We create rating systems that evaluate each company on consistent measurements. Our editors choose which metrics best reflect the companies or policy types being scored. Our metrics and ratings are not influenced by advertisers.

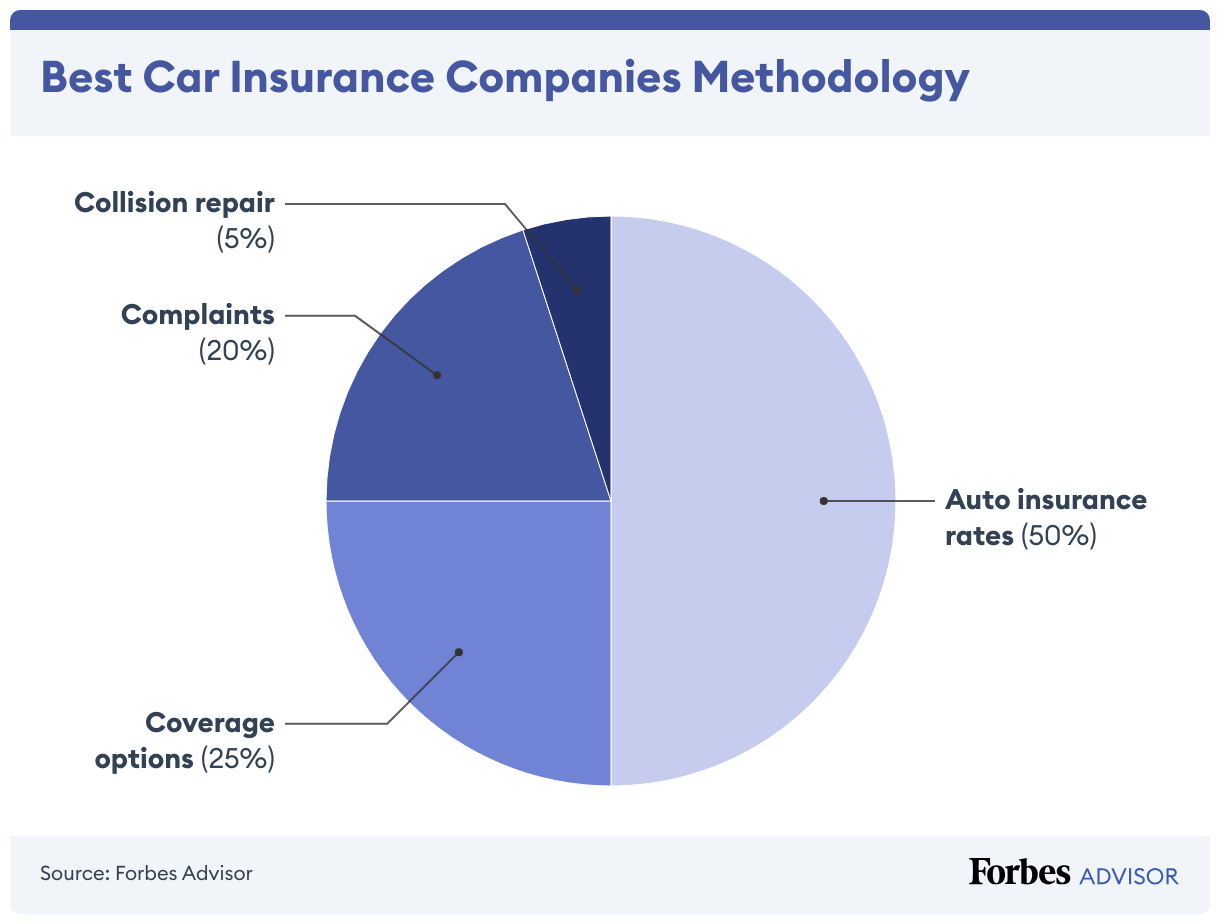

Best Car Insurance Companies of 2024

The best car insurance companies offer budget-friendly rates and a wide variety of extra coverage options, so we weigh these factors more heavily.

