Soft College Loans are Prepared, Students Pay Once They Get a Job

The option of financing college through government-subsidized "student loans" is being seriously discussed, targeting the lower middle class.

This article has been translated using AI. See Original .

About AI Translated Article

Please note that this article was automatically translated using Microsoft Azure AI, Open AI, and Google Translation AI. We cannot ensure that the entire content is translated accurately. If you spot any errors or inconsistencies, contact us at hotline@kompas.id, and we'll make every effort to address them. Thank you for your understanding.

The following article was translated using both Microsoft Azure Open AI and Google Translation AI. The original article can be found in Pinjaman Lunak Kuliah Disiapkan, Mahasiswa Bayar Setelah Dapat Kerja

A number of students from the Bandung Institute of Technology demonstrated in front of the ITB Rectorate on Sulanjana Street, Bandung City, West Java, on Monday (29/1/2024). They demanded convenience in paying the single tuition fee without having to involve high-interest online loans.

JAKARTA, KOMPAS — Student loans or student loans for students are possible in Indonesia. The soft student loan scheme is planned to be paid after students graduate from college and when they get a job. The loan amount depends on the student borrower's application.

"Soft student loans are planned for students from middle to low-income families. "These are the ones who have a lot of financial difficulties and are in arrears on single tuition fees or UKT but do not qualify for scholarships for poor students," said Warsito, Deputy for Coordination of Education Quality Improvement and Religious Moderation, Coordinating Ministry for Human Development and Culture in the webinar "Tuition Costs High, Education Loans Become Solution” in Jakarta, Monday (18/3/2024). This discussion was held by the West Merdeka Forum 9.

According to the 2023 National Socio-Economic Survey (Susenas) by the Central Statistics Agency, only 10.5 percent of the population aged 15 years and above have had access to higher education. The Gross Enrollment Ratio (GER) in higher education is still below 40 percent. However, in order to achieve Indonesia's Golden Jubilee in 2045, the GER in higher education must reach at least 60 percent.

Excellent human resources from graduates of higher education are needed by our nation. However, access to college education is still difficult for students from low to middle-income families. As a result, the threat of dropping out of college looms over students because they are unable to pay, while scholarships cannot be given due to limited availability and economic ineligibility.

According to Warsito, coordination with various ministries/agencies is being seriously discussed. Funding scenarios have been intensified, including regulations that protect students. "We are currently discussing how loans can be made as soft loans, with repayments beginning when students graduate and start working. Repayments could even be made in the second year after graduation," he said.

Student loan scenarios will be prepared with very soft interest rates, such as those applied to microcredit of 3 percent per year or without interest. In addition, revolving funds can also be used. Support from non-governmental entities is also being studied, for example from philanthropy and corporate social responsibility (CSR) to support the scenario of soft loans without interest.

Also read: Middle Class Bears Heavy Burden of Paying for Children's College Education

In order to avoid payment failure or bad credit, said Warsito, there are several aspects to pay attention to, namely governance. This is so that borrowers after graduation know what their ties are, including being included in a collaboration database with alumni associations at universities.

"In the past, repayment obstacles occurred in Indonesian student credit loans because graduates were difficult to trace their whereabouts after graduation. Learning from this, various governance scenarios with the unification of population identification number (NIK) data, like developed countries, can be traced well. Valid governance and data unity are necessary," said Warsito."

Workable

Elza Elmira, an academic with a PhD in Development Research from the University of Bonn, Germany, explained, referring to Indonesian student credit, loans provided and supported by the government for students from the middle group and below. However, the failure rate reaches 95 percent, making it a burden on the government.

As a result, banks looking to enter the student loan space are worried. Apart from that, the tax system in the past was not good and tracing or tracking population data was not as sophisticated as it is now, so borrowers could not be asked to pay back their debts.

