures that could affect global markets. He has been warning about the regional consequences of US Federal Reserve Board quantitative easing for several years.

The "monetary dislocation" caused US and other global investors to "seek yield" in emerging and other markets. These speculative flows caused property, bond, share and other asset price inflation. Now fears of tightening have brought about withdrawals, and a US dollar surge.

Mr Brown cautions that the emerging currency crisis could spill over to the euro, sterling, yen and other currencies. European and US exporters to Asia and other emerging nations could well experience a fall in orders and this will ultimately be reflected in their results.

The knock-on impact will be persistent demand for dollars to repay the loans, bankers say. Regional and other emerging market central bankers are faced with a dilemma. Do they raise interest rates to protect their currencies and counter inflation or do they ease to prevent a business downturn?

Morgan Stanley's base-case scenario suggests that "while emerging markets and macro policy will be stressed further during the current transition period, we will not witness a widespread 'sudden stop' of the kind experienced in 1998".

Instead, the bank expects "differentiation, based on structural reform winners and losers and separating the vulnerable from the not-so-vulnerable".

David Bloom, foreign exchange economist of HSBC, contends that the euro and sterling have been firm against the dollar because of "signs of stabilisation in the eurozone economy".

Despite the improvement in data recently, consensus expectations for eurozone growth in 2013 "remain deeply negative", he reckons. HSBC predicts that the dollar will eventually rise against developed nation currencies.

American Enterprise Institute resident scholar John Makin takes the opposite view. He believes the market surprise will be another bout of quantitative easing. Home sales and building have slackened because US mortgage rates have followed US Treasury bond yields higher.

A narrowing budget deficit is cutting the supplies of Treasury bonds, and "taper trauma" interest rate increases are bringing in their wake a generally slower US economy.

In such circumstances, the US dollar could weaken and reduce some pressure from emerging nations, Mr Makin contends.

(Source: The Business Times)

MARKET SCOOP

Singapore steps up scrutiny of Indian bank branches: bankers

CSC clinches two contracts

XMH Holdings Q1 profit up 23%

Temasek Holdings names Wu Yibing head of China

Temasek unit plans up to US$185 mln selldown Youku Tudou: IFR

Offer for Singapore Windsorlaunched at S$0.18/shr

Unemployment rate rises to 2.1% in June

China Gaoxian responds to CAD's request

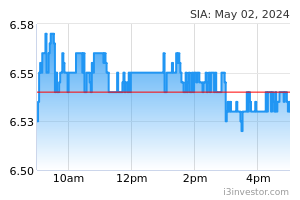

(Source: The Business Times) DBS Securities says... SINGAPORE AIRLINES | BUY | TP: S$11.40

SIA's share price has recently broken below -1SD (0.92x P/BV) in August to its current level of 0.87x P/BV, or -1.3SD

This is a level seen previously only in crises such as 9/11, SARS, and the GFC

Also, at this current price, the rest of SIA is valued at less than S$3 per share if we were to strip to out its net cash and stake in SIA Engineering

Despite weak earnings in recent quarters, SIA's net cash per share has grown to S$4.20 as of June'13, and given SIA's good track record of rewarding shareholders in the past, there is a firm chance that SIA will return some of this cash to shareholders, via capital reduction or special dividends

Over the last decade, SIA has distributed nearly S$8 per share in total to shareholders, which works out to be an average of c.S$0.80 per year

Upgrade to BUY, S$11.40 TP based on 1x FY14 P/BV, which translates to -0.5SD, reflecting the still muted outlook for Singapore's premier carrier

Nonetheless, we see the stock's current valuation at 0.88x P/BV as an attractive level for entry and hence, we upgrade our call for SIA to a BUY

Catalysts for re-rating would include better earnings and/or a cash distribution to shareholders

UOB KAY HIAN says ...

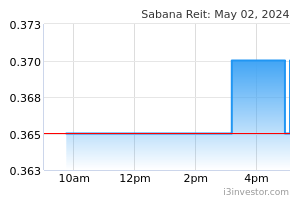

SABANA REIT | HOLD | TP: S$1.29

Sabana REIT (Sabana) has completed a private placement of 40m new units at an issue price of S$1.00 per unit to raise gross proceeds of S$40.0m

Net proceeds are approximately S$39.2m after fees

The 40m new units represent a 6.2% increase from the 649.7m units in issue as at 30 June 2013

The underwriters are HSBC and Morgan Stanley

The placement price of S$1.00 per unit represents a 9.6% discount to the adjusted Volume Weighted Average Price (VWAP) of S$1.1066 per unit for trades done on 12 September (less the proposed advanced distribution) and at a 11.1% discount to the last traded price of S$1.125 per unit

The issue price also represents an 8.3% discount to the adjusted NAV per unit of S$1.09 as at 30 Jun 2013

The net proceeds of S$39.2m will be used to fund 58% of the S$67.2m acquisition of the Advanced Micro Devices' (AMD) light industrial building at 508 Chai Chee Lane which was announced on 22 August

Sabana has also announced an estimated advanced distribution of 2.2 S cents for the period 1 July to the date prior to which the new units are issued (estimated 24 September 2013)

Details will be announced at a later date when the management accounts for the period has been finalised

Aggregate leverage remain at 37.2%, following the acquisition and the private placement, relatively unchanged from the 37.1% as at 30 June 2013

We had earlier estimated that if the acquisition had been fully-funded by debt, gearing would have reached 40.5%

We see a potential near-term 2-3% dilution of DPU as the acquisition is currently 50% occupied, and would need some time to be fully leased out

We currently have a HOLD on Sabana with a target price of S$1.29 based on DDM (required rated of return:8.1%, terminal growth of 1.8%)

We may relook our DPU assumptions as we had factored the acquisition to be fully-funded by debt DMG OSK Securities says... OUE HOSPITALITY TRUST | BUY | TP: S$0.94 OUE Hospitality Trust (OUEHT) is a stapled group consisting of OUE Hospitality Real Estate Investment Trust (OUE H-REIT), a REIT under which the initial portfolio is held, and OUE Hospitality Business Trust (OUE H-BT), a dormant business trust

The initial portfolio of OUE HREIT comprises Orchard Road area's largest hotel, the 1,051-room Mandarin Orchard Singapore (MOS) and the 196,336 sq ft GFA Mandarin Gallery (MG)

MOS is a prominent, upscale hotel located along Orchard Road while MG is a notable landmark with 152 metres of prime Orchard Road frontage

These assets make OUEHT the only pure Orchard Road play in the REITs/Business Trust space

This initial portfolio has an aggregate value range of S$1,705m-S$1,756m, based on independent valuation estimates

Approximately 69% of the valuation is from MOS

Some headwinds for hospitality, but largely in the price

The current oversupply situation in the Singapore hospitality sector is a known concern

Given this, we are pleased to note that MOS clocked 3.3% RevPAR growth for pro forma 1Q13

It is also worthwhile noting that 46.7% of MG's leases by NLA have attractive step-up rental increases of 5.5% p.a., with only 20.7% of all leases by NLA expiring in FY13 and FY14

Right of First Refusal (ROFR) for three assets

OUEHT's sponsor is Overseas Union Enterprise Ltd, a well-established real estate owner, developer and operator

There are currently three sponsor-granted ROFR properties, Crowne Plaza Changi Airport, Meritus Mandarin Haikou China and Meritus Mandarin Shantou China

These properties could provide some medium-term growth for OUEHT, potentially more than doubling the number of hotel rooms to 2,233

Based on a dividend discount model, we arrive at a fair value of S$0.94 for OUE Hospitality Trust and initiate our coverage with a BUY |