• Auto insurance rates: 50% of score

• Coverage options: 25% of score

• Complaints: 20% of score

• Collision repair: 5% of score

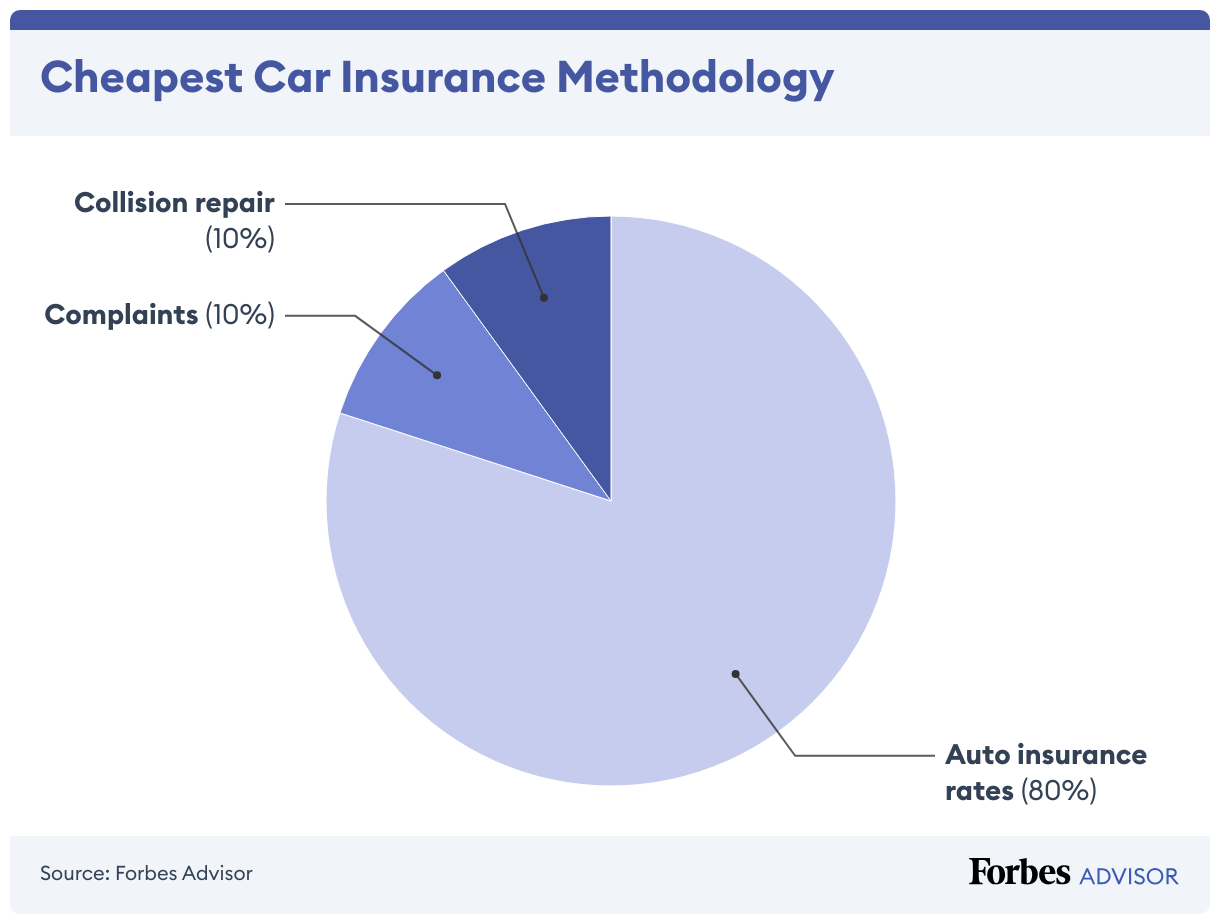

The Cheapest Car Insurance of April 2024

Cost matters the most when looking for the cheapest car insurance, so we focused primarily on rates.