"One of the most important things about student loans is a system to be able to track students who borrow when they graduate. "With increasingly advanced population data and a much better tax system, the student loan scheme in Indonesia can be implemented," said Elza.

Also read: Considering College Loan Schemes Without Getting Into Debt for Life

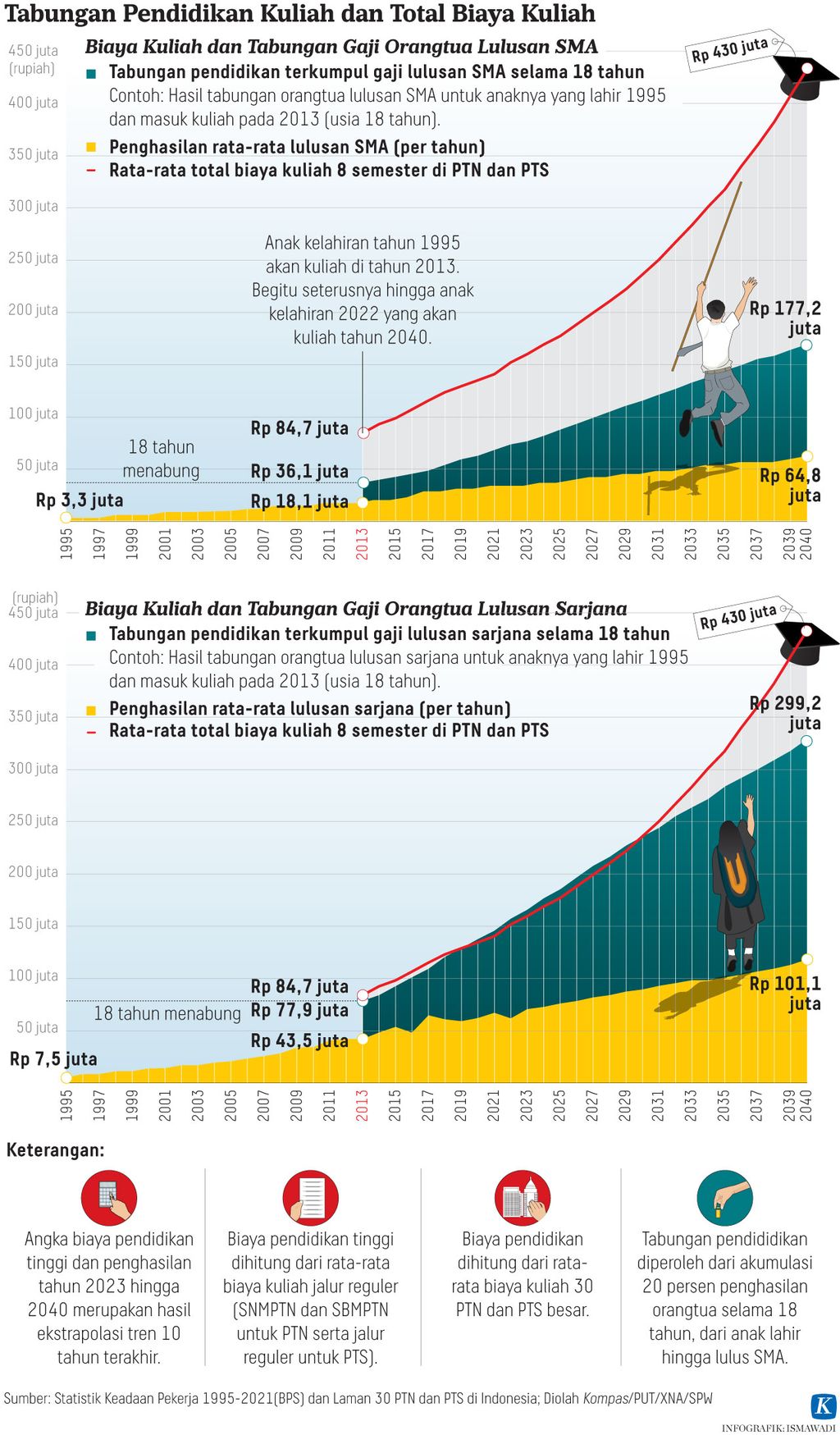

In 2014-2015, when Elza conducted a study, data from Susenas BPS showed that the expenses of poor students to obtain an undergraduate degree (S-1) reached Rp 49 million per year. This amount is almost equal to the government scholarship. However, this amount does not include personal expenses for books, transportation, and living costs. Meanwhile, the cost of tuition in state universities (PTN) can reach up to Rp 100 million, and even higher in private universities (PTS).

Dozens of students who are members of the IAIN Cirebon Student Alliance are protesting at the IAIN Syekh Nurjati Rectorate Office in Cirebon City, West Java on Tuesday (30/6/2020). The protesters are demanding a reduction of the single tuition fee and a subsidy for remote learning quotas during the Covid-19 pandemic.

Elza explained that the problem of student loans abroad occurs when the borrower's payments become an economic burden, especially with a mortgage model with a fixed amount paid every year. Meanwhile, when the borrower has economic difficulties due to layoffs or a decrease in income, the installment amount remains the same so that the borrower has difficulty paying and default occurs.

The income contingent loan (ICL) scheme tries to answer the problem of student loan defaults. Payments are made after graduates have a certain income and when the borrower has economic difficulties, the borrower does not pay. The amount of payment is in the range of 8-11 percent of total income.

"Previously, there was a study from Australia which found that in Indonesia, with a mortgage system, debt repayment burden can reach 30 percent in Java and for low income individuals in Sumatra it can reach 85 percent, making the repayment burden too large. Therefore, in many developed countries now, a scheme that is being considered is ICL so as not to discourage students from taking out loans because of fear," said Elza.

Soft loans are provided, repayment is made after the student graduates and starts working. It is possible to repay the loan during the second year after graduation.

