Gartner forecasts that by 2020 there will be 21 billion connected “things” in the world. In the coming years, financial institutions will not be able to avoid

wondering how this multitude of IoT devices can help their business. Let’s touch upon some IoT use cases in financial services.

How the Internet of Things Changes the Banking and Finance Industry

In the last decade, due to constantly changing consumers’ preferences, financial institutions, like many other industries, have been forced to invest into and develop digital strategies and adapt to the accelerating pace of innovations.

A reliable digital portfolio is a priority for every financial institution that wants to grow and be competitive. Today, customers can be in touch with their bank using a laptop, a tablet, a smartphone or a smart watch. The advantages of such connections

are pumped up by the development of the market of the innovative IoT in banking and finance, which allows banks to collect more data about their customers’ preferences, their behavior and needs.

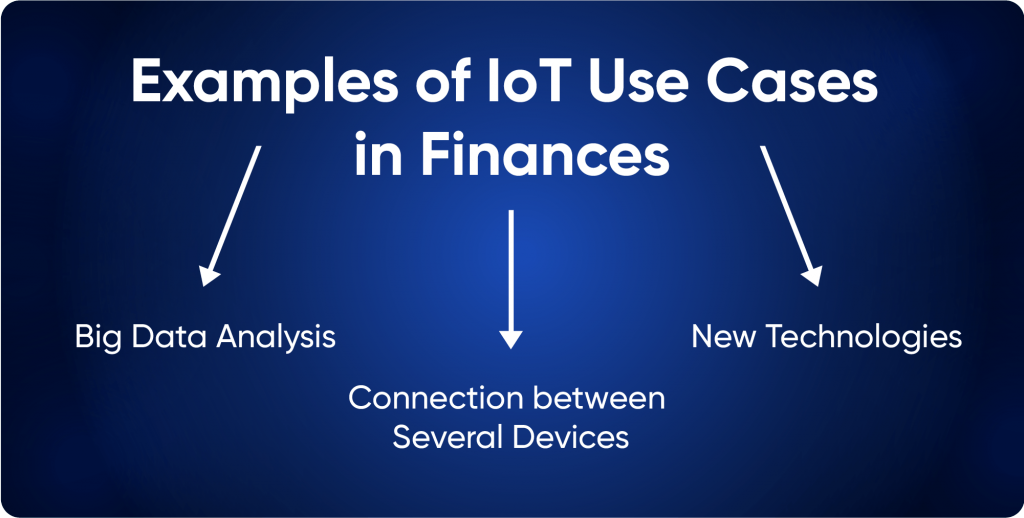

Big Data Analysis

The use of IoT technologies ensures the collection and analysis of large amounts of banking information. The bank learns more about its customers by receiving information from IoT devices, thereby it improves internal decision-making processes in terms of

service delivery, product strategy and investment.

Banks can use the obtained data to better understand and track the behavior of their customers. This will provide customers with a more personalized experience. What is more, banks will develop targeted commercial offers of banking products and services.

Banks will have the opportunity to reach a new level of understanding of needs and relationships with customers.

For example, such data can be used by banks to get a better picture of individual credit risks. The same data will help to develop individual customer reward programs and thus increase their loyalty. Thus, banks can take personalized banking to a whole new

level.

The IoT can help financial institutions stay one step ahead, allowing them to better understand the whole situation in other spheres. For example, data analysis can deliver a real-time status of the situation in retail, industry, or agriculture, which is

important in exploring new markets and improving underwriting processes.

The practical use of the IoT in a banking environment can be diverse. Today, biometric and positional sensors are being installed in bank offices, coupled with video cameras, which allows to recognize a client from the moment he or she enters the premises.

The analysis of information from sensors located at ATMs makes it possible to determine the optimal zones for installing the devices. Using information based on the data related to the customer and location, banks can determine their needs by offering relevant

products and helping them make financial decisions that are acceptable to both parties.

In the upcoming years, customers will begin to perform large-scale transactions using home and wearable smart devices. Options include the ability to perform basic operations through special applications using wearable (fitness trackers, smart watches) and

voice devices, car GPS systems, invisible payments for transport and restaurant services, etc.