• Auto insurance rates: 80% of score

• Complaints: 10% of score

• Collision repair: 10% of score

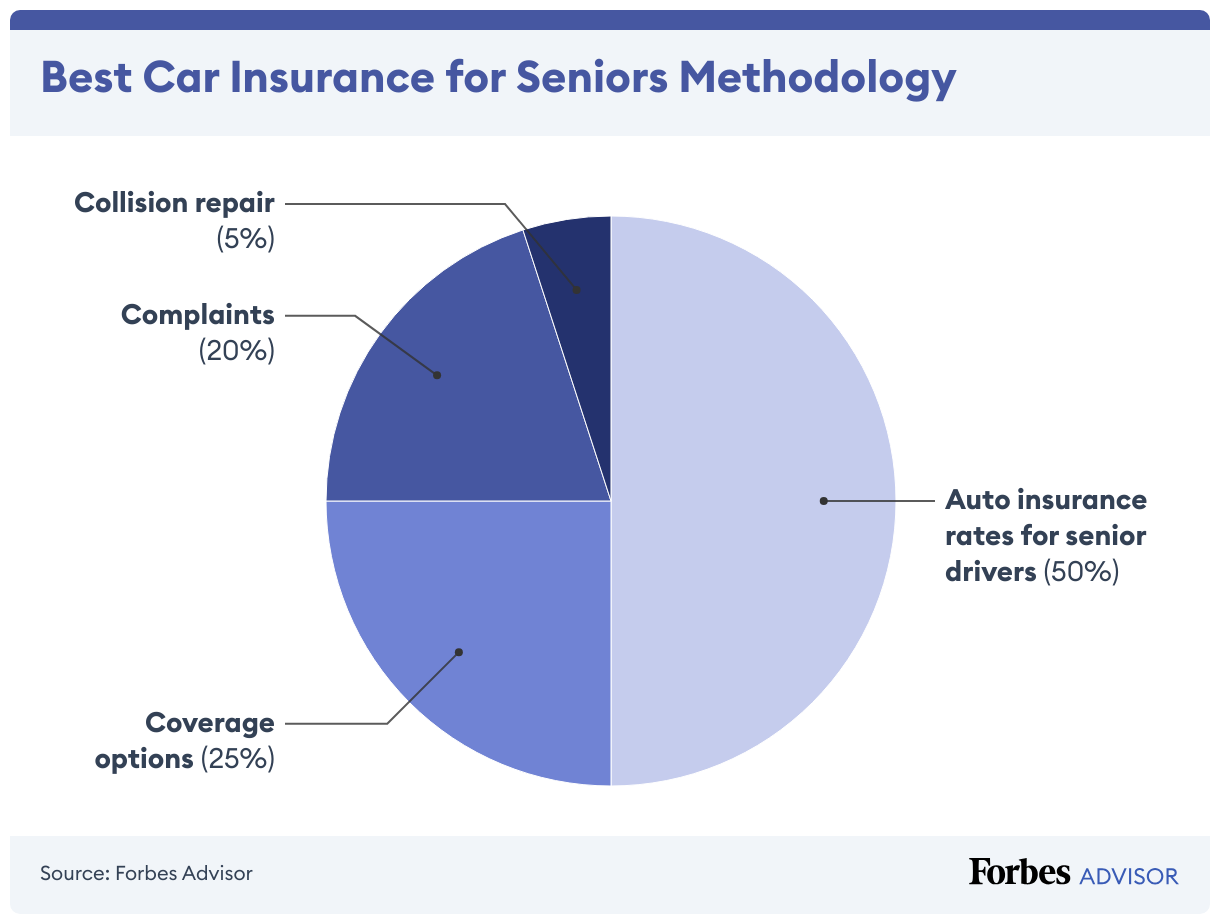

Best Car Insurance Companies for Seniors of 2024

To find the best car insurance for seniors we focus on costs for drivers age 65 to 80 and coverage options.