Using the ICL scheme, for 25 percent of graduates with the highest income, the government subsidy burden is only 12 percent of the debt. As for the very bottom segment, the government subsidy burden is around 45 percent or almost half. "With the ICL system, student loans become like semi-scholarships," said Elza.

Through research conducted, it was found that borrowers from the lowest group (bottom 25 percent) with minimum wages can only pay off their debts 2-3 years after graduation. Meanwhile, high-achieving students and those from wealthier families can immediately pay off their debts, approximately six months after graduation.

Keep providing scholarships

Warsito added, even though there will be soft student loans, poor people will still be provided with college scholarships or KIP Merdeka. This scholarship is targeted at the 30 percent of the population whose income is at the bottom and outstanding students such as recipients of LPDP (Education Fund Management Institute) scholarships and other scholarships.

At present, the government provides approximately 1 million KIP Scholarships and affirmative scholarships for 7,500 students from the 3T regions (underdeveloped, remote, and border areas). It is even being considered to increase the number of recipients to benefit more underprivileged students.

Also read: Minimum Higher Education Budget, Access to College in Indonesia Still Difficult

Soft loans, interest-free loans, or microloans, explained Warsito, target the middle to lower economic class. Dropout rates are quite high in this group because when students have difficulty paying tuition fees, they cannot access government assistance. On the other hand, those in a higher income bracket are already capable of financing their education.

In the future, loans will be flexible or adaptive according to the needs and can be applied for at the beginning or middle of the study period, or only for the final project. Loans can only be applied for by those from middle-income to nearly low-income groups. The aim is to enable them to study with their own expenses, through a soft loan subsidized by the government. The government's interest is to ensure a high APK (Human Development Index) improvement, so that there are quality human resources available.

"Student loans are an option for those facing financial difficulties. Regulations are being prepared to target undergraduate and postgraduate students. Once the regulations are ready, they will be implemented soon, whether they will be managed by banks or public service agencies," said Warsito."