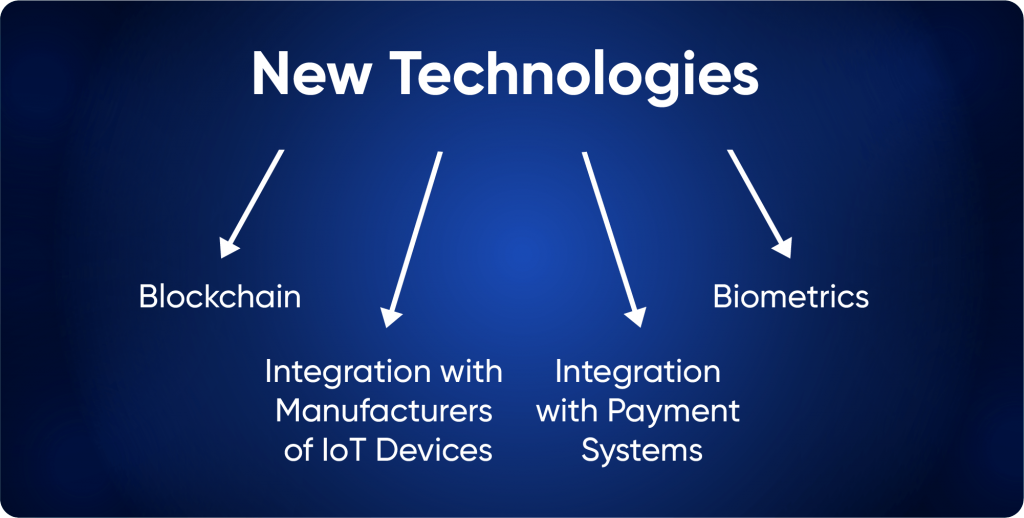

So, which technologies can banks introduce to keep customers and their positions in the banking system?

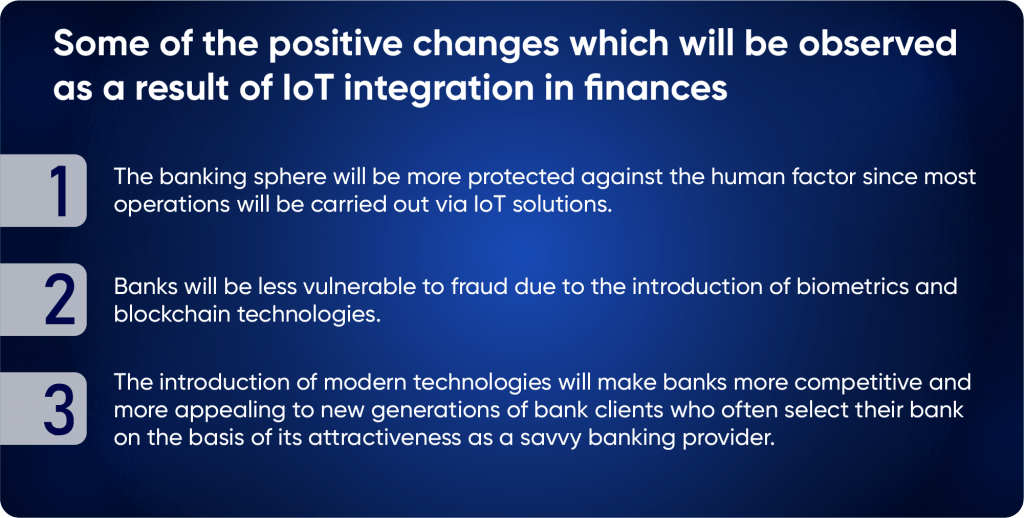

First and foremost, it is blockchain technology, since it can minimize costs/losses by reducing fraudulent activities and reduce money spent on staff and information technologies. Unfortunately, banks are not so much interested in introducing this

technology, since it completely changes the structure of their activities.