• Auto insurance rates for senior drivers: 50% of score

• Coverage options: 25% of score

• Complaints: 20% of score

• Collision repair: 5% of score

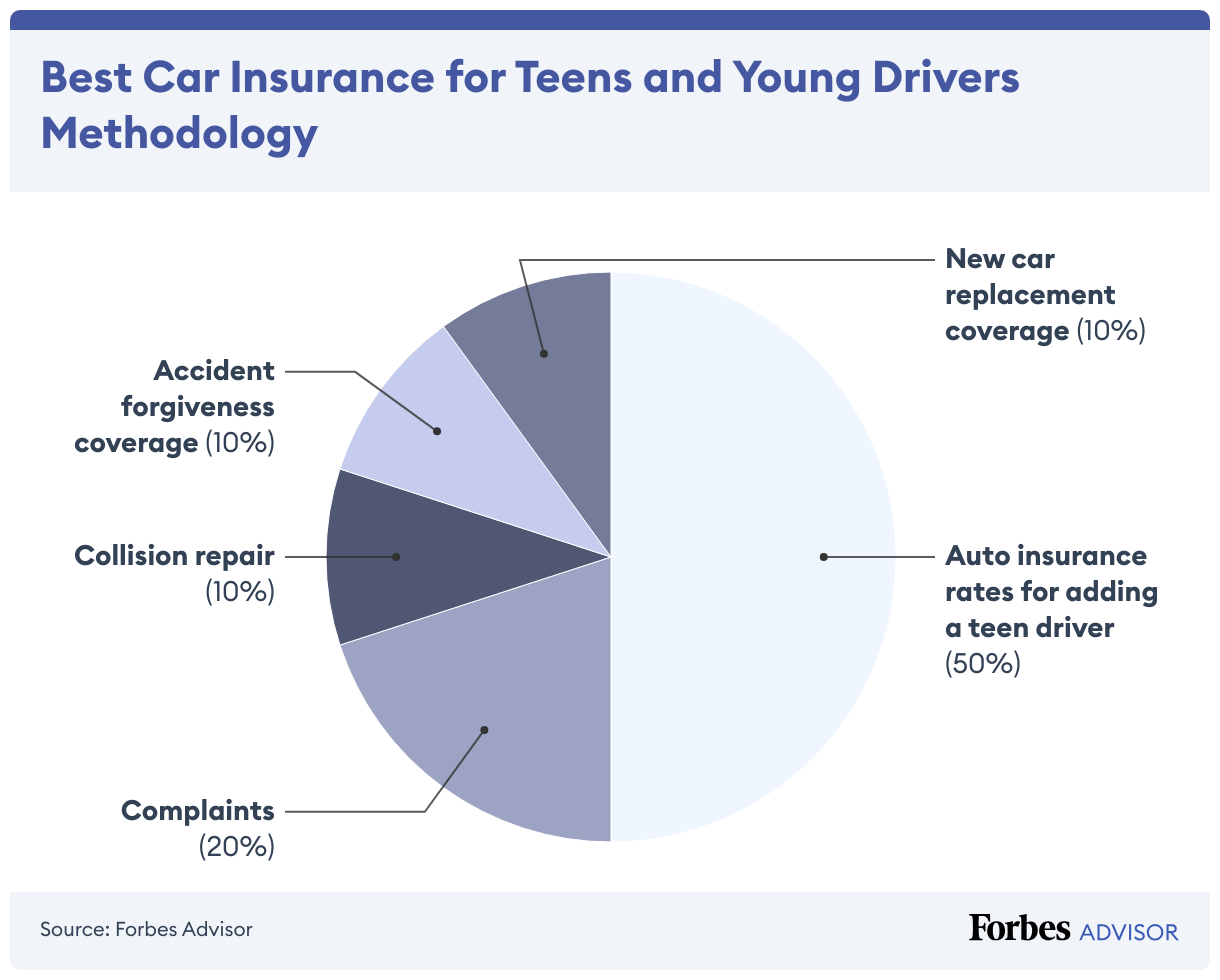

Best Car Insurance for Teens and Young Drivers of 2024

To find the best car insurance for teens and young drivers, we focused on the cost of adding a teen driver to a parent’s policy and two additional coverage types: Accident forgiveness and new car replacement, which are valuable when you have an inexperienced driver behind the wheel.

