Opinion

Why a family trust could be your best friend in retirement

Looming increases to minimum pension drawdowns present a problem to retirees whose income is more than they actually need.

Michael HuttonContributorFor retirees who have built up a large super balance, a key question is what to do if you have to draw down more than you actually need. To qualify for tax concessions, you are required to withdraw from your super fund a minimum pension each year.

The reason pension-paying super funds are required by the government to make minimum annual pension payments is to ensure they are being used to provide a retirement income rather than just being used as a tax-advantaged method of building wealth for your beneficiaries.

If a super fund, including self-managed super funds, fails this minimum pension test, it loses concessional tax treatment and the tax rate reverts to the normal 15 per cent rate applicable to accumulation superannuation accounts.

However, if you live a frugal lifestyle and don’t need all that money from your super pension each year, what do you do with the excess?

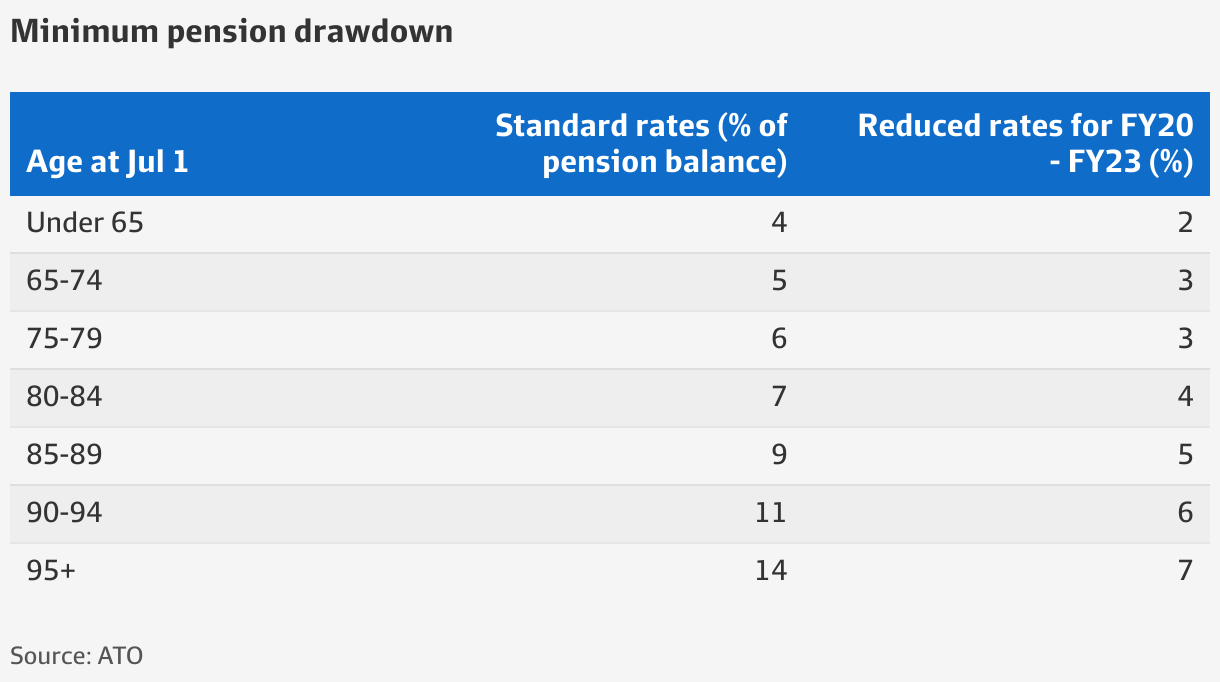

Admittedly, this is a great problem to have, but it’s important you make the most of this welcome opportunity. And it can become more pronounced as you get older as you are required to take a greater proportion.

Further, from July 1, 2023, the rates may revert to normal after four years of half rates introduced as a COVID-19 concession.

How it works

Consider a retiree couple who have $1.7 million each in pension mode in super, making $3.4 million in total. They are both 76, which means they are each required to draw a minimum of three per cent a year from their super to fund their super pension, or $102,000. This is tax-free income to them.

From July 1, 2023, the required minimum pension drawdown is likely to revert to six per cent for them, after which they must take combined payments of at least $204,000 from their super for the 2023-24 financial year.

When they reach 80, the standard rate increases again to seven per cent. If their pension balances were maintained at $1.7 million each, the required combined pension payments would amount to $238,000, tax-free.

Due to indexation, the limit for new pensions may increase from July 1, 2023, from $1.7 million to $1.9 million. A couple may have up to $3.8 million in pension accounts from which they may be required to draw $190,000 per year at five per cent, or $266,000 at seven per cent if they are over 80.

Where to put the excess

It’s certainly possible for a retired couple to live a comfortable lifestyle with a mandated yearly pension drawdown and still have plenty of money to spare. So, what can they do with that money?

An alternative could be to set up another non-superannuation investment account – either in joint names or, if there is other substantial wealth, in a family trust or investment company. The pension payment can then be paid to that investment account and the couple can draw only what they need and invest the remaining balance.

Depending on whether they have any other taxable income, investment earnings could attract very little tax due to the individual’s tax-free threshold.

This strategy can be particularly useful when one spouse dies and a large lump sum superannuation death benefit may be paid out. This death benefit can also be added to the non-super portfolio.

Some wealthy retirees also use the spare income to assist their children or grandchildren. Using a tax-free superannuation pension income is a great way to fund the part payment of a grandchild’s non tax-deductible school fees, for example.

You may even wish to donate more to your charities of choice and get to see the benefits conferred, rather than leaving bequests as part of your estate planning.

Whatever you do, all the money accumulated over a working life should be doing something useful, and not just sitting idle. You’ve worked hard for your money, and now that you’re in retirement, make it work for you.

Subscribe to gift this article

Gift 5 articles to anyone you choose each month when you subscribe.

Subscribe nowAlready a subscriber?

Introducing your Newsfeed

Follow the topics, people and companies that matter to you.

Find out moreRead More

Latest In Personal finance

Fetching latest articles