Secondly, banks need to use biometric technology in customer service. This is an expensive technology, but it protects the bank from financial losses caused by cheaters. Currently, many banks use cameras to identify customers (Face ID), but this is

also unsafe. Note that the use of the two-factor authentication of clients in banking applications is often a must. This is also envisioned by Europe’s Payment Services Directive, which obliges customers to use this type of authentication when logging into

their account in order to ensure the safety of their savings (biometrics, passwords or tokens are requested in this case).

Thirdly, it is the integration of banks with developers of IoT devices and payment systems (Visa, Master Card, UnionPay, PayPal). This is a classic IoT scheme with great financial opportunities. However, it may give rise to the following issues: authentication

methods of the payment owner; the place for storage of payment details; the possibility of unauthorized access to data; conflict resolution for unauthorized payments.

Among the new IoT technologies in the finance industry, we may also specifically point out robots and drones for cash delivery.

In general, the IoT in finance is a highly automated sector which seeks the “value” of new IoT solutions.

Connection with Several Devices

Digital technologies form the operational models of the banking sector. The most popular innovations were cloud technologies, Big Data, AI, ML, process automation, blockchain and the IoT. As a result, today’s customers have the chance to contact the bank

and manage their accounts through tablets, smartphones, laptops and even smart watches. In addition, a separate phenomenon emerged — the concept of the “Bank

of Things” — automatic payments that various devices can make without human intervention.

The emergence of a generation of more “advanced” customers (generations Y and Z) forced banks to adapt to the fast pace of development of information technology and the introduction of innovation. And the emergence of the IoT concept simply contributes to

the transformation of the banking industry to maintain its competitiveness against the fast development of FinTech companies.

Innovation Integration

In the near future, we will witness a huge impact on the part of innovations driven by FinTech and other industries. As of now, the Internet of Things has not unveiled its full potential, which will define business strategies of forward-thinking banks. Banks

will be able to eliminate the danger of extinction by keeping up with the world digitalization tendencies of everything that surrounds us.

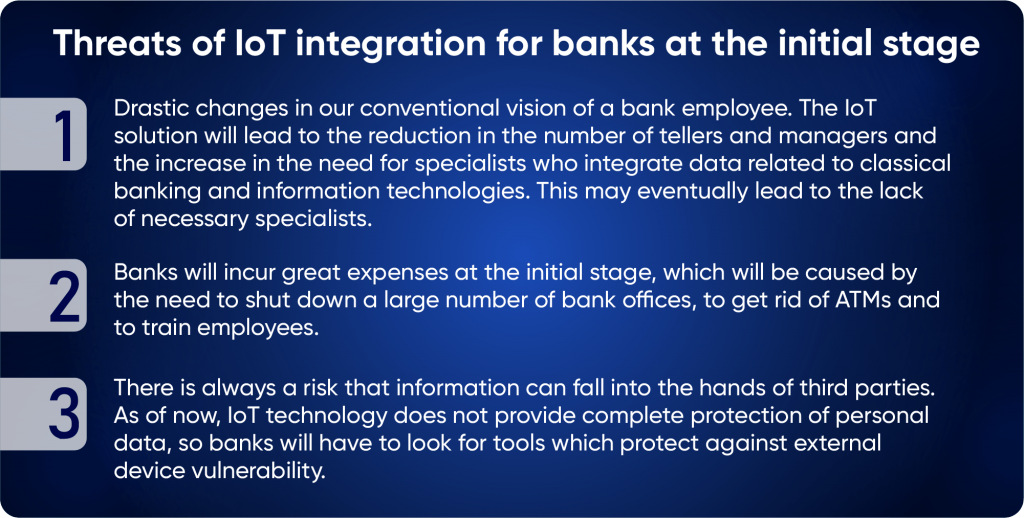

Nevertheless, we insist that it is impossible to completely exclude the human factor: firstly, because someone has to configure information exchange technology; secondly, control over the use of information is extremely necessary. Especially in the banking

sector, where most of the information is bank secrecy, and its leak carries both financial and reputational risks.

More will be revealed in the upcoming second part of this article.

About the author:

Denis Novikov, Deputy Director of Business Development at Qulix Systems.

Denis is:

· A strategy development consultant for Digital Banking products;

· An expert in the field of software development and implementation for financial organizations;

· A representative of the StandFore FS intellectual banking platform.