• Auto insurance rates for adding a teen driver: 50% of score

• Complaints: 20% of score

• Collision repair: 10% of score

• Accident forgiveness coverage: 10% of score

• New car replacement coverage: 10% of score

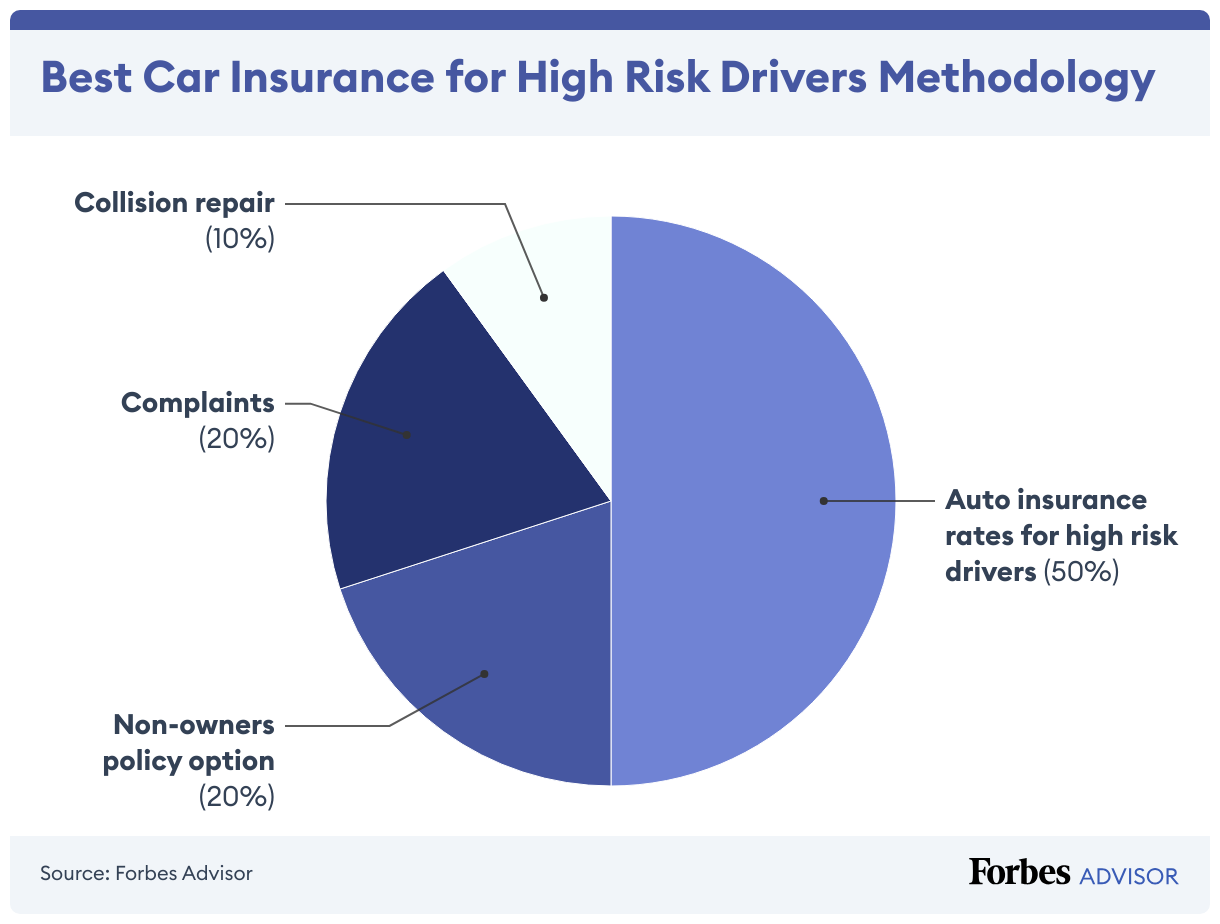

Best Car Insurance Companies for High Risk Drivers of 2024

To find the best car insurance companies for high risk drivers we looked at only insurers that offer SR-22 filings, as high risk drivers are more likely to need this certificate of financial responsibility. We analyzed the cost of auto insurance for drivers who caused an accident with injury or property damage, drivers with a DUI and drivers with poor credit, as these issues tend to get someone labeled as a high risk driver.

• Auto insurance rates for high risk drivers: 50% of score

• Non-owners policy option: 20% of score

• Complaints: 20% of score

• Collision repair: 10% of score

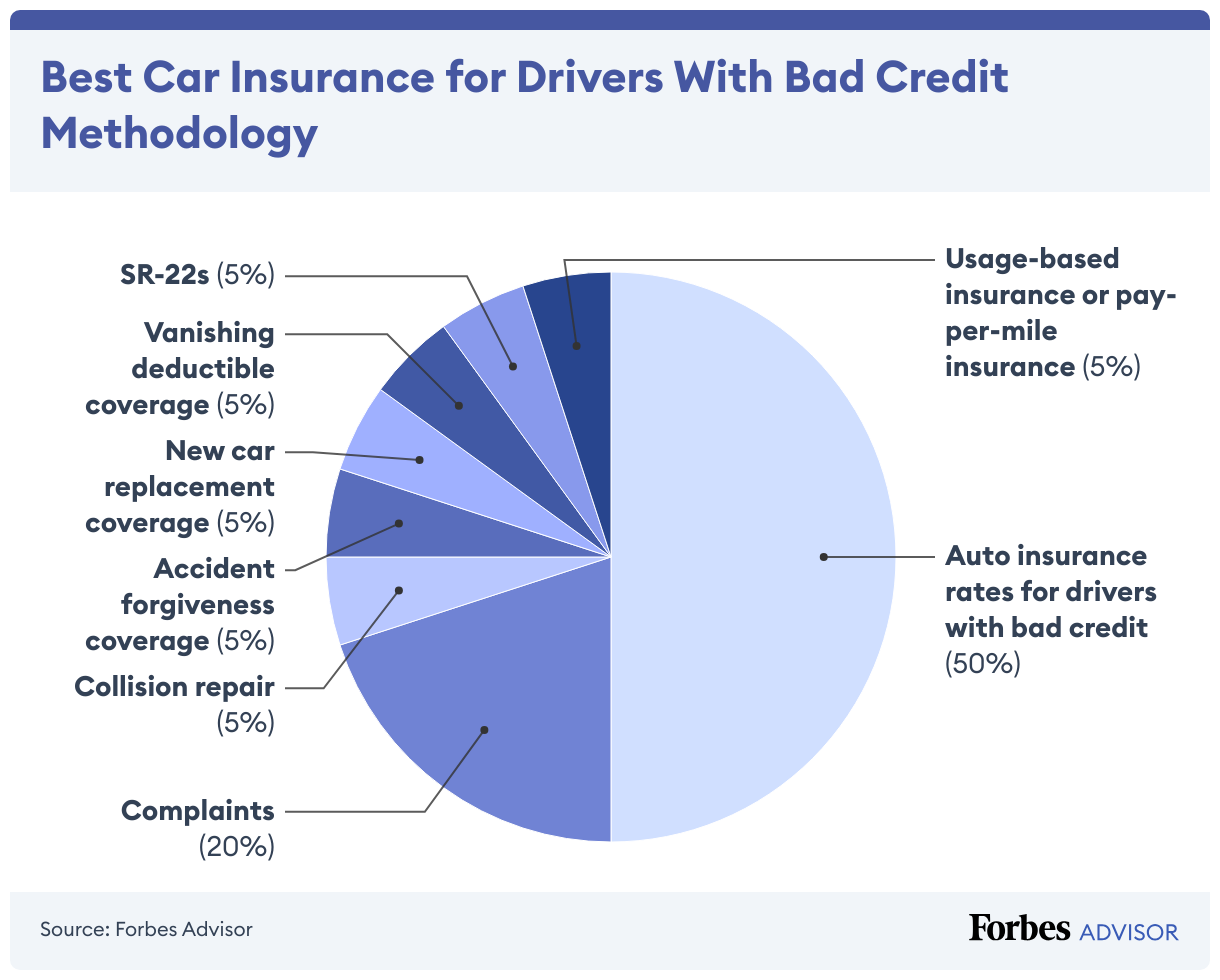

Best Car Insurance for Drivers With Bad Credit of 2024

To determine the best car insurance for drivers with bad credit we focused on rates for drivers with poor credit as well as helpful coverage types.

• Auto insurance rates for drivers with bad credit: 50% of score

• Complaints: 20% of score

• Collision repair: 5% of score

• Accident forgiveness coverage: 5% of score

• New car replacement coverage: 5% of score

• Vanishing deductible coverage: 5% of score

• SR-22s: 5% of score

• Usage-based insurance or pay-per-mile insurance: 